Dear investors,

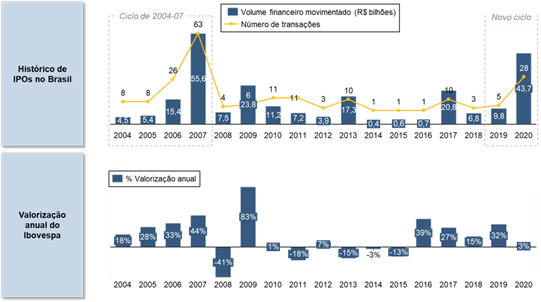

The Brazilian capital market is experiencing a new cycle of IPOs[1]. Between 2019 and 2020, we had 33 companies debuting on the stock exchange, which moved a total of R$ 54 billion. In 2021, we already had 9 IPOs[2], and there are more than 30 offers under analysis by the CVM. To give you an idea, between 2014 and 2016, we had only 3 IPOs!

This cycle is only comparable to the period from 2004 to 2007, when there were a total of 105 IPOs and a total turnover of R$ 81 billion.

Considering the similarity between the two periods, we brought an analysis of the historical performance of the IPOs of this cycle from 2004 to 2007 to try to answer the following question: is it worth investing in IPOs?

The chart below shows the history of IPOs in Brazil between 2004 and 2020 and illustrates the numbers cited in the introduction to this letter.

Graph 1 – History of IPOs in Brazil and annual appreciation of the Ibovespa

The fact that more companies are managing to go public is excellent for the Brazilian capital market, as it means that entrepreneurs are managing to raise funds to finance expansion plans, which, in turn, generate new jobs and benefit the economy.

From the point of view of us investors, IPOs increase the range of investment opportunities. In a country with few listed companies, newcomers to the stock market are very welcome.

As we mentioned in the November/2011 letter, Brazil had until that moment 316 companies listed, a very low number when compared to countries with economies of similar size to ours, such as India, Canada and Australia, with 5,541, 3,948 and 1,967 companies listed[3], respectively.

Despite these benefits, investors need to be selective in choosing assets. It is no coincidence that the periods with the highest volume of IPOs are precisely those in which the stock markets operate on the rise (see graph 1 above), as this is when entrepreneurs understand that they will be able to sell their shares at valuations attractive.

This is an important point: if entrepreneurs, who know much more about their own company than any investor, understand that it is a good time to sell, it is necessary to be careful in selecting what may in fact be a good investment.

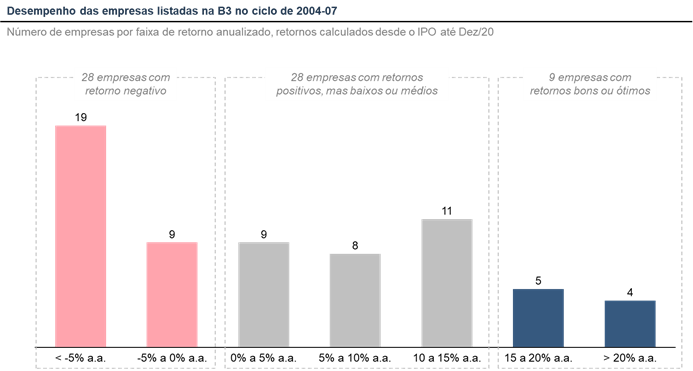

To illustrate this point, we brought an analysis of the return of newcomers on the stock exchange in the cycle from 2004 to 2007. At the time, the situation was very similar to the current one: dispute between investors to participate in IPOs and huge valuations of shares in the days of debut.

Almost 15 years after that period, of the total of 105 listed companies, only 65 are still public. Of the 40 that were delisted, 22 were acquired or went through an M&A process, 15 went private through a takeover bid and 3 went bankrupt.

Of the 65 companies that remain listed, the average performance is not very positive. Only 26 companies surpassed the Ibovespa in the period.

More alarming data is that 28 companies (43% of those still public) had negative returns. Among these, there are cases of builders such as PDG, Gafisa, Viver and CR2; banks like Indusval and Pine; the mining company MMX (OGX, the most famous company in the X group, made the IPO in 2008). In all these companies there was significant capital loss, in some cases up to 99%.

Of the others, 28 had low or medium returns (between 0 and 15% per year), and only 9 had good or excellent return levels (above 15% per year). The graph below illustrates this data:

Graph 2 – Dispersion of returns of listed companies between 2004 and 2007

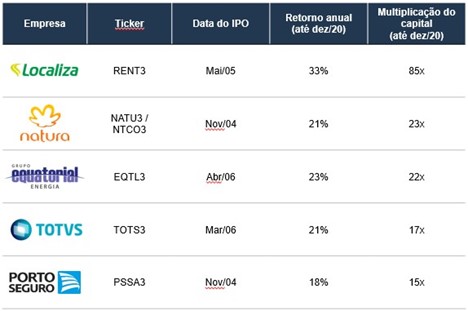

Despite the average of poor results, the window from 2004 to 2007 brought excellent companies to the stock exchange, which were able to bring significant value creation to their shareholders. Among them, highlights for Localiza, Natura, Equatorial, Totvs and Porto Seguro, all with multiplication of invested capital by at least 15x.

Graph 3 – Most successful IPOs of the 2004-07 cycle

Source: CapitalIQ, Arctic Analytics

If history repeats itself, which seems likely to us, the cycle of IPOs we are living now should bring companies with huge performance dispersion. Discipline to select the best opportunities, investing in good companies that are negotiated at fair prices is what makes the difference in the long term.

[1] Initial Public Offering (“initial public offering” in English, or “initial public offering” in Portuguese) represents the first time that a company's shares are offered to the market. After the IPO process, it becomes a publicly traded company

[2] Until 11/Feb/2021

[3] In 2017