A decade of investments

Dear investors,

Ten years ago, on June 27, 2013, we founded an investment club called Arcádia, with initial capital of BRL 126 thousand. At the time, the goal was to pool efforts to better manage our stock investments, since we all worked in investment banking and our free time was insufficient for each of us to manage our investments separately.

The strategy worked. We began generating strong results, grew our investments, and also received contributions from friends and family. By end of 2014, we had BRL 6 million under management — still tiny compared to investment funds. With high returns and some new contributions, by end of 2018 we reached BRL 46 million in assets under management, enough for us to decide to found a professional asset manager and convert the club into an investment fund. This is the story of how Ártica Asset Management was born and how the Arcádia Club became the current Ártica Long Term FIA, which completed 10 years of history last week.

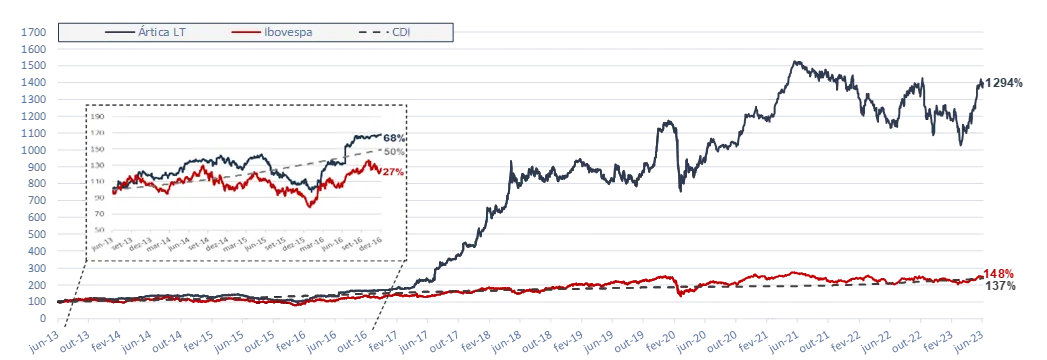

We closed our first decade of investing with a cumulative return of 1,294% through 06/30/2023, corresponding to an average annual return of 30% per year.

Historical Unit Value of Ártica Long Term FIA 11

In this letter, we will share some episodes and lessons our firm experienced along the way that helped us consolidate the investment philosophy we follow today.

Investment theses mature in a non-linear fashion

Unipar

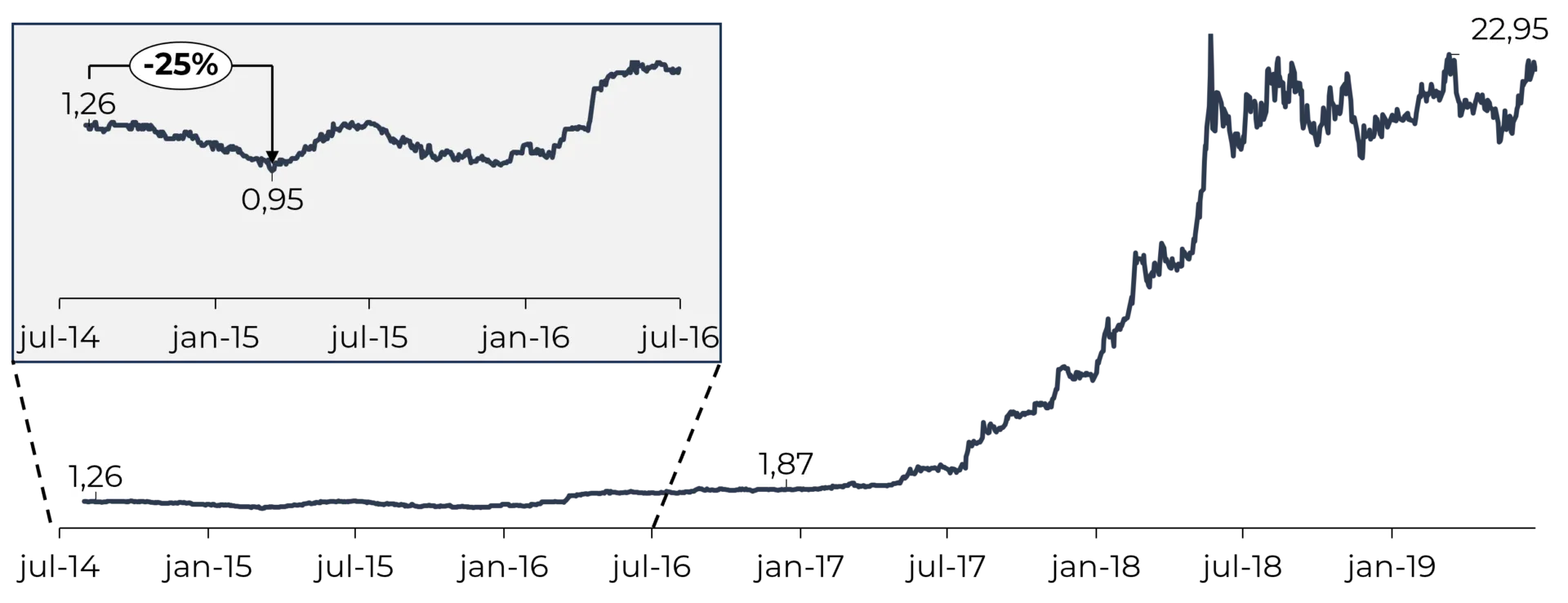

In 2013, Unipar’s sole asset was a 50% stake in Carbocloro, a chlorine and soda manufacturer. That year, Unipar announced the purchase of the other 50% of Carbocloro, and the acquisition price caught our attention. The asset being purchased was exactly the same as the one Unipar already held, yet it paid for the second half of Carbocloro at about 25% more than Unipar’s entire stock market value. In other words, either Unipar had overpaid for the acquisition or its shares were undervalued. This prompted us to deepen our analysis to estimate the real value of Carbocloro, and we concluded that Unipar — now the owner of 100% of Carbocloro — was worth at least twice its traded stock price.

In August 2014, we began buying Unipar shares. Six months later, the share price had fallen 25% (vs. a 12% decline in the IBOV over the same period). Despite the discomfort such a drop generates — especially in a recently purchased position with a healthy margin of safety — we conducted a detailed review of the thesis. The result of that review was counterintuitive.

Carbocloro’s operations were performing very well — even better than our initial expectations. The share price decline seemed more related to macro factors (2015 was the year of the crisis surrounding the impeachment of Dilma) than to the company’s own performance. In that context, we decided to buy more shares.

Our conviction in Unipar’s value was not shared by the market for quite some time. The stock only began rising meaningfully in the second half of 2017. In other words, we held the stock through three years of sideways movement before seeing the thesis truly prove correct and Unipar’s price rise sharply the following year. We sold our entire position in 2019, after five years as shareholders. During that period, we received dividends amounting to nearly the same as what we had paid for the shares, making the sale virtually pure profit and generating a return of approximately 20x the invested capital. The price appreciation during our holding period is illustrated in the chart below.

Price History* of UNIP6

This case illustrates clearly that the market is far from perfectly pricing the value of listed companies. Unipar’s price volatility during that period was far greater than the volatility of its operating results. Another lesson is the importance of patience. Had we grown frustrated with the first years of little appreciation and sold the position, we would have forfeited millions of reais in gains for our investors. This investment case is described in greater detail in our July 2020 letter.

After our sale, the stock moved sideways for about a year and a half before rising again to surpass BRL 100. Even with the 20x return on the Unipar investment, we still feel some regret for not having bought that stock again — one we knew so well — and capitalizing on the second wave of appreciation. It is part of an investor’s fate to dwell on calculations of the extra returns that could have been earned with a few different decisions along the way.

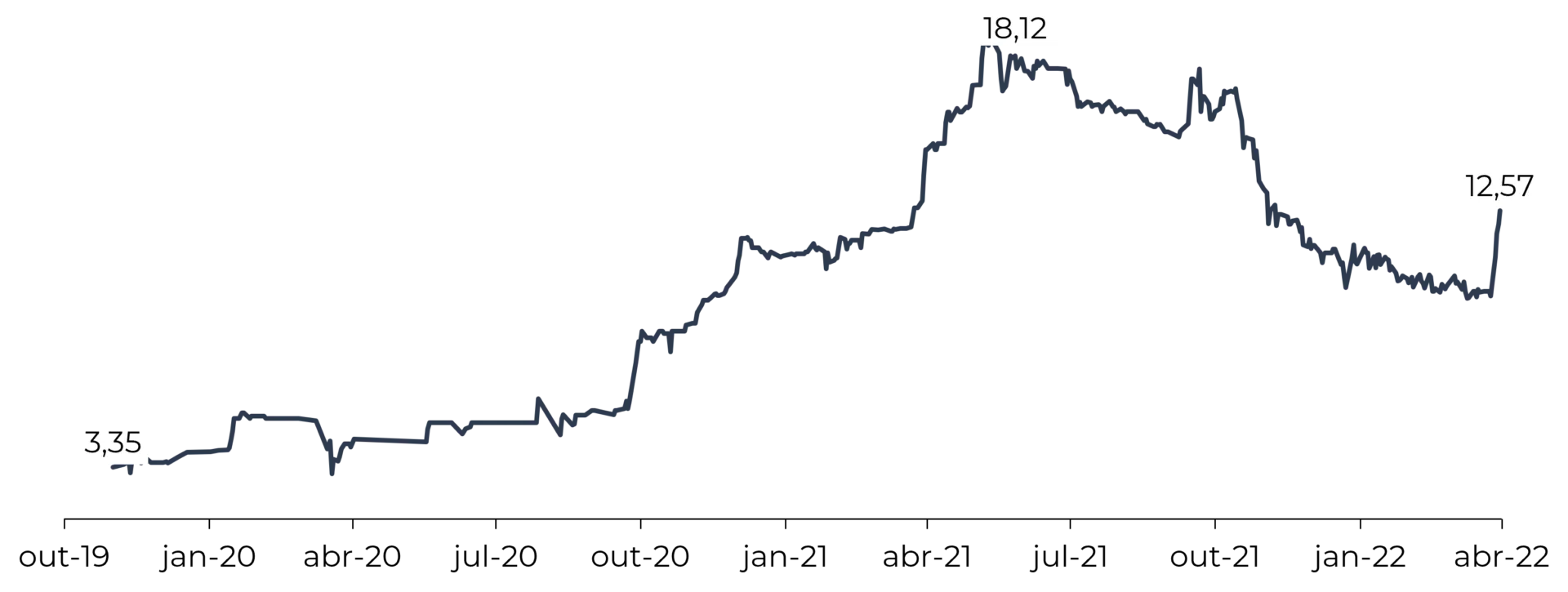

Marcopolo

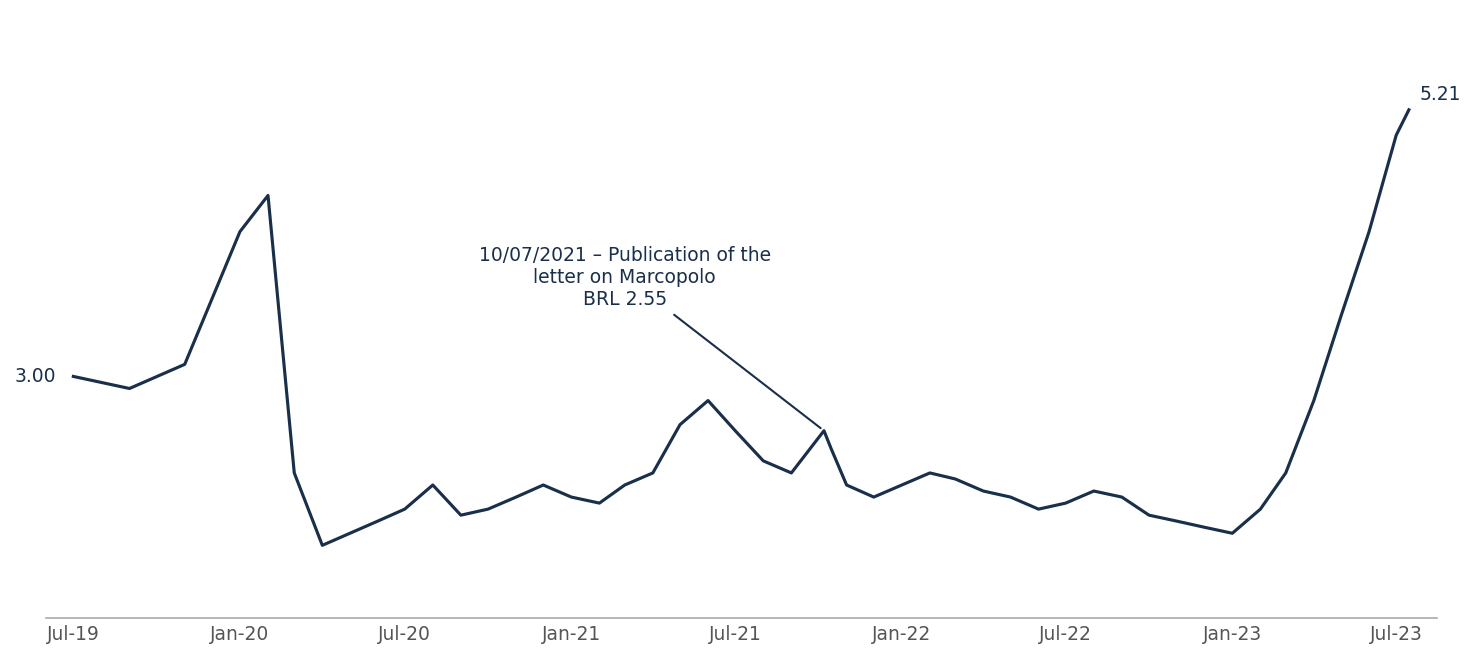

A more recent case still in our portfolio illustrates the same point. In 2019, we began buying shares of Marcopolo, the leading manufacturer of bus bodies in Brazil. In short, the thesis rationale is that Brazil’s bus fleet is much older than the equilibrium age implied by the last 25 years of historical data. Since bus replacements are technical decisions (when a bus starts generating high maintenance costs and excessive mechanical breakdowns, it is time to replace it), a wave of higher sales volumes was expected until the fleet age returns to its normal level.

The journey over the years was winding. The first months after our purchases were positive — the price rose about 50% — until the pandemic hit and the stock fell to 35% below our purchase price. We reviewed our numbers and concluded the sell-off was excessive, so we bought more Marcopolo shares.

To be honest, at the time we believed the pandemic would last less time (let those who didn’t think so cast the first stone). For those interested, our view on the COVID crisis at the time is in our April 2020 letter. In any case, the advantage of a thesis grounded in the aging of the bus fleet is that the passage of time can only make it older still, so we kept increasing our investment in Marcopolo until we held a position about 6x larger than before the pandemic.

Today, this investment has proven quite profitable, as seen in the stock price chart below. The thesis is described in more detail, including our rationale for increasing the position during the pandemic, in our October 2021 letter.

Price History* of POMO4

Strong Returns Do Not Depend on Buying and Selling Constantly

Whirpool

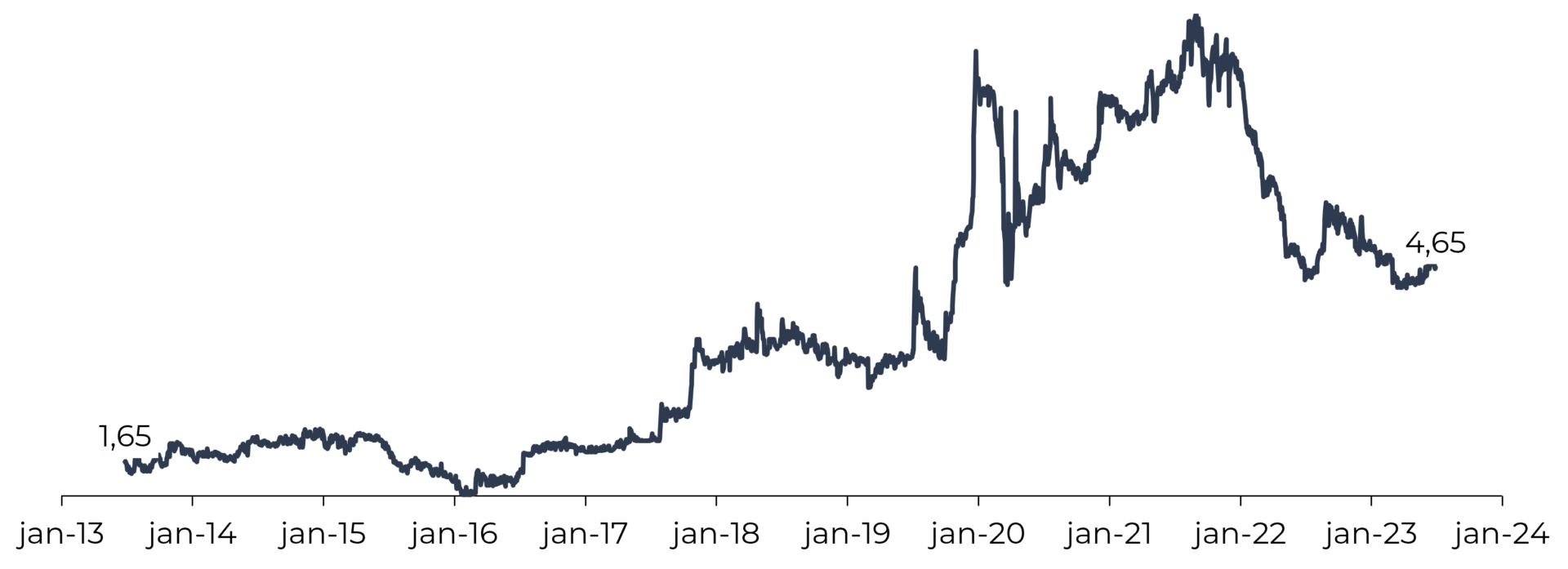

Another successful investment case, but with a very different profile, was Whirlpool — the company that manufactures Brastemp, Consul, and KitchenAid appliances in Brazil. Despite the company generating ~BRL 11 billion in annual revenue, it is almost never discussed in the Brazilian market because its stock is extremely illiquid (today trading volume is ~BRL 40 thousand per day). The lack of liquidity has historical reasons.

The company listed on B3 is a subsidiary of Whirlpool Corp, one of the global leaders in home appliances, listed on the New York Stock Exchange with annual revenues of ~USD 20 billion. The parent company attempted to delist its Brazilian subsidiary twice: the first in 2000, which reduced the free-float to 5%, and in 2016, which reduced the free-float even further, to the current 2%.

This was our first investment thesis. We bought our initial shares in 2013 and increased our position over the years. During the second delisting attempt, we were already shareholders and organized a group of minority investors to negotiate what we considered a fair price for the offer. The price negotiation with the company’s executives was not successful, but we managed to prevent the delisting at too low a price and kept our investment in the portfolio.

Due to the lack of liquidity, the company is overlooked on the stock exchange and we are unlikely to see enormous price spikes, but its business is excellent, with highly relevant competitive advantages, and it generates outstanding dividends. We have held the stock for 10 years, took advantage of downturns to increase the investment over time, and today have an internal rate of return of 14% per year since inception, even with the stock currently at a very low price level.

Price History* of WHRL4

The Stock Market Also Offers Atypical Opportunities

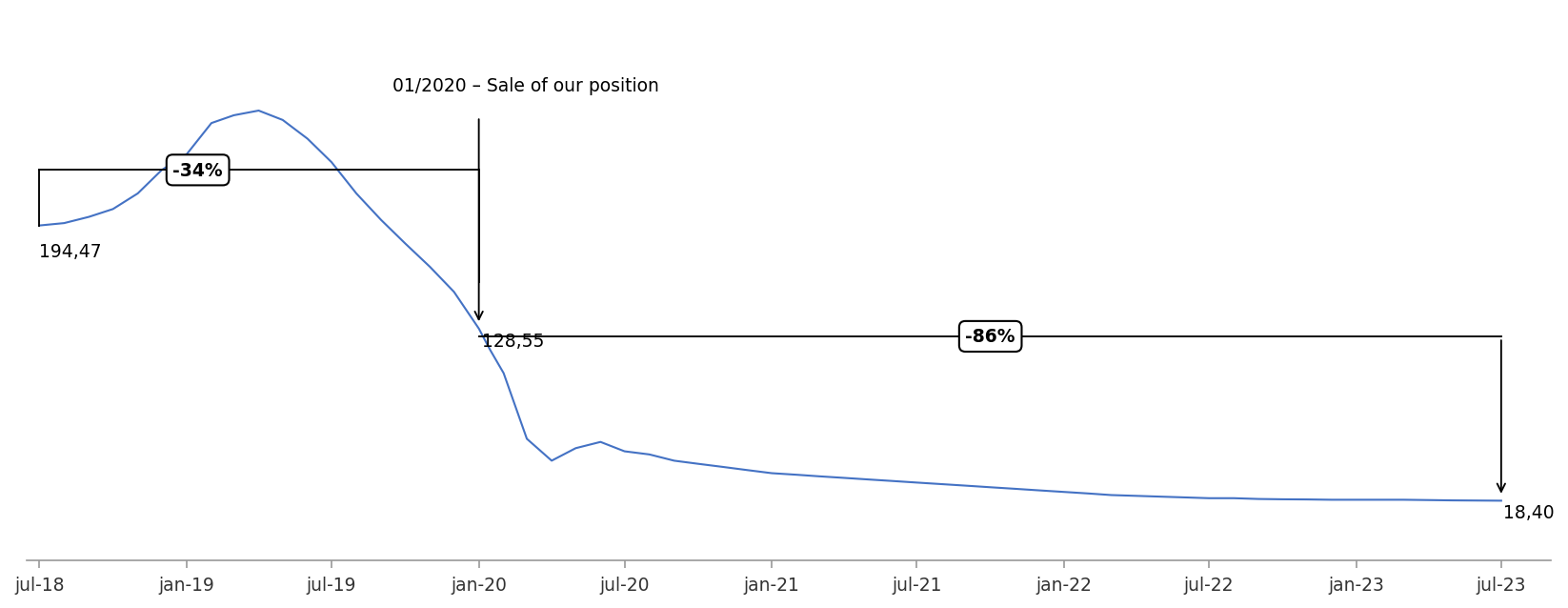

CEB

Buying shares in a good company at attractive prices and waiting for time to generate strong returns is the most traditional investment formula, but not every opportunity fits this category. In 2019, we were drawn to the case of Companhia Energética de Brasília (CEB), a state-owned company controlled by the Federal District government. At the time, the company’s main asset was an electricity distributor (CEB-D), which had a loss-making operation and risked losing its concession because electricity sector regulations require operators to maintain minimum financial health indicators. Far from what we would classify as “a good company.”

However, there were plans to privatize CEB-D, in which case it could prove to be a valuable asset, as Brazil’s electricity sector has a successful track record of state-owned company privatizations (Equatorial and Energisa, for example, generated enormous value for their shareholders by acquiring state companies and making them more efficient). We decided to analyze the situation in detail.

In short, we concluded there were two very distinct scenarios for the future of a potential investment. If CEB-D were privatized, the likely return was in the range of 150%. If privatization did not happen, the risk was that the company would lose about 50% of its market value at the time. In other words, if the probability of privatization were greater than 25%, the expected value of the investment was positive. We monitored the situation until it appeared the probability of a successful privatization was quite high, and we began buying CEB shares in November 2019.

Since the thesis risk was significant, we started with a small investment, and as the privatization process became more certain, we kept buying until approximately 10% of the fund was invested in CEB.

The privatization of CEB-D was completed in March 2021, at an acquisition value higher than we had anticipated. After that, the market still took time to appropriately price the stock. For months, CEB’s market value remained below the cash position it would hold after receiving payment from the CEB-D sale. As a result, we held our investment for another year and sold in 2022, with a cumulative return of 5x the invested capital. Further details on this investment were described in our January 2021 letter.

Price History* of CEBR6

Not Every Thesis Will Succeed: Constant Attention and Flexibility to Change One’s Mind Are Essential

Restoque

Since not everything is rosy, we will tell the story of our worst investment, which was in Restoque (currently renamed Veste), the apparel manufacturer and retailer that owns the Le Lis Blanc, Dudalina, and several other brands.

The company had a troubled history after acquiring Dudalina from its founders, partly due to failed strategies and partly due to conflicts among its main shareholders. Nevertheless, the stock appeared very cheap, the shareholder conflicts seemed resolved, and the business recovery plan presented by its executives was reasonable. We followed the company for some time, and after three consecutive quarters of improving indicators, we interpreted the recovery plan as beginning to bear fruit and this as an inflection point for the business. If the plan were successfully implemented, the upside potential was enormous. We began buying shares in mid-Q3 2018.

Over the following two quarters, the operating indicators deteriorated again. As operational restructurings are always complex, we gave the company and its management team the benefit of the doubt and remained invested. After five quarters of poor results, in early 2020 we decided to liquidate our position and took a loss of around 30% of the invested amount.

Price History* of LLIS3

The only consolation is that the decision to exit was correct, as after we sold, the shares continued falling to a fraction of their historical value. The company recently had to undergo a capital restructuring.

It was our first case of a significant loss, and we make a point of revisiting it from time to time — to contemplate the irrefutable proof that even carefully crafted theses can be completely wrong, and to keep alive the fear that makes us diligent and willing to change our minds.

The Profile of the Investor Base Is Important for the Fund’s Performance

As you can see, even the successful theses had their “exciting” periods. In these moments, the greatest risk an investor faces is to panic, setting rationality aside and beginning to make decisions based on psychological factors. Beyond the natural pressure that investment jolts generate, fund managers face an additional layer of pressure: demands from their investor base. In this regard, we feel privileged.

To this day, our fundraising from new investors is atypical. While most managers choose to make their funds available on brokerage platforms — which allow anyone to invest with little information beyond the fund’s historical returns — we decided to keep Ártica Long Term FIA off these platforms and adopted practices that ensure greater alignment of expectations.

We explain to interested parties our strategy, the results it should generate, and what portion of their capital is appropriate to invest in this manner. In short, we seek to maximize the fund’s absolute return over long time horizons, exceeding 5 years. We are subject to periods of volatility along the way (though Ártica LT’s volatility is very similar to that of the IBOV itself), as we tend to take advantage of market stress moments to make purchases and are willing to wait several years to sell, as long as the investment thesis remains sound. Therefore, only a portion of capital that can remain invested for several years is appropriate for investing with us — ideally with timeline flexibility to be able to withdraw at a favorable market moment.

Despite seeming like an obvious approach, few managers follow this path because it reduces fundraising and, therefore, the manager’s own compensation (at least in the short term). However, we prefer to grow slowly and steadily rather than seek shortcuts to attract investors whose profile is incompatible with our investment style.

The great benefit is that today we have an extremely differentiated investor base that is aligned with our philosophy. The best proof of this is to compare the evolution of Ártica LT’s assets under management during the 2022 downturn cycle with what happened to other equity funds. While most funds experienced waves of redemptions due to months of losses — some losing more than half of their assets under management — we received a substantial volume of new contributions, which allowed us to take advantage of depressed prices and expand our investment portfolio. Moreover, approximately 90% of our investors have never made a single withdrawal, even having endured difficult periods alongside us.

Having the support of our investors to do what we truly believe will deliver the best long-term return — even when it requires psychologically uncomfortable decisions — is a rare privilege. For this, we extend our most sincere thanks to all who have entrusted their capital to us over all these years. We will continue striving every day to bring you, in the years ahead, a return as strong as the one we achieved in our first decade.

* The prices shown in the charts are adjusted for dividends, and any share consolidations or splits during the period.

1 Ártica Long Term started on 06/27/2013 as an “investment club” and, on 09/27/2019, was converted into an “equity investment fund”.