The Future of Indebted Countries

Dear investors,

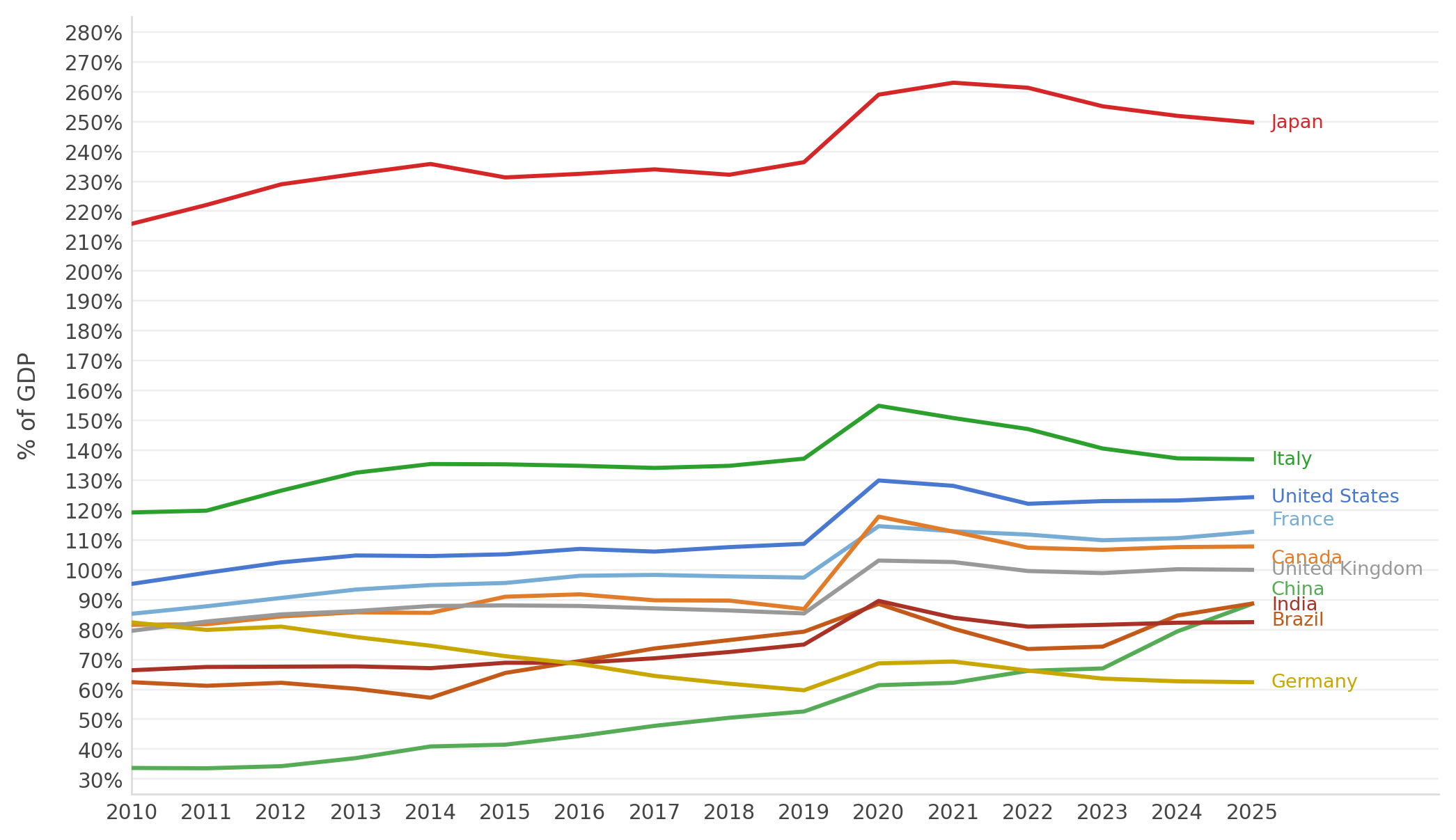

Brazil's public debt problem is well known, and it has gotten meaningfully worse in recent years. Between 2010 and 2025, our public debt climbed from 62.4% to 88.7% of GDP. Brazil isn't an outlier, though over the same period, several other nations have piled on debt too. Among the world's 10 largest economies, Germany is the only one moving in the opposite direction.

Public debt of the 10 largest economies

Source: IMF Data- April 2026 WEO

This wave of government leverage can't climb forever. The key questions: how long can this run, what would reverse it, and what it means for investments.

How We Got Here

Each country has its own story of how its debt got this large, but two common threads explain most of the trend: crises cushioned by government spending, and political resistance to fiscal adjustment.

For decades, governments have leaned on the Keynesian playbook for economic shocks: the state steps in as a counterweight to private markets during a crisis, ramping up public spending when private spending drops too sharply. The idea is that direct intervention avoids recessions, or at least softens the blow.

This played out on a massive scale during COVID-19. Countries rolled out stimulus programs to offset the income lost to lockdowns, funded by a jump in public debt. A smaller, more recent example: governments cushioning the oil-price spike triggered by the closure of the Strait of Hormuz. Brazil recently rolled out diesel subsidies.

In theory, spending should come back down after the crisis passes, to unwind the stimulus and rebuild government coffers. In practice, it's easier to hand out benefits than to take them away, so that reversal rarely happens. Of the world's 10 largest economies, 6 still haven't returned to their pre-COVID debt levels.

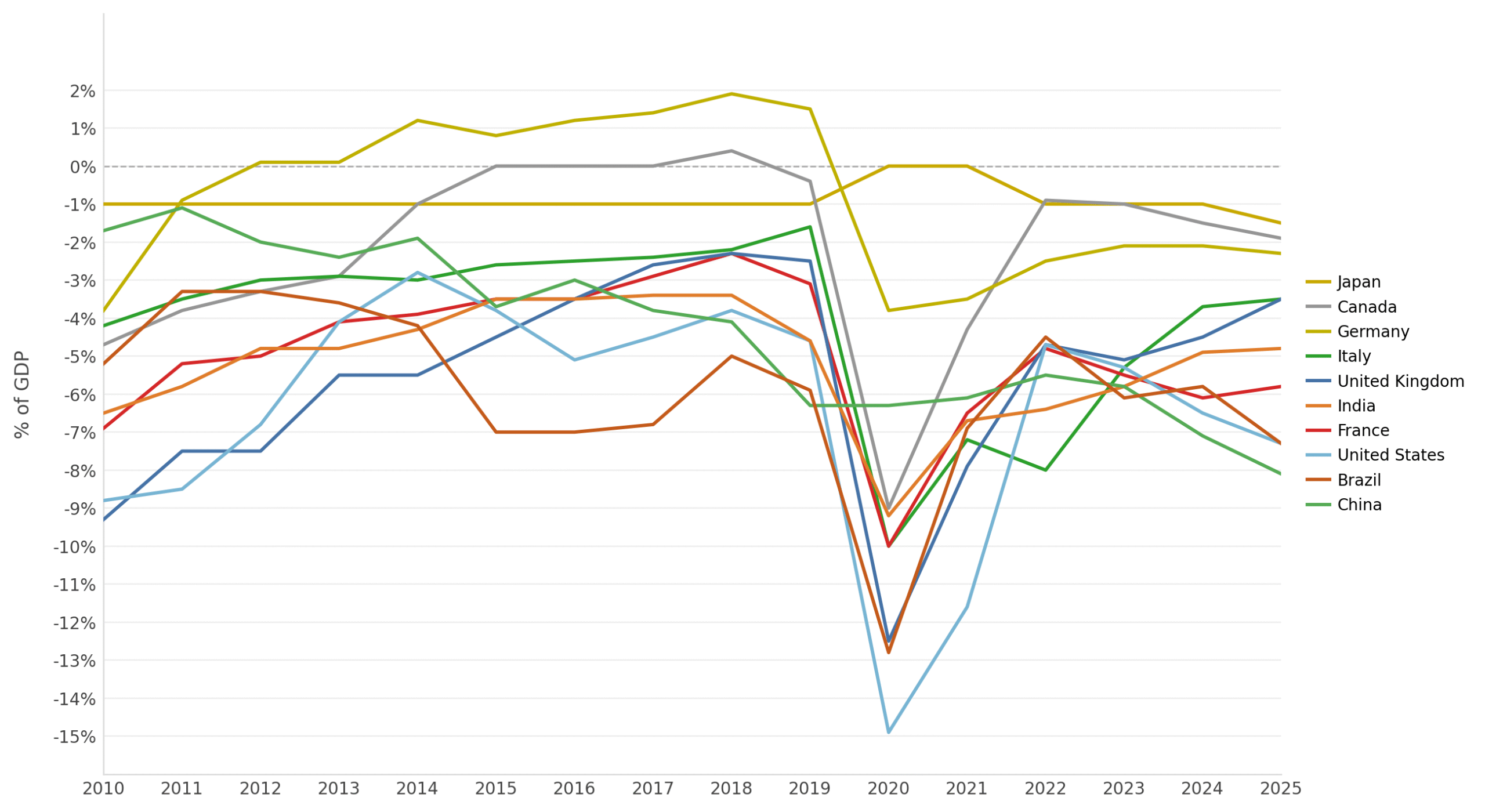

Political incentives point the same way almost everywhere: voters applaud bigger benefits and punish tax hikes. Where's the money supposed to come from? Campaign speeches skip that question fiscal accounting doesn't. Growing benefits generate fiscal deficits, and those deficits usually get financed with more debt.

Fiscal deficit (nominal) of the 10 largest economies

Source: IMF Data – April 2026 WEO

In an environment where economic growth outpaces the interest rate on public debt, some fiscal deficit is sustainable (in the simplified case where debt equals 100% of GDP, it stays stable when the deficit matches nominal GDP growth). Under that logic, the usual political urge to push spending to the edge of what's fiscally defensible, combined with the low-rate years between 2010 and 2021 made it easy to argue that rising deficits and debt were sustainable. The cracks started showing after 2022, when the illusion of permanently low rates faded and the cost of debt began weighing on the fiscal balance again.

This is the position Brazil and much of the developed world find themselves in today: high public debt, high interest rates, and popular resistance to spending cuts. Let's walk through what happens here.

What Comes Next

The best-case fix would be faster economic growth. With GDP growing quickly, debt gets diluted without any need for spending cuts. That's exactly how the U.S. worked off its debt after World War II American debt hit 121% of GDP in 1946 and fell below 40% over the following decades. Today it sits at 124% of GDP, without a world war in sight.

That's a hard trick to repeat, especially with demographic and geopolitical headwinds working against it. Instead of a post-war baby boom, most countries today are aging fewer working-age people, more pension spending. Instead of globalization and the growth tailwind that came from deepening trade ties, several countries are now prioritizing independence and national security. (We covered this in more depth in our March letter, “The New Cold War").

The other classic way out is old-fashioned austerity: spend less than you collect, and use the surplus to pay down debt. Economists have preached it forever; politicians have ignored it just as long. It's obvious advice for any household or business in financial trouble, but a tough sell for leaders who answer to voters with little patience for economics and even less for benefit cuts. Historically, it's been the exception, not the rule.

The other classic way out is old-fashioned austerity: spend less than you collect, and use the surplus to pay down debt. Economists have preached it forever; politicians have ignored it just as long. It's obvious advice for any household or business in financial trouble, but a tough sell for leaders who answer to voters with little patience for economics and even less for benefit cuts. Historically, it's been the exception, not the rule.

A more extreme option is outright default, refusing to pay, or forcing a moratorium, since no supranational institution can compel a state to honor its obligations. The problem is what comes after: new debt gets harder to raise once credibility is gone; the financial system takes a hit as securities once seen as safe (and widely used as collateral) suddenly lose value; and the currency depreciates as foreign investors head for the exit. Given how severe that fallout is, we'd only expect countries with no other options to go down this road.

The likelier path is that governments fall back on subtler, historically well-worn tools: inflation and financial repression. Both require debt to be denominated in the national currency which covers virtually every economically relevant country today. The world's 10 largest economies hold more than 95% of their public debt in their own currencies.

Down the inflation path, governments print more of their own currency and use that artificially created capital to cover the nominal value of their debts. Since no real economic value comes from thin air, that currency issuance generates inflation and erodes the real value of everything denominated in it. In practice, it's a transfer of wealth from asset holders to the government a hidden tax by another name.

Financial repression works through subtler mechanisms that force the market to finance the government below what it would normally charge. A government might, for instance, issue a class of low-yield public bonds and require every pension fund in the country to hold a slice of its portfolio in them. Several of the Asian Tigers leaned on financial repression during their economic-miracle years. On a smaller scale, Brazil does something similar through mandatory FGTS contributions every formally employed worker is required to invest at rates barely above inflation, with real returns near zero, and that capital ends up financing public projects.

In short: faster growth is unlikely, and austerity is a political non-starter. Between the two options left, outright default, or inflation and financial repression it's almost certain governments choose the latter.

What This Means for Investments

The scenario we see as most likely won't necessarily trigger a major economic crisis. Governments will try to address the debt problem as gradually as possible what unfolds slowly tends to cause less disruption and carries less risk of a major shock. The concern isn't a sudden, catastrophic loss. It's how to position portfolios for a long stretch of inflation and financial repression without watching their value quietly erode.

The typical Brazilian investor's instinct, at the first sign of trouble, is to rotate into fixed income and real estate. In this scenario, real estate still holds up reasonably well but fixed income may be the more dangerous move. The two asset classes worth a closer look instead are commodities and equities.

Fixed income is the asset class most exposed to measures aimed at reducing the public debt burden, especially government-issued bonds in Brazil, Tesouro Direto. Fixed-rate bonds are the most exposed to inflation, which eats into their locked-in nominal return. Floating-rate bonds can suffer as monetary policy compresses the base rate. Inflation-linked bonds with a fixed real return (in Brazil, Tesouro IPCA+ / NTN-B) are the safest within sovereign fixed income, but not fully immune they can still be hit by direct intervention: a change to the inflation index used, a special tax regime, or liquidity restrictions. Creative legislators have no shortage of options.

More broadly, any asset whose value rests on cash flows fixed in nominal terms is exposed even ones unrelated to public debt. Private credit behaves much like public bonds under inflation and compressed rates; it's only spared from the direct interventions that specifically target sovereign debt.

The other asset classes hold up better because their value doesn't depend on the currency directly the currency is simply the unit they happen to be priced in. If the currency loses half its value, the price of real assets roughly doubles. That logic applies across consumer goods, commodities, real estate, and equities alike though each deserves its own caveats.

Commodities offer strong inflation protection but come with their own drawbacks. Prices swing on all sorts of unpredictable factors, and since commodities don't generate cash flow, their long-term returns tend to be fairly low. It's not the asset class we'd reach for if safety is the goal.

Real estate is a traditionally safe bet, but one that tends to deliver modest real returns. Outside of well-executed, property-specific theses (location-driven appreciation, or some other specific catalyst), long-term returns tend to hover close to the real base interest rate.

Equities are more nuanced. In principle, they hold up well against inflation a company's assets don't devalue along with the currency and they offer more attractive upside than real estate or commodities. But a stock's intrinsic value depends on the issuing company's future earnings, and the monetary policies at play here can hit different businesses in very different ways. Each case needs its own read.

The safest equities belong to companies with real pricing power the ability to pass through price increases to offset inflation and whatever else these monetary policies throw at them. That takes demand that isn't price-sensitive (low elasticity) and limited competition, backed by durable competitive advantages or other barriers that keep customers from walking away.

Not by coincidence, this profile overlaps heavily with what we look for in any environment. The most profitable companies over the long run tend to be the same ones that hold up best across a range of adverse scenarios.

In tougher times, the one tactical tweak we make to our usual value-investing approach is to lean harder into quality and be warier of bargains ordinary businesses trading well below fair value. There are moments when preserving value matters more than reaching for extra return.