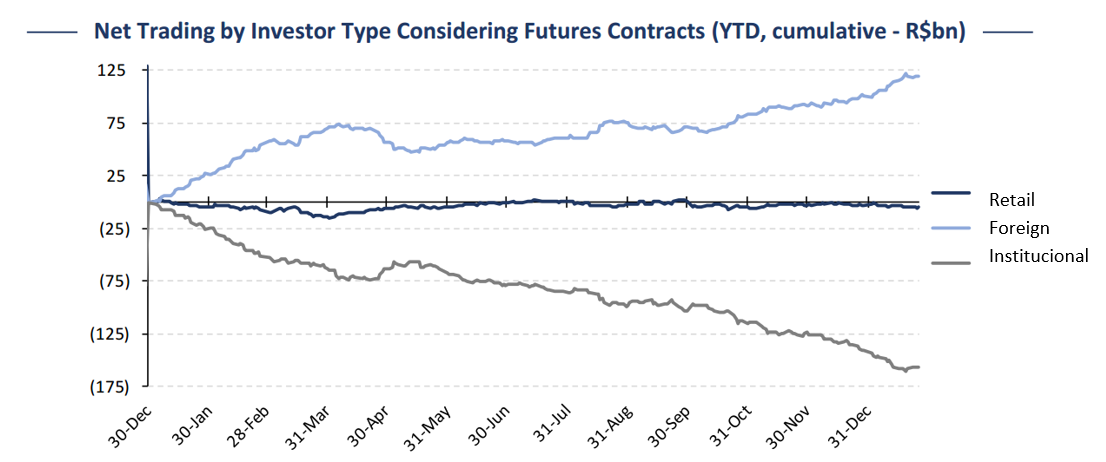

Dear investors, One of the sayings repeated over and over again by Charlie Munger, the Berkshire Hathaway partner who turned 99 this month, is that "To the man with a hammer, every problem looks like a nail." In its always laconic style, it is a criticism of the tendency to see the world in an overly simplified way, trying to explain everything through very restricted ideas, instead of trying to understand the nuances and complexities of each situation. With all the turbulence that Brazil has been going through, the public of investors has been closely following every news, no matter how small, about economics and politics. We were no exception. We've devoted more time than usual to these topics in recent months. However, we have the impression that newspaper headlines have been given more weight than they should in the decisions of Brazilian investors. The news has been the “hammer” of the market, considered as a relevant factor in estimating the probable future of the economy even when it has a very speculative character or very limited impact. Meanwhile, foreign investors bought around R$ 120 billion worth of shares on the Brazilian stock exchange in the last 12 months, sold by local investors. In other words, foreigners are “betting” that the future of our economy will be better than Brazilians themselves believe. Only one side can be correct.