The New Cold War

Dear investors,

Read enough history and every episode seems to have a clean starting point. World War II began on September 1, 1939, when Nazi Germany invaded Poland. The Cold War between the United States and the Soviet Union began on March 12, 1947, with the announcement of the Truman Doctrine. But that clarity is really just hindsight historians tidy up the story after the fact. Lived in real time, the edges of any historical episode are far blurrier.

The U.S., China rivalry, impossible to miss today, has been building for more than a decade. Some argue we're headed toward a new world war; others believe the deep economic interdependence the two countries still share will keep the conflict contained. It's hard to say how far this goes, but it's already clear the rivalry has reshaped global geopolitics. Here are our reflections on those shifts, and on how they might shape what comes next.

History of the Rivalry

Back in the 2000s, China wasn't on Washington's radar as a threat. In fact, the United States was the main architect of China's accession to the World Trade Organization in December 2001. The logic at the time: integrating China into the global economy would hand American companies enormous cost advantages via cheap Chinese labor, and China's development within the global trading system would eventually nudge it toward Western practices and a more democratic political system. Neither prediction panned out over the decades that followed.

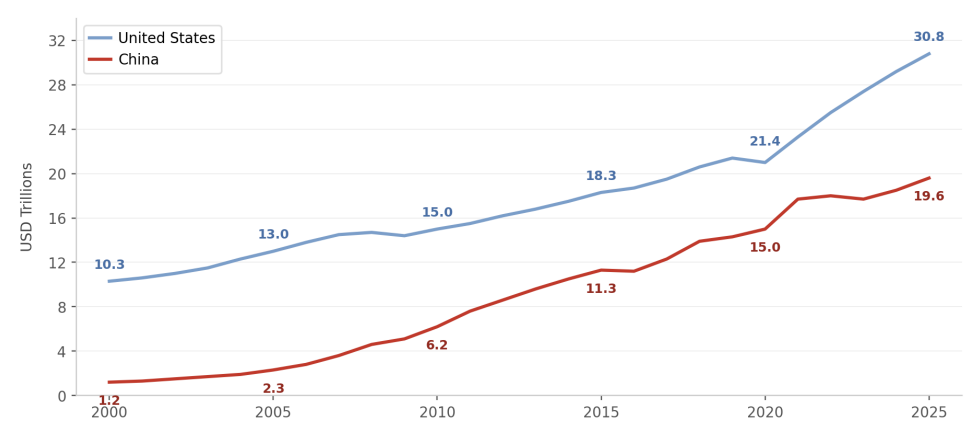

China's rise was faster and bigger than anyone anticipated. Between 2000 and 2025, China's GDP grew 16-fold, versus 3-fold for the United States. China went from 12% of the size of the U.S. economy to 64%.

US and China GDP Evolution

Source: Federal Reserve Bank and World Bank

The prediction about economic benefits panned out. The United States and many other countries outsourced much of their manufacturing to China and saw real gains in living standards as the cost of consumer goods fell. But the prediction that China's growth would make it democratic and politically aligned with the West never materialized.

China still runs on a culture, political system, and economic model that look nothing like what the West expected. Its worldview and development goals don't necessarily fit within the global order that Western powers, led by the United States, built after the World Wars. With 1.4 billion people and the world's second-largest economy, China was always going to look like a threat to U.S. supremacy.

A Paradigm Shift

After the Soviet Union collapsed in 1991, the great powers entered a long stretch of relative peace, with most countries operating under the diplomatic order the Western bloc had built after the World Wars, loosely organized around cooperating toward global development and well-being.

In democratic countries, with no major geopolitical threat looming, government priorities tracked what voters wanted most: a better quality of life, which tracks closely with economic efficiency. We watched Germany, an enemy of Russia in both World Wars deepen its dependence on Russian gas to cut energy costs and hit environmental targets. The United States flagged the geopolitical risk and leaned on Germany diplomatically to reverse course. Economic logic won out anyway. Voters would rather cut their cost of living than hedge geopolitical risk, and what voters want wins elections. That episode captures the mindset of the era well: economic optimization was the supreme goal of nations.

In recent years, two major developments forced the world to reshuffle its priorities. The first was the outbreak of war between Russia and Ukraine, stoking fears of Russian expansionism across the European Union and deepening the West's broader frustration with Russia's disregard for the diplomatic norms it expects other nations to follow. The second was Trump's return to the American presidency and the rollout of his “America First” policy, which made the rivalry with China far more explicit and abandoned the long-standing premise that the United States was responsible for defending the entire Western bloc, without asking much in return.

Then, seemingly overnight, national security started outranking economic efficiency. Germany stopped buying Russian gas, at least directly, rather than keep funding the war machine advancing on the EU. The United States banned the sale of advanced technology to China. American companies will earn less because of it, but they'll stop fueling the rise of the country threatening to take over as global leader.

This isn't just a shift in how politicians and diplomats think. Ordinary people have grown more aware of geopolitical conflict too, and are acting on it. Shortly after the invasion of Ukraine, British port workers refused to unload Russian oil with no legal obligation to do so.

Putting national security ahead of economic interest might feel odd to anyone alive today, but it's actually how most of human history has worked. During the World Wars, a French citizen would never have bought Nazi products just because they were cheaper than the French alternative. The last few decades were the exception and that exception looks like it's ending.

What We Expect for the Future

The push for national security will lead every country to try to cut its economic dependence on politically misaligned nations either by nationalizing parts of its supply chain or by developing suppliers in countries that pose no threat. That will likely shrink global trade flows, and with it, growth will slow and inflation will run higher, as production costs rise once economic efficiency stops being the only thing driving business decisions.

The U.S. and China both tend to double down on their spheres of influence closer to home, since geography matters enormously in military terms. Projecting military power over long distances is expensive and risky it depends on complex logistics with far more vulnerabilities than operations closer to home. Hence the logic of never letting a neighboring country slip into a rival's orbit.

This kind of cold-war competition for influence can actually create opportunities for developing countries. One option is staying neutral, preserving trade relationships with whichever nation offers the best terms, as Switzerland did even through the World Wars. Another path is to quietly auction off one's loyalty, trading political alignment for financial assistance, technology transfers, and military protection, the way many countries did during the Cold War between the Soviet Union and the United States.

Expect the technological race to intensify too, along with investment in the infrastructure a military conflict would require a risk that never really goes away and has been getting more explicit. This race runs independent of either side's stated intentions. The weaker side fears the stronger one's power and races to close the gap; as it does, the stronger side fears being overtaken and accelerates its own development to defend its lead. So even with purely defensive intentions on both sides, the competition for economic and military power keeps going.

None of this is new. It hasn't been part of our own lived experience, but history is full of episodes just like it.

Impact on Investments

Since these conflicts can hit the economy hard broadly, or concentrated in specific sectors, we've started factoring them into how we evaluate opportunities.

Traditional fundamentals still hold. We still want to invest in companies with real competitive advantages and high profitability, but we've started asking whether a business is exposed to potential sanctions or tariffs.

The risk matters most for export-oriented companies. If a company's home country gets hit with sanctions or tariffs, it can lose customers or be forced to cut prices to absorb the new costs. In these situations, having a moat doesn't guarantee protection. Under a full sanctions regime, a company can lose sales even as the sole producer of something with genuinely inelastic demand. Nvidia, for instance, is barred from selling its most advanced chips to China, after the U.S. government moved to restrict access to cutting-edge technology with potential military use.

Domestically focused companies tend to hold up better. They can even benefit if a good chunk of their competition comes from imports, if their own country slaps sanctions or tariffs on other nations, competition thins out and these companies capture the resulting gap in the local market.

There can also be indirect hits to an entire economy if one important sector gets caught in the crossfire. If Brazilian agricultural exports took a hit, for example, the whole country would feel it.

Fortunately, Brazil sits far from the center of today's geopolitical conflicts, and the odds of getting badly hit by sanctions or tariffs are low. If anything, we're among the countries positioned to benefit as others hunt for trading partners with no geopolitical baggage. A recent example: the EU-Mercosur free trade agreement, under negotiation for decades and now on the verge of taking effect, which only got over the finish line because the EU wanted to cut its own dependence on the United States.

Right now, our portfolio carries very little geopolitical risk. Even so, we think it's prudent to start tracking these global developments closely, and to apply an extra layer of caution when evaluating opportunities in sectors that could be considered strategic.