Interest Rates and Capital Allocation

Dear investors,

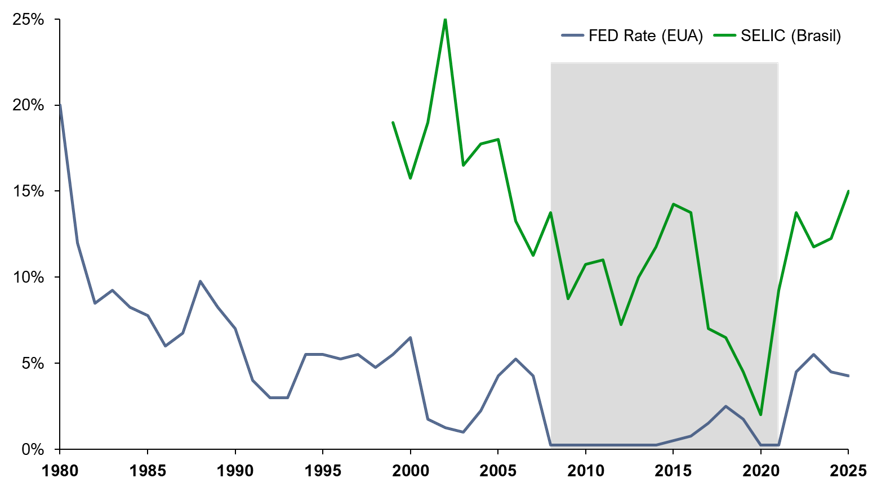

Between 2009 and 2021, the world lived through remarkably low interest rates. That decade of cheap money was fertile ground for “new businesses.” Venture capital funds proliferated, financing startups of every stripe. Mature companies pushed into international expansion, M&A programs, and new factory construction. At the peak of the hunt for alternatives to sagging fixed-income returns, even exotic asset classes emerged most notoriously NFTs, certificates of ownership for easily replicable digital images that traded an estimated USD 6 billion in January 2022.

Throughout 2022, central banks raised rates to combat inflation stoked by pandemic-era stimulus programs, and the era of cheap money came to an end taking the previous decade's euphoria down with it. In Brazil, the move was more modest, but in the same direction.

Evolution of Benchmark Interest Rates

Note: rates at end of each year. SELIC was created in 1999.

None of this was new. Capitalism has always run in cycles, and the benchmark interest rate plays a key role in shaping the behavior that drives those cycles. Below, we walk through this dynamic and share our view on where things stand today.

Interest Rates and Capital Allocation

In theory, investors should always seek the best possible use of their capital, weighing potential return against risk for every opportunity. In practice, many do something subtly different: the typical investor sets a return target they consider sufficient to meet their goals, then looks for the lowest-risk way to hit it. The distinction may sound minor, but it has real consequences for the broader economy.

The most convenient options are government bonds and low-risk private credit. They require little analytical effort, carry low volatility, and are accessible to virtually any investor. Their yields track the benchmark rate closely, and the market behaves quite differently depending on whether that rate sits above or below the return most investors consider adequate.

When rates are low, plain-vanilla fixed income stops being good enough, and appetite shifts toward alternatives that offer a shot at higher returns: risk assets, longer-duration projects, leveraged companies, ambitious business plans. There's never a shortage of people and companies looking for financing what's scarce is genuinely good opportunities to deploy capital productively in the real economy. When too much money chases too few ideas, underwriting standards slip. Marginal projects get funded and come off the ground. Later, a chunk of that investment crop turns into idle capacity, operating losses, and bankruptcies the hangover from a period when everyone paid more attention to upside than to risk.

When the benchmark rate is high, the opposite happens. Fixed income satisfies a large share of the market and soaks up a considerable portion of available capital. Most investors stop looking at alternatives, and new projects struggle to get financed. Beyond the scarcity of capital, few initiatives can offer a risk premium over already-high rates. Risk-asset investment slows, the economy grows more sluggishly, and unease sets in. But investors who avoid complacency can turn this into an advantage.

With opportunities abundant and competing capital scarce, active investors can afford to raise their bar allocating capital only to genuinely above-average opportunities, ones likely to face less competition down the road since few rival initiatives will get financed at the same time.

The Impact of Interest Rates on Consumption

Alongside these capital allocation dynamics, interest rates also have a direct effect on consumption. When rates are high, there's little incentive to take on debt to consume more. Some will still do so out of necessity or poor money management, but overall consumption tends to track the population's real economic capacity more closely, and grows more slowly. Low rates flip this dynamic.

Easy access to cheap credit pushes many people to spend beyond what they could afford in cash. The problem: credit expansion doesn't actually increase the population's long-term purchasing power. It simply pulls forward future consumption, in exchange for interest payments that shrink each person's lifetime purchasing power. The resulting growth spurt is temporary and bound to reverse.

From a corporate vantage point, this dynamic is hard to see while it's unfolding. What executives do see clearly is their own sales figures. When revenue grows, the natural read is that the business is thriving in a promising segment not that part of that growth is credit-fueled and likely to evaporate once the cycle turns.

This backdrop breeds optimism and sparks new ideas: capacity expansions, new ventures to meet rising demand. In other words, low rates simultaneously create investors hungry for risk premium and executives building plans on optimistic assumptions. It's a recipe for capital misallocation.

These cycles repeat over and over, even though nearly everyone involved investors and executives alike has seen the pattern before. Part of that comes down to psychological biases that are hard to shake; part of it is the sheer impossibility of predicting how long any given phase will last, combined with some investors' confidence that they can do exactly that. Believing they can call the next turning point, many keep pouring into risk assets too late in the upswing, and hold back too long in the downturn. That behavior pushes prices to excessively optimistic or pessimistic extremes, feeding the pendulum swing that defines economic cycles.

Finding Opportunities in Capital Cycles

Understanding capital cycles isn't hard. Neither is explaining one after the fact. The hard part is knowing when to act against consensus which, more often than not, is right.

A good starting point: the market pays far more attention to demand trends in a given sector visible in company revenues than to supply trends, which have to be inferred from investment volumes. Some sectors have supply capacity that adjusts quickly to demand swings. Capital-intensive sectors typically don't have that flexibility building a new factory can take years. In these businesses, capital cycles matter far more.

When demand is booming and everyone is pouring money into capacity expansions, that's usually a bad time to invest in the sector. Sentiment will be upbeat, but odds are the sector is quietly building excess capacity that sits idle once the cycle turns, intensifying competition as companies scramble to keep their assets utilized, and eroding profitability across the board.

The best time to find good opportunities is when demand is weak, expansion investment has dried up, sentiment is pessimistic, and assets are cheap. If there's no structural reason demand can't recover, it probably will eventually and when it does, supply becomes the bottleneck limiting sales volume. Basic supply and demand then take over: prices rise, and sector profitability recovers.

The catch: this kind of thesis takes patience. It can take years for the cycle to turn and the expected scenario to play out. Our investment in Marcopolo is a good example we bought our first shares at the end of 2019 and waited more than three years for sector profitability to improve meaningfully. But the thesis has delivered an average annual return of ~36% to date (we still hold part of the position), so the wait paid off.

What Phase of the Cycle Are We In

There's no single capital cycle governing the whole economy. Each sector, in each region, runs on its own clock, with highs and lows hitting at different times so this analysis has to be done case by case. That said, an entire country's economy runs on the same benchmark rate, and long stretches of high rates tend to push several segments into a downturn at once.

Sometimes sector-specific dynamics override the influence of interest rates altogether. AI infrastructure is a good example: massive investment is pouring in even with rates elevated. In 2025, the hyperscalers Microsoft, Amazon, Google, Meta, and Oracle invested USD 400–450 billion, with a further USD 600–800 billion expected in 2026. The capital deployed may not be excessive given the technology's potential, but this sector is certainly not in a down cycle.

Meanwhile, several more traditional segments of the economy haven't seen anything as exciting lately, and are feeling the weight of what is now the fifth year of high rates a backdrop shared by Brazil and the world's major economies alike. It's a good time to hunt for pockets of capital scarcity that could turn into tomorrow's supply bottlenecks. Last month, we bought shares in a company that fits this opportunity profile well. We expect to disclose the new position at our next investor meeting.