Why we like the volatility of the Brazilian stock market

Dear investors,

This year the Ibovespa started at 161,000 points, climbed to roughly 199,000 in mid-April, and pulled back to around 172,000 in the months that followed. Brazil's macro backdrop didn't shift meaningfully over that period. Even the crisis in the Strait of Hormuz, the most significant global event of the year, and the resulting swings in oil prices don't come close to explaining price moves of this size.

This is nothing new for our market. Over the past five years, the Ibovespa has fallen more than 20% in under six months on two separate occasions, and risen more than 20% over a similar span four times. Volatility is a feature of our market, not a flaw. Understood correctly, and paired with the right strategy, it's a source of consistent returns our own track record makes the case. Ártica Long Term just marked its 13th year last month, with an average annual return of 28.5%.

Heavy presence of foreign capital

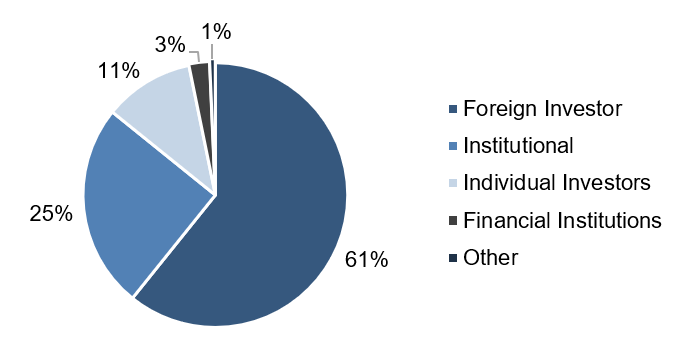

In May 2026, foreign investors accounted for 61% of total trading volume on B3. That group includes global emerging-market funds, index-tracking ETFs, hedge funds, sovereign wealth funds, and pension funds. The catch: despite driving most of the volume here, Brazil isn't a particularly important market to any of them.

Our stock market represents roughly 0.6% of global equities and about 5% of emerging-market equities. We show up in international portfolios for diversification, or on the back of a passing macro thesis not because these investors have done deep, company-by-company work. They tend to buy the most liquid names, or take positions based on broad sector calls.

The practical effect: tactical, short-term calls that barely register for a foreign investor can still move the Ibovespa significantly. During the rally through April, B3 saw a net inflow of R$69 billion in foreign capital most likely explained by global investors growing wary of how concentrated the U.S. market had become, and looking to diversify into emerging markets instead. The Ibovespa's rise tracked other emerging-market indices closely. During the pullback through June, that flow reversed: a net outflow of R$36 billion, likely driven by rising U.S. interest rates and a wave of U.S. mega-IPOs pulling capital back home. In short, what drove the sharp swings in the first half of the year had little to do with Brazil itself.

None of this means Brazil's own fundamentals don't matter it means they carry more weight over the long run than over any given month. If Brazil becomes a more attractive place to invest, we should see more capital flow in over the years. But what foreign investors do next month may have nothing to do with that story at all.

One way to think about this dynamic in peripheral markets: compare the restaurant scenes in São Paulo and Guarujá. Restaurant revenue in São Paulo tracks the city's economy fairly closely, since the customer base is mostly local people spend more when the local economy is doing well.

Guarujá is different. Its appeal as a tourist destination matters over the long run, but in any given month, weekend weather or a long holiday can move restaurant revenue more than the state of the economy. That's because whether to visit Guarujá is a low-stakes decision for the São Paulo tourist. A cloudy Friday sky is sometimes all it takes to call off a beach weekend, even if the actual odds of rain are low on closer inspection.

Peripheral markets are, by nature, more volatile: they're more exposed to external factors, and they get far less scrutiny from investors who hold only a sliver of their portfolios there.

Short-Term Focus and Pro-Cyclical Behavior

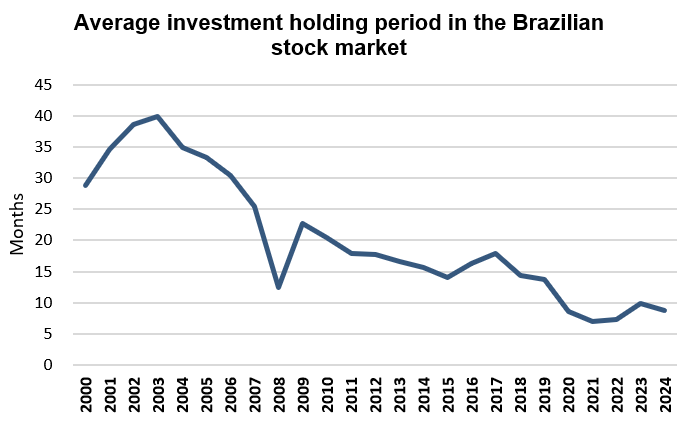

Another driver of local volatility is that average holding periods keep shrinking. In the early 2000s, investors held each stock for about three years on average. Since 2020, that figure has been under a year and the downtrend appears to be continuing.

Source: World Federation of Exchanges

Part of this compression comes from the growing weight of quantitative funds trading large volumes daily (high-frequency traders). But we've also seen it firsthand, in conversations with equity managers and individual investors: a large share of Brazilian investors are highly reactive to price swings over just a few months.

Rational buyers increase demand when prices fall and pull back when prices rise. The stock market tends to work the other way around. Many investors treat rising prices as the signal to buy and falling prices as the signal to sell a pattern known as momentum trading, built on the assumption that a recent price trend will keep going. It amplifies the intensity of market cycles, regardless of what actually triggered the move in the first place.

Now put both dynamics together: foreign investors adjusting their Brazil exposure for reasons that often have nothing to do with local fundamentals, and Brazilian investors making decisions based on short-term price trends. The result is volatility that's sometimes completely disconnected from the economic fundamentals of local companies a pattern that will feel familiar to anyone who has followed this market for a while.

Who Sets Valuations?

We've already noted that foreigners drive most of the volume on the exchange. Here's the full breakdown by investor type on B3:

Source: B3, May 2026

Institutional investors (funds and pension vehicles run by market professionals) are the group in the best position to set prices on the exchange. In theory, they should be the market's main price-setters. In practice, not all of them are fundamentals-driven: some are quantitative funds trading off statistical signals, others are passive vehicles simply tracking the Ibovespa, and others are multi-strategy funds more focused on macro calls than on individual companies.

Even within equity funds, some managers lean on chart patterns or broad sector narratives rather than hard numbers. And then there are the speculators, making short-term bets on rumors or news flow.

Traditional fundamentals-driven investors, the ones who dig into a company and put in the work to estimate its fair value, are a minority. They likely account for less than 10% of total volume on the exchange, though there's no official breakdown to confirm that figure precisely.

Trading volume translates into pricing power. With most participants trading for reasons other than fundamentals, it's no surprise that price and intrinsic value drift apart as often as they do on our exchange.

Where the Opportunity Lies

Fundamentals-driven investors don't actually want a market that's always right one that prices every stock at intrinsic value. A volatile, erratic market works in our favor: it creates buying opportunities when prices fall below fair value, and selling opportunities when they climb above it. That may seem to contradict the common view that volatility equals risk, but there's an important nuance here.

A company's operating volatility is not the same thing as its stock price volatility. In a well-priced market, the two should move together volatile prices should simply reflect volatile earnings. In a market with real pricing inefficiencies, prices can swing sharply even when the underlying business is stable. When that happens, price volatility isn't a source of risk it's a source of opportunity.

We're convinced the Brazilian market fits squarely into that second case. We've spent years tracking companies with reasonably stable operating performance and disproportionate swings in their stock prices. Our 28.5% average annual return exceeds the average ROE of the companies we've owned precisely because we've been able to exploit these price-to-value mismatches as they arose.

The idea that price swings should guide buying and selling decisions, never the investment thesis itself, isn't new. Benjamin Graham laid it out in 1949 in The Intelligent Investor, and Warren Buffett gave it its most memorable phrasing in Berkshire Hathaway's 1987 shareholder letter: “The market is there to serve you, not to instruct you.” It holds up just as well today for investors who can stay rational.