Dear investors,

Source: Aurum Research Limited

The result is the same in Brazil

Source: Aurum Research Limited

The result is the same in Brazil

Source: CVM, Ártica analysis

Why does it happen?

Source: CVM, Ártica analysis

Why does it happen?

Today, the functioning of the financial market in Brazil is still unclear to most individual investors. For example, have you ever wondered how the big brokerages make money, even though they offer free services to individuals, and what are the implications of this business model for investors?

One of the main sources of revenue for brokers is to charge trading commissions on investment funds available on their platform, which commonly amount to 50% of all fees paid by investors to fund managers, over the entire investment period.

This business model has two relevant implications. The first is that brokerage advisors, who serve clients for free, have the incentive to recommend the products that pay the highest commissions, and not necessarily the ones that are best for each client. The second implication is that the remuneration of managers, who effectively work to improve the profitability of investments, is reduced by half. The rest is left to the brokerage houses, which provide the convenience of a good application and the ability to centralize investments in a single account, but do nothing to improve the return on invested capital. It's like the packaging costs the same as the product inside.

As a result of this structure, managers seek to compensate for the rate reduction by increasing the fund's capital under management. However, this creates a burden for its investors, as the larger the fund, the more difficult it is to achieve excellent returns. This will be the subject of today's letter.

Smaller funds, higher returns

The fact that small funds have higher average returns than large funds is well known in the financial market. Although the subject is little commented on, there are several studies and articles that prove the point¹.

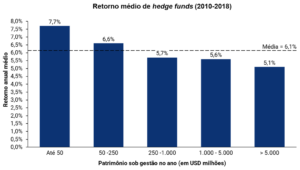

Aurum, a manager of funds of funds (funds specialized in selecting and investing in quotas of other funds), analyzed the returns of hedge funds between 2010 and 2018. At the beginning of the period, there were around 1,700 funds that had USD 1.7 trillion under management, and at the end of the period there were 3,800 funds with USD 3.2 trillion under management. They found a clear correlation between fund size and profitability: while “micro” funds (less than USD 50 million under management) had an average return of 7.7% per year, “mega” funds (more than USD 5 billion under management) had an average return of 5.1% per year. The difference is bigger than it seems: USD 100 thousand invested in “mega” funds would become USD 156 thousand at the end of the 9 years, while the same investment in “micro” funds would reach USD 195 thousand, a final value 25% higher.

Source: Aurum Research Limited

The result is the same in Brazil

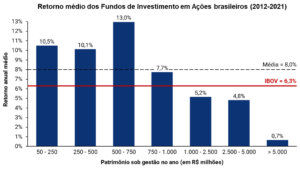

To verify whether this return difference also applied to equity funds operating in the Brazilian market, we collected data from 1,049 investment funds listed on the CVM with net worth from R$ 50 million for the period from 2012 to 2021 and compared the average return between different size ranges. The result was similar. There is no return erosion until the R$ 750 million range, but the average return starts to reduce after that. While funds smaller than R$ 750 million had an average return of 10.61%, those larger than R$ 5 billion had a return of 0.66%. That is, R$ 100 thousand invested in large funds would become R$ 107 thousand over these 10 years, while the same investment, in small funds, would reach R$ 274 thousand, leading to a final value 157% higher.

Source: CVM, Ártica analysis

Why does it happen?

Huge deals are quite rare. For example, in Brazil we have 366 listed companies² on the stock exchange, of which 253 are worth less than R$ 5 billion, 95 are worth between R$ 5 and 50 billion and only 18 are worth more than R$ 50 billion. Similarly, there are fewer investment opportunities in which it is possible to invest billions of reais, due to the size of the company or the liquidity of its shares in the market, than opportunities to invest tens or a few hundred million.

At the same time, fund managers typically only invest time analyzing opportunities that make it possible to invest a minimum amount. The larger the fund, the greater the minimum amount required, and the greater the number of shares that do not pass this filter and are ignored. A fund that only invested in shares with a market value above R$ 5 billion would analyze only 113 shares on the Brazilian stock exchange, disregarding the other 253, which represent 69% of possible opportunities.

As a result, large funds compete among themselves for the restricted number of investment opportunities that can absorb large volumes of capital. This fierce competition among professional investors makes it more difficult for large asymmetries to arise between the price and intrinsic value of each asset.

Consequently, the chance of these funds having very high returns ends up being smaller.

In contrast, there is far less competition for small opportunities and, in some cases, competition comes from non-professional investors, who are more likely to make mistakes and misprice the analyzed stock. So it's easier to find small caps (stocks with low liquidity, usually of smaller companies) undervalued in the market and, in addition, small caps tend to have higher returns than large caps in the long term³, as they tend to have greater growth potential and more agile and efficient management structures. Funds that can invest in companies of this type have an advantage in the search for higher returns.

Our plans

We are quite realistic with the fact that our investment strategy would not bring the same level if we had billions under management. The size threshold at which we have a good chance of continuing to hit our profitability target is not precise, but we do know that it is somewhere between R$ 500m and R$ 1bn. As a result, we made two decisions.

The first is that, when we start having difficulties finding good investments due to the size of the fund, we intend to close it to new investors, because, in addition to investing most of our personal assets in Ártica Long Term FIA, there is also capital relevant from various friends and family. Thus, both through professional ethics and personal relationships, we have a deep commitment to monetize this capital in the best possible way.

The second decision was not to distribute the Ártica Long Term FIA across platforms. We prefer to raise money directly and avoid the “packaging cost”, guaranteed once the fees paid by our investors are allocated to the management structure, which is what generates a return. The impact of this is quite large: we managed to sustain the same structure with half the assets under management that would be necessary if we paid distribution commissions.

In addition, we like to meet and maintain close contact with our investors. Capturing directly has the added benefit of allowing us to continue this practice. We have sought to be increasingly transparent about our investment philosophy and market vision: we started to carry out lives on the themes of the monthly letters (every first Wednesday of the month at 7:00 pm) and, also, presentations of quarterly results, in exclusive online meetings for our investors.

If you have any suggestions on what else we could do to improve communication with you, please email us at [email protected] . We are happy to hear new ideas!

¹ Gao, Chao; Haight, Tim and Yin, Chengdong, Size, Age, and the Performance Life Cycle of Hedge Funds (September 2018); Chen, Joseph S. and Hong, Harrison G. and Huang, Ming and Kubik, Jeffrey D., Does Fund Size Erode Mutual Fund Performance? The Role of Liquidity and Organization (May 1, 2004)

² B3 data on 07/30/2022, excluding listed companies that have no shares traded.

³ We published a letter about investments in small caps in September 2021, which is available at https://articainvest.com.br/cartas/investimento-em-small-caps/