Investment Case – Porto (B3:PSSA3)

Dear investors,

The ideal investment opportunity is to find a high-quality company trading at low prices in the market. This type of opportunity almost never arises when the economic environment is favorable and the company is delivering strong results. Therefore, if you want to buy truly undervalued stocks, you must be prepared to invest when the macro backdrop is very weak, when the company is reporting poor results, or when both are happening simultaneously.

It was in such a context that we purchased shares of Porto (PSSA3). This thesis is particularly interesting because it is almost a textbook case—without major complications or unexpected twists—and it clearly illustrates key aspects of our investment philosophy. We will therefore walk through the story of this investment, which is still ongoing. Currently, Porto is the second-largest position in the Ártica Long Term FIA portfolio.

What Porto does

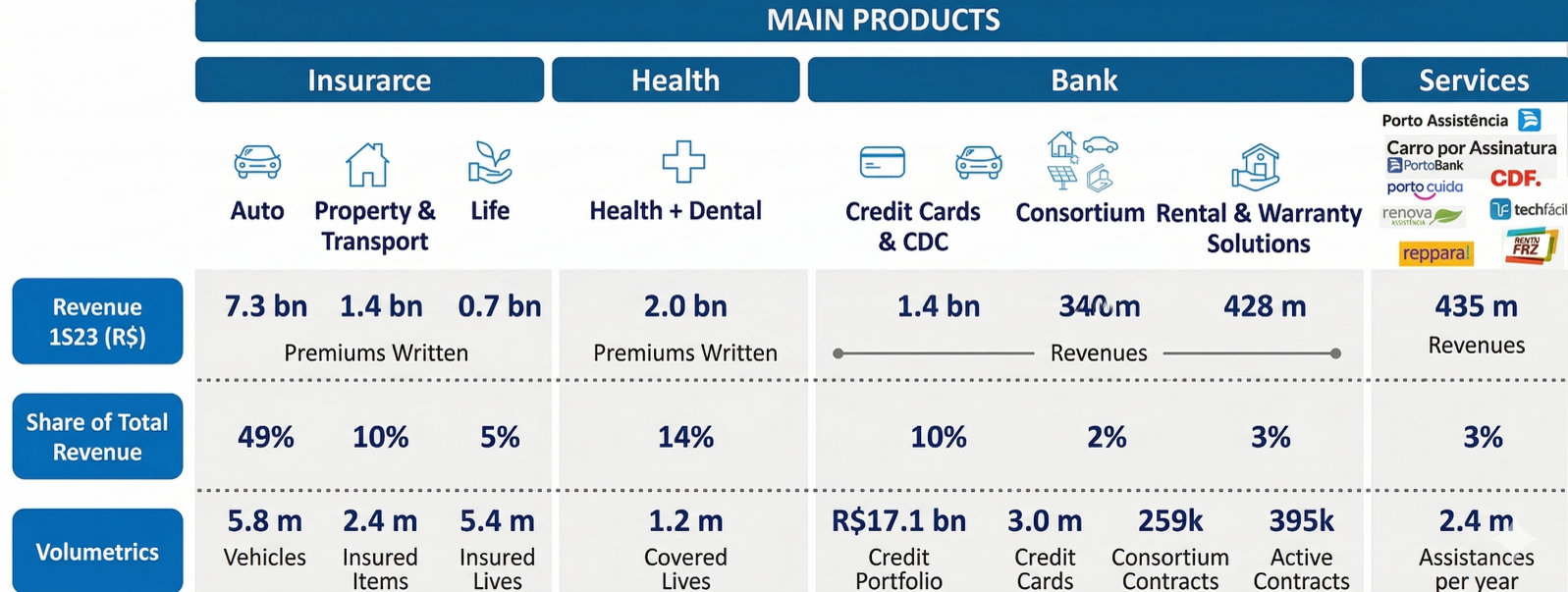

Porto is one of the leading insurance companies in Brazil, with 13,000 employees and 37,000 independent brokers who currently serve 16 million clients across the country. The group is organized into four business verticals: Insurance, Health, Bank (financial services), and Services (general services). The core of the business is the Insurance segment, which currently accounts for approximately 65% of the company’s total revenue. This was the group’s original activity. The other verticals were developed with the objective of offering additional products and services to Porto’s existing insurance clients. The table below provides a clear overview of the company’s current business lines.

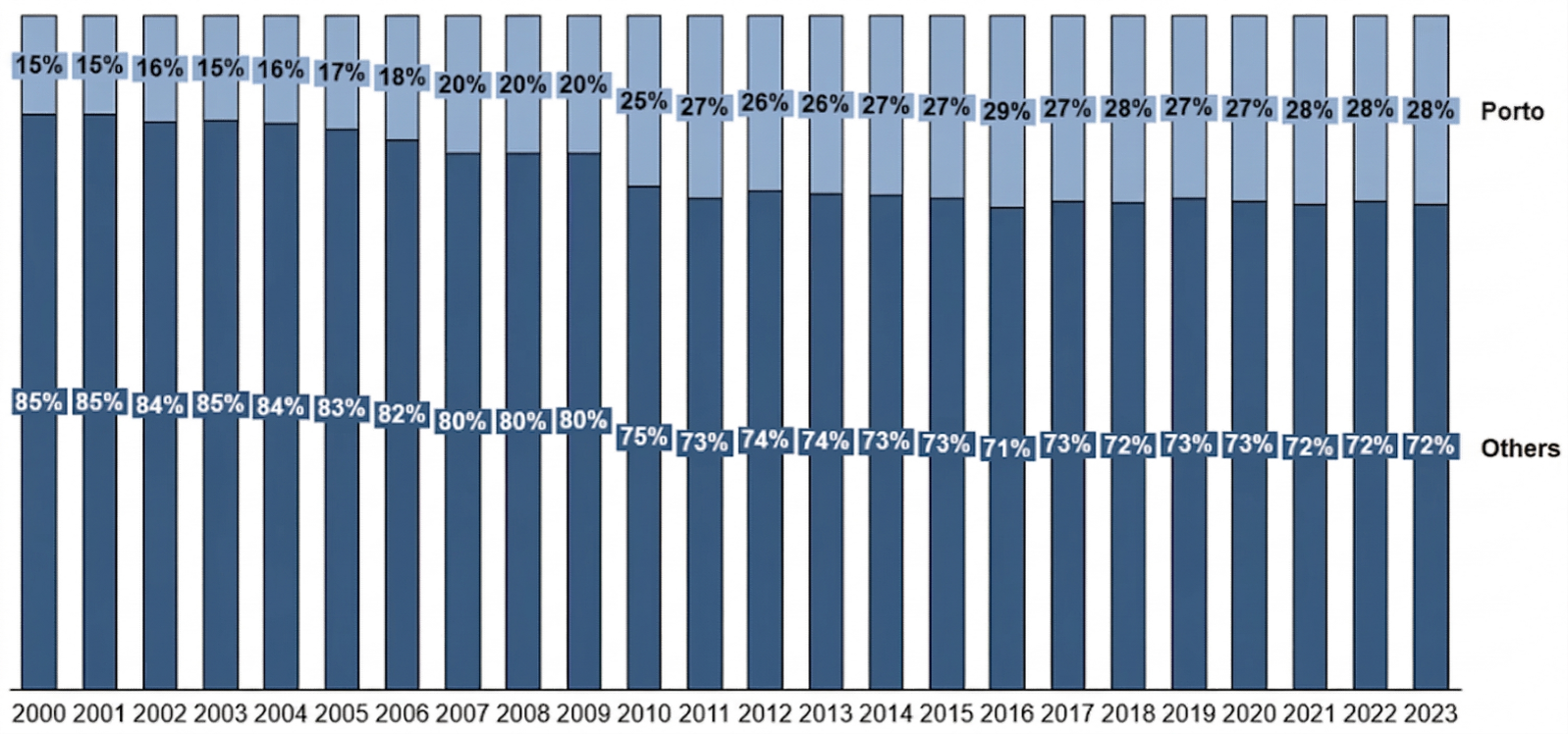

In auto insurance, Porto is the clear market leader in Brazil, having maintained a market share of approximately 27% for more than a decade, while the second-largest player holds around 18% (following acquisitions) and the third about 13%. In the Southeast—where Porto has its strongest presence—its market dominance is even more pronounced. This segment is the most relevant for the company not only because it accounts for roughly 50% of group revenue, but also because it is the most recognized business line and serves as the primary entry point for new clients, to whom the rest of the company’s products and services are subsequently offered. For this reason, we will place greater emphasis on this segment.

The key point is to understand how Porto has been able to sustain its leadership position for so long. Stable market share typically indicates the presence of barriers to entry and competitive advantages, as only with such constraints are competitors unable to attract large numbers of customers. Industries with these characteristics tend to exhibit orderly competitive dynamics, in which each company dominates specific regions or product segments and avoids aggressive moves to capture market share from competitors. This framework applies well to the auto insurance sector in Brazil, where the market share of leading insurers has remained stable or has changed only gradually over time. Below, we show how Porto’s market share has evolved since 2000.

Market Share Porto vs. other insurers

Source: Susep

In our view, there are three main competitive advantages that make Porto’s leadership position highly sustainable: the scale of its operations, the strength of its brand among end customers, and the strong reputation and relationships the company maintains with its network of independent brokers. We will explore each of these in turn.

The importance of scale in the auto insurance segment is tied both to traditional economies of scale (e.g., bargaining power in negotiating spare parts) and to the need to maintain a support network capable of assisting insured vehicles that, for example, are involved in traffic accidents.

This support structure must be sized to handle peak demand in each region—i.e., the number of simultaneous service requests each unit must be able to handle in order to ensure a satisfactory level of service. For smaller insurers, both geographic coverage and the efficient utilization of the assistance network are challenging requirements.

The issue of geographic coverage is straightforward. Consider a small insurer whose clients are concentrated in the state of São Paulo. It is natural for the company to have a service structure in the region where its clients are based—but how should it assist a policyholder involved in an accident while traveling to Minas Gerais? It is inherently unpredictable where and when clients will travel, and maintaining coverage across all potential locations to handle sporadic events is economically unviable. An insurer with clients in both São Paulo and Minas Gerais has a clear advantage. Ideally, an insurer should operate nationwide, as is the case with Porto.

Understanding the advantages of scale in optimizing the use of the assistance network requires some basic statistical intuition. A traffic accident is a low-probability random event, and therefore it is impossible to predict whether a specific driver will have an accident on a given day. However, it is much easier to estimate how many accidents a large group of drivers will have in a day. The larger the group, the greater the predictability of the total number of accidents, as it converges toward the probability of an individual accident multiplied by the number of drivers in the group. This statistical principle is known as the Law of Large Numbers. Accordingly, the larger the number of clients within the service radius of a given assistance unit, the more predictable and stable the number of accidents that unit will need to handle each day—and the lower the cost per service. In this context, it is not only the total number of clients that matters, but also how concentrated they are within a given region. Therefore, the insurer with the highest market share in a specific geography will likely have the lowest logistical cost to service insured events. Once again, this is the case for Porto in the country’s main regions.

As an illustration, based on our estimates using 2023 data from the Ministry of Transport (excluding minor accidents that are not officially recorded), the average probability of a driver in Brazil being involved in an accident is once every 78.9 years. Accordingly, an insurer with 100,000 clients within the service radius of a given unit could expect to handle approximately four accidents per day in that location. This highlights how difficult it is for a smaller insurer to maintain a support network that delivers a high level of service without remaining idle most of the time.

As the market leader with nationwide coverage, Porto is in an excellent position to offer superior service levels to its clients, further reinforced by a culture strongly focused on service quality. Over decades of consistently serving its clients well, the company has built an outstanding reputation that is very difficult to replicate. Today, the Porto Seguro brand is one of the most recognized and well-regarded in Brazil.

An insurer’s reputation is particularly important given the nature of its business. Customers pay for their policies upfront and expect the insurer to honor its obligations, but they only truly test that expectation on a bad day—when they find themselves stranded with a damaged vehicle. It is therefore natural for individuals to prefer contracting insurance with a company that has a strong reputation, and to be willing to pay a premium for the confidence that the insurer will be reliable and responsive when needed.

Porto’s average annual auto insurance premium was BRL 2,600 (USD ~520) in 2023, or approximately BRL 220 (USD ~44) per month. If a lesser-known insurer were to offer a 10% discount—a meaningful difference—would it be worth saving BRL 22 (USD ~4.4) per month at the expense of peace of mind regarding service quality in the event of a claim? Most people believe it is not and prefer to remain with Porto, particularly as the incremental cost is unlikely to materially impact their finances. This pricing premium, relative to the industry average, directly supports the company’s profitability.

The third competitive advantage is the strong relationship with its network of independent insurance brokers, which accounts for approximately 80% of new auto insurance policy sales. This relationship is sustained by several factors: commissions are attractive relative to market averages; payments are consistently made promptly and efficiently (within up to seven days), which is particularly important for brokers, who may not always have strong financial positions; Porto’s systems and internal teams interact with brokers in an efficient and practical manner; and the company runs incentive programs to motivate the network, such as travel awards or product prizes for top-performing brokers. This combination of initiatives, together with the strength of the Porto Seguro brand among end customers, makes Porto’s products the preferred choice for brokers, increasing the likelihood that they are recommended to clients.

Acting together, these three core competitive advantages create a virtuous cycle that continues to strengthen Porto and makes it very difficult for competitors to challenge its leadership position. Scale supports broad coverage and a high level of service, which enhances customer satisfaction and reinforces brand strength. This, in turn, allows the company to command a pricing premium and better compensate brokers, who help attract more clients—further expanding scale.

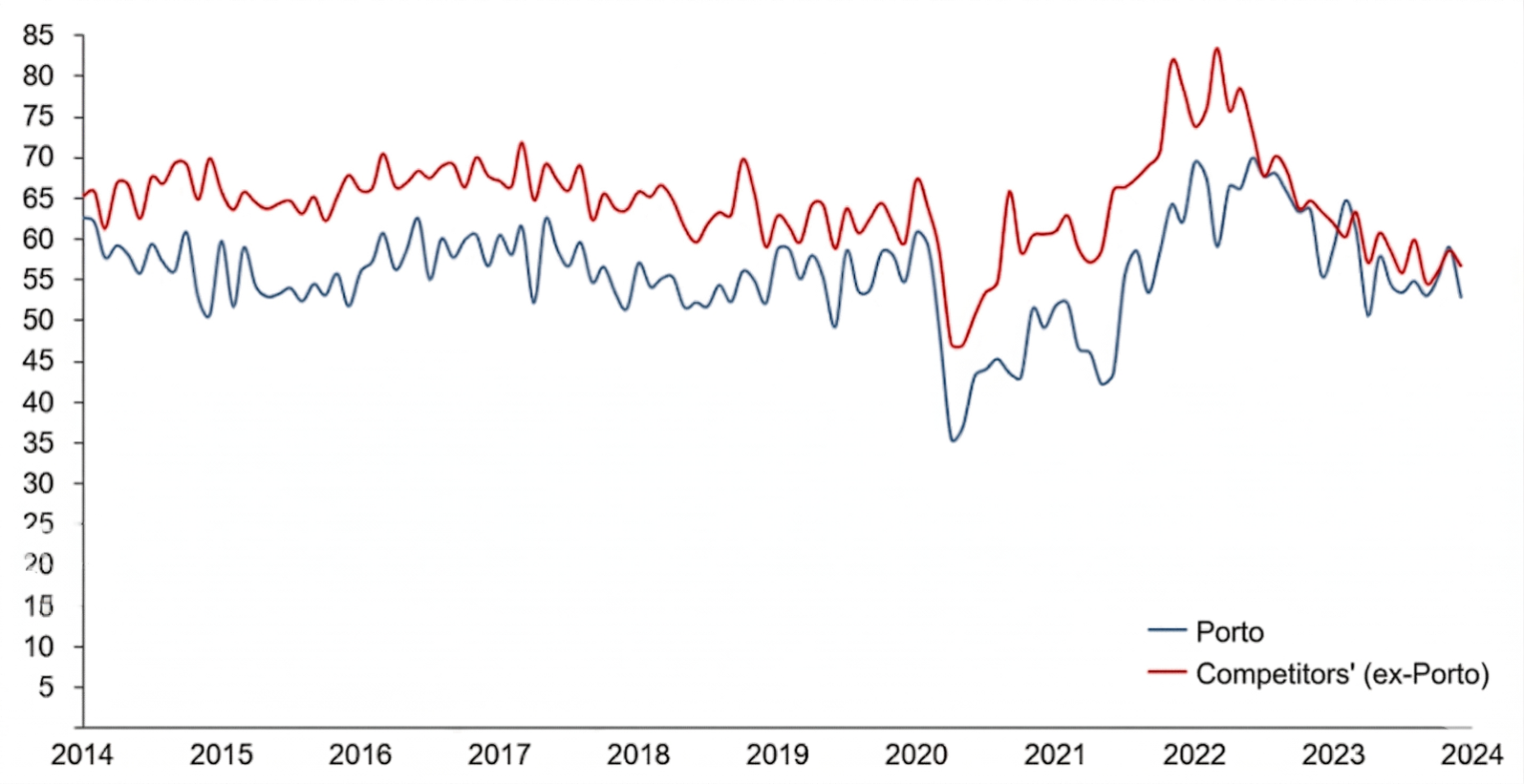

Porto’s advantage is evident when comparing its loss ratio (claims incurred divided by earned premiums) with that of the broader market. Year after year, it outperforms its peers (the lower the loss ratio, the better).

Porto Loss Ratio vs. Other Insurers (%)

Source: Susep

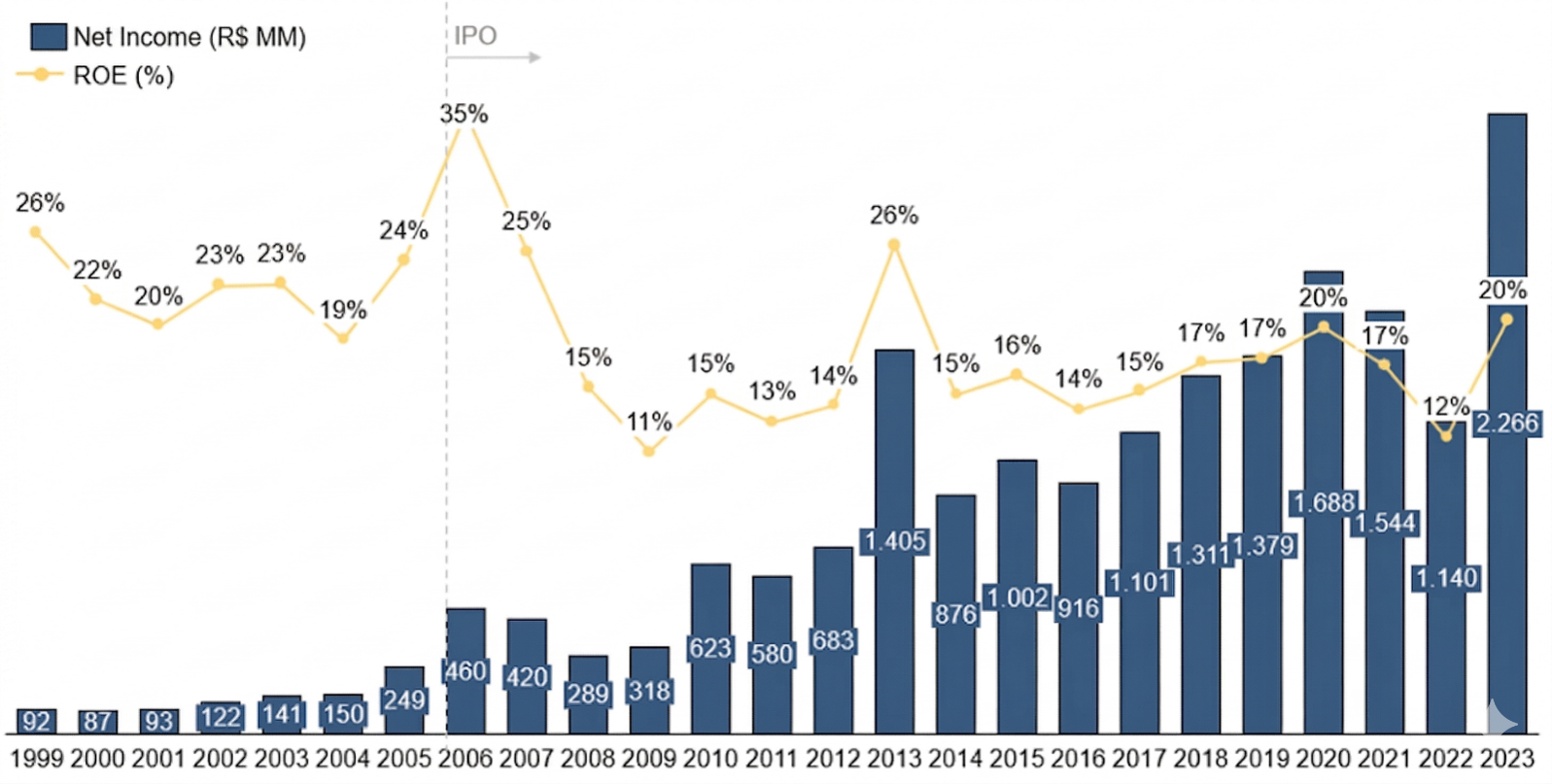

In this context, Porto has been growing and delivering excellent financial results for decades. Over a 25-year period, its revenue has expanded and its margins have remained healthy every single year—even through major crises such as the subprime crisis in 2008, Dilma’s impeachment in 2015, and COVID-19 in 2020. Very few companies have such a strong track record. In businesses with these characteristics, it is very difficult to lose money as an investor. Even in the absence of any major re-rating in the company’s valuation, the compounding effect of sustained results over time is significant. Since its IPO in December 2004, Porto’s shares have delivered an average annual return of 16.3%, increasing in value by 18.3x.

Net Revenues (BRL billion)

Net Income and Return on Equity

What Created the Opportunity

Porto is a well-known name in the market. Nearly 20 years since its IPO, combined with above-average profitability, have made it one of the standout success stories in the Brazilian stock market. Historically, its shares have outperformed the Ibovespa over virtually any five-year period. As a result, the high quality of its businesses is no secret. What led to the decline in its share price was a specific set of circumstances.

During the pandemic, the auto insurance sector faced several shocks. The first was the sharp decline in new car sales in 2020, which also reduced the number of insurance policies—typically purchased when a new car is delivered. As a result, Porto’s auto insurance revenue did not grow that year and, more importantly, market expectations for the company’s future growth were revised downward, putting pressure on the stock price.

We made our initial purchases in early 2021, still with a modest capital allocation, in order to begin tracking the case more closely. Our view was that the insurance sector had historically been highly resilient and would likely remain so, as private vehicles would continue to be an important mode of transportation.

The first half of 2021 still showed typical growth, and Porto resumed stronger growth in the second half. Even so, the company’s shares declined amid the beginning of the interest rate hiking cycle announced as a measure to combat inflation. We took advantage of this decline to make our first meaningful purchases at the end of 2021—somewhat early, in hindsight.

In 2022, another shock affected the industry. During the period of social distancing, vehicle usage had declined significantly, reducing the number of accidents (loss ratios) that insurers had to cover. Initially, this had a positive impact, but competitive dynamics led to adjustments in the pricing of new policies, reflecting the expectation of lower claims. Shortly thereafter, two unexpected developments negatively affected insurers’ profitability: urban traffic returned to normal faster than anticipated, and, at the same time, there was a sharp increase in the prices of vehicles and spare parts, raising the average cost per claim. As a result, some cohorts of insurance policies became significantly less profitable than usual, compressing industry earnings. Weaker results, combined with broader macroeconomic uncertainty—driven by higher interest rates and presidential election-related concerns—kept Porto’s share price depressed throughout the year.

We kept buying. One factor that gave us strong confidence was observing the company implement a significant increase in auto insurance pricing (a 43% increase in premiums written in 2Q22 vs. 2Q21) without any reduction in its customer base, as all insurers followed the repricing. Once this adjustment was made, it became only a matter of time before profitability was restored, as the less profitable policies would need to be renewed at the new pricing once they reached their one-year anniversary from issuance.

It is rare to have such clear visibility into the factor that will drive a company’s return to its historical profitability, as well as a clear timeline for when this will occur. To this day, we still ask ourselves why this investment opportunity persisted for so long in such a well-known and liquid stock. Our best hypothesis is that many funds were facing redemptions, which limited managers’ ability to act on the opportunity, or that they were seeking investments with the potential for faster returns in order to address investor dissatisfaction. In any case, we spent 2022 acquiring Porto shares at attractive prices, ultimately tripling our capital allocation relative to the end of 2021 and making this our largest position at the time.

Where We Stand Today

Fortunately, the auto insurance segment has recovered its profitability and resumed growth throughout 2023, as we had anticipated. Growth was, in fact, stronger than we initially expected. Over the past two years, auto insurance revenue has increased by 44%. The company’s other business segments, although not the focus of this discussion, also contributed meaningfully to growth, with non-auto revenues expanding by 57% over the same period. As a result, the group’s consolidated revenue grew by 50%. It is worth noting that we are referring to a company of significant scale, with net revenue of BRL 21.3 billion (USD ~4.3 billion) in 2021, which reached BRL 31.9 billion (USD ~6.4 billion) in 2023.

As a consequence of these strong results, the share price has increased, albeit more modestly than one might expect. Today, Porto’s market value is 37% above the market capitalization implied by its 2021 year-end closing price. While this may appear to be a significant increase, the stock was already undervalued at that time, and the business has evolved to a clearly higher level over the past two years—something that is readily observable when comparing recent financial results.

Another data point suggesting that the company remains undervalued is that Porto’s current P/E multiple stands at 8.1x, compared to a historical average of 10.9x over the past 10 years.

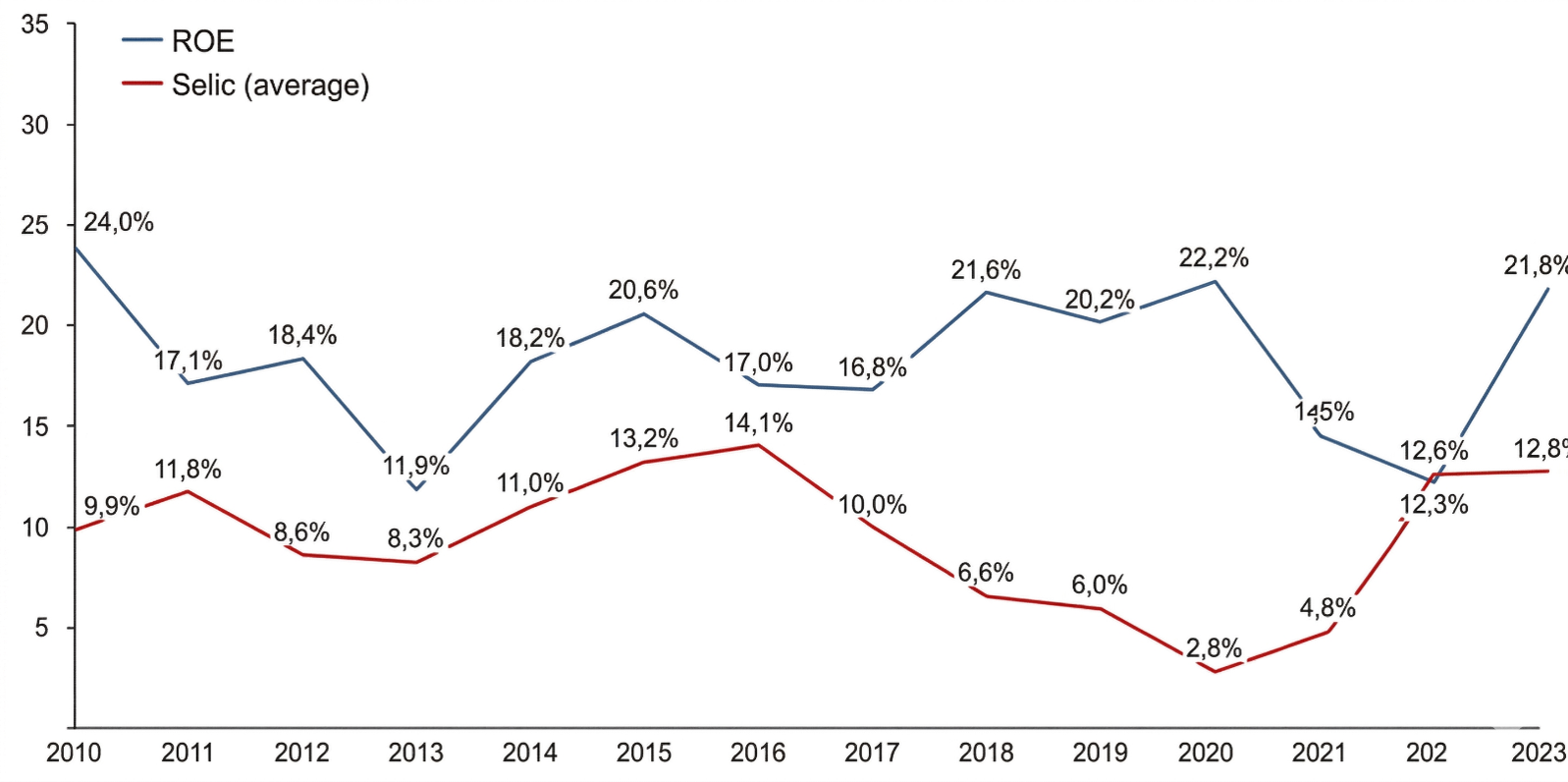

One argument that could explain the market’s reluctance toward the stock is the expectation that insurers will deliver weaker results in a lower interest rate environment, as part of their revenue comes from investing premiums received upfront from policyholders. However, this hypothesis is not supported by Porto’s historical performance. The company has maintained a similar level of profitability across various economic environments with significantly different interest rate levels. In essence, this is because the insurance industry in Brazil is highly professionalized and prices its policies by already incorporating the interest rate curve expected by the market. As such, the anticipated decline in interest rates is already embedded in current pricing.

Porto Return on Equity vs. SELIC Rate (% per year)

In the absence of a compelling explanation for why the stock would be undervalued, it appears to us that it simply remains cheap amid the continued reluctance of many Brazilian investors toward the equity market. As such, Porto remains one of the core positions in our portfolio, and we remain optimistic about the results it should deliver in the years ahead.