Why invest in stocks outside Brazil?

Dear investors,

Our investment track record is almost entirely in the Brazilian stock market. While a large portion of Brazilian investors believes our exchange is not a good investment environment — due to the country’s political and economic turbulence and the well-known comparison of the Ibovespa’s return against the CDI over recent decades — we hold a different view. Although a passive equity investment strategy offers little in the way of attractive prospects, there is ample room to generate good returns through active management. That is the strategy we have successfully executed over the past decade. Recently, however, we have begun looking more beyond Brazil.

In 2022, the topic of international investing gained some prominence, as several multi-market funds invested in foreign economies and even the general public began seeking investments abroad through new brokerages that offered accounts for trading overseas. However, that movement was driven by concern about the Brazilian economy and the consequent desire to diversify into other geographies, while our motivation is quite different. We will explain why we still like the Brazilian stock market and why, even so, it made sense for us to also seek investments in other countries.

The good side of the Brazilian stock market

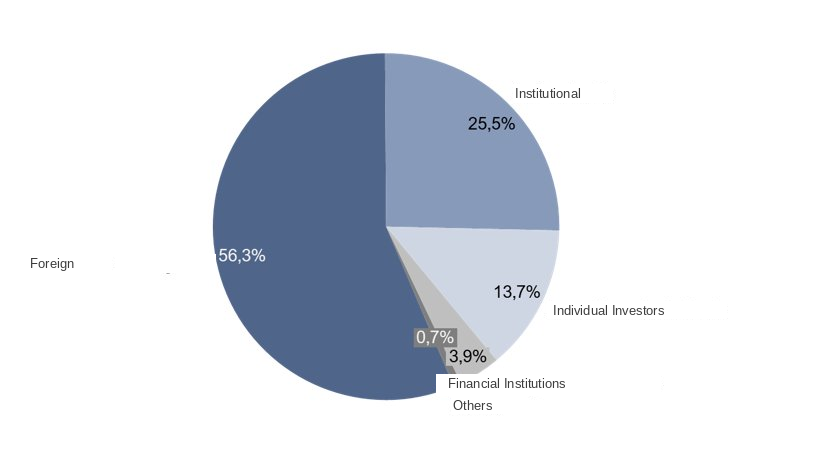

Investing in equities is a competitive activity. To achieve returns above the index, one must be more right than the market average. As in any competitive dynamic, the first thing a participant would want to know is who the other competitors are and how challenging it is to beat them. So an important question is: who invests in the Brazilian stock market? A good reference for this information is the share of each type of investor in the total volume traded in the equity spot market, reported monthly by B3 itself:

Investors in B3's Total Monthly Volume (April 2024)

For foreign investors, Brazil is a completely peripheral market. The total value of companies listed on the Brazilian exchange represents ~2% of the global equity market, and only ~70 companies are worth more than USD 2 billion. Below that threshold, the American market classifies stocks as small caps. In other words, for an American institutional investor, we are a small emerging market of small caps. Many of the foreigners who invest in Brazil do so as part of a portfolio diversification strategy into emerging markets, assessing the average valuation level of the exchange and the expected growth of the Brazilian economy relative to developed economies. Few will conduct in-depth analyses of individual Brazilian companies.

Individual investors have varied profiles but generally lack deep technical knowledge and do not have much free time to dedicate to stock analysis. Most conduct superficial analyses or follow the recommendations of some subscription service that provides market research.

What remains are institutional investors and financial institutions. These are indeed professional, qualified investors with dedicated teams and information systems. However, this category encompasses both equity funds and other types of funds — multi-market funds in particular — and a large portion of them do not pursue active equity management strategies. They may track the index portfolio and make tactical variations around it, or pay more attention to the balance between equities and other asset classes than to selecting the best individual stocks.

In other words, fewer than 30% of participants in the Brazilian equity market (and potentially far fewer) are actively conducting in-depth analyses of specific companies. Moreover, many investment funds still face the problem of having a volatile investor base that panics when market sentiment deteriorates and begins making redemptions, so that even if the fund manager believes it is time to buy more, they may be forced to sell in order to return money to their shareholders.

This is the competition we face in Brazil. The typical investor active in our exchange pays less attention to the details of listed companies than to the country’s macroeconomic environment. This generates stock price volatility that is, at times, uncorrelated with the expected financial results of each company. This is the perfect environment for fundamentalist investors to operate in: a market where stock prices fluctuate considerably around estimates of each company’s intrinsic value, which is precisely the condition required for there to be opportunities to buy cheap and sell dear.

The bad side of the Brazilian stock market

On the other hand, there are three characteristics we consider negative in our stock market. The first is the small number of assets. Today, there are 340 companies listed on the B3 and only 214 of them with daily liquidity above BRL 500,000 — still considered quite low, but which allows us to operate with small positions. This significantly limits the universe of opportunities we have to evaluate.

The second negative factor is that the Brazilian economy is not strong in sectors that simultaneously offer high profitability and globally competitive advantages. For example, many of our listed companies operate in commodity sectors, characterized by volatile results that make it difficult to estimate their fair value with confidence. Others are highly regulated or state-controlled, with the consequent unpredictability brought by potential political interference. Removing from the list the businesses in sectors we consider uninteresting, between 100 and 150 companies remain. It is quite a small set of opportunities and, consequently, the number of excellent investment theses one can find within it is quite limited.

The third aspect is Brazil’s legal uncertainty, particularly regarding tax matters. In many businesses, even with correct and diligent executives, significant legal disputes arise over the amount of taxes owed by the company. The discomfort this creates for investors is that, in many investment theses, there is a chance the company could lose a relevant portion of its value if the court ruling goes against its position. Litigation tends to be complex, with highly uncertain timelines and outcomes. To illustrate how disruptive this is: in one particular investment thesis, we evaluated a tax dispute that had been ongoing for more than 10 years. We read more than 500 pages of court records, held meetings with several lawyers, and the result of all that work was an estimate of the order of magnitude of the losses associated with each possible outcome, a very vague sense of the likelihood of each scenario materializing, and the expectation that the case would still take years and years to resolve.

Why we started looking abroad

The balance of the good and bad aspects of the Brazilian stock market still seems positive to us. It offers good investment opportunities, with some regularity, for those willing to do careful work in selecting the companies in which to invest. However, international exchanges caught our attention because an atypical window of opportunity emerged.

What developed countries are facing now are inflationary crises very similar to Brazil’s, with the difference that Brazil began fighting inflation about a year before the United States and Europe. Thus, while our central bank is already cutting interest rates, the central banks of other countries are still at a stage similar to where Brazil was in the second half of 2023: at the peak of interest rates, debating how long they will need to maintain them or whether any additional increases will be necessary.

Investors’ reaction to this global rate-hiking scenario was the same as what we saw happen in Brazil: there was a major migration of capital from equities into fixed income securities and, as a result, stock prices fell under the selling pressure. As a result, several exchanges are trading at valuation levels considerably below their historical averages, the same scenario we see here in Brazil. The current supply of cheap stocks is a global phenomenon.

Amid this turbulent macroeconomic environment, it is worth noting that not everything is cheap. Amid the attractive average valuation, there are bargains and companies trading at bold prices. A notable example is the price level of American big techs. They are undoubtedly companies of excellent quality and great potential, but it is far from obvious to claim that valuations in the range of 25 to 60 times price/earnings represent great bargains.

Is investing abroad more difficult?

The major disadvantage of investing abroad is having to deal with exchange rate risk, which is like the price of commodities: impossible to predict. In theory, the relationship between two currencies should vary only as a function of the difference in inflation between the two currencies, but in practice the real exchange rate can spend very long periods far from that theoretical equilibrium point. For example, the analysis below shows the relationship between dollars and reais (USD/BRL) since 1999, when Brazil adopted the floating exchange rate regime. The red line is what the exchange rate should have been over time if the theory worked perfectly, and the blue line is the actual exchange rate.

Real vs. Theoretical Exchange Rate (USD/BRL)

The analysis serves as a reference for where the exchange rate should gravitate in the long run, but does not help much in predicting what the exchange rate will be in the coming years. The problem with this is that a large exchange rate movement can undermine the return of an otherwise successful investment from the perspective of the investee company’s local currency, if the conversion of capital back into reais is made at a rate far worse than the one in effect when the investment was made.

We take two precautions to mitigate exchange rate risk: the first is the good old margin of safety — to invest outside Brazil, we require a larger discount in the share price relative to its fair value to compensate for the extra risk; the second is to avoid investing in cyclical businesses abroad, since the exchange rate could be unfavorable at the point in the sectoral cycle when it would be appropriate to sell the shares.

Aside from the exchange rate problem, there are no major obstacles to investing in other countries, as long as those selected have stable economies and business environments we are capable of understanding. The type of fundamental analysis we conduct is applicable to any geography, and today physical location matters little when it comes to gathering data and communicating. Scheduling video calls with executives in London is just as simple as scheduling them with executives in São Paulo.

The advantages of looking at the whole world

The main impact of looking beyond Brazil is that we have expanded our universe of possible investments from 214 companies to more than 25,000 listed stocks around the world. The advantage is statistical: the chance of finding extraordinary opportunities in a sample of 25,000 stocks is far greater than finding something extraordinary among 200 local stocks, in the same way that it is easier to find a person standing 2.20 meters tall in a group of 25,000 people than in a group of 200. This allows us to be far more rigorous in our selection criteria while still expecting to find stocks that meet our requirements.

Another characteristic that works in our favor is that the equity markets of developed countries are much larger than Brazil’s, both in terms of the size of the companies and the size of the investment funds that operate in them. In the American market, equity funds with less than USD 1 billion are considered small, and below USD 10 billion they are still considered mid-sized. That is why companies worth less than USD 2 billion are classified as small caps.

Today, the Ártica Long Term manages approximately BRL 250 million (~USD 50MM) — a minuscule size by global standards, which translates into a relative advantage for operating in developed markets. For us, it is a worthwhile investment of time to conduct an in-depth analysis of a company in which we can allocate 10% of our portfolio (USD 5MM), with daily liquidity above USD 100,000. For a typical American fund, stocks of that size are too small to even be worth the effort of analyzing. In other words, it is not the good American fund managers we will be competing against when we evaluate stocks in companies worth USD 1 or 2 billion. Since what matters most to us is the return generated for our investors, we will continue to make the most of the advantage afforded by our current size and to seek out the least competitive environments possible.

What we have done so far

For approximately six months, we have been looking at stocks in places with business cultures we already have some familiarity with: the United States and Western European countries. So far, we have invested in two companies listed on the London Stock Exchange. The fact that both are British was a coincidence — we did not find them by targeting England specifically.

One of them is a small cap that fits well within the typology we described, with a market cap of ~BRL 600 million and daily liquidity of ~BRL 750,000 — too small for most British funds to care about. It has grown at an average of 21% p.a. over the past five years and maintained an average return on equity of 15% p.a. in British pounds. We bought shares in this company at a valuation of approximately 5x Price/Earnings.

The other is a large cap worth tens of billions of dollars. It is a mature global business that no longer has significant growth, but maintains good profitability, strong cash generation, and is currently trading at 7.5x Price/Earnings, while it used to trade between 10-15x Price/Earnings before the inflationary crisis. In this thesis, what attracted us was not exactly those price references, but the fact that the chance of losses is low and there is potential for significant appreciation of the business within a few years, due to changes in the sectoral context.

As you may have noticed, we are not yet ready to disclose which companies these are, as they represent small positions in our portfolio and we may still add to them. If they grow to a relevant size, we will provide more details about them in a future letter.