Why We Invested in Multi?

Dear investors,

Something we enjoy evaluating are opportunities to invest in “elite athletes with a cold”: businesses with an excellent track record of financial results that are undervalued due to poor recent performance caused by some temporary ailment. Especially in times of weaker economic conditions, the market tends to place excessive weight on short-term results and penalize heavily those companies that post poor quarters. This creates opportunities to buy at low prices the shares of companies with a good chance of recovery through the simple reversion of their results to the historical average.

This type of investment requires a willingness to act against prevailing public opinion, which is more difficult than one might imagine. Companies with poor recent results and falling share prices are easy targets for criticism from market professionals. At a certain point, so many people are speaking negatively about the stock that a stigma forms around the company, and several investors begin dismissing the thesis without properly investigating its merits — simply assuming that the majority must be right, and, in the case of professional fund managers, also because of the reputational risk implicit in investing in what the entire market believes to be a bad idea, which would create the image of an avoidable mistake should the thesis produce poor results in the future.

Note that this type of stigma has no impact on the real risk of a given business, but can cause its share price to fall further than fundamentals justify, creating risk-return asymmetries that may offer atypically attractive investment opportunities. This is precisely the type of situation that investors should investigate.

In this letter, we will share a summary of our investment thesis on Multi (formerly Multilaser), which fits exactly what we have just described: it has an excellent track record over the past ten years, poor results in recent quarters, and is the target of disdain from most professional investors. In this context, its share price has fallen so far that only a partial recovery of its historical results is needed for the investment to deliver attractive returns.

Performance Over the Last Decade

Multi started its operations in 1987, selling rechargeable printer cartridges. By 2003, the company was the leader in its market niche, with annual revenue of around R$30 million, and an unexpected event changed the course of the business: its founder, Israel Ostrowiecki, passed away in an accident while diving on a vacation trip. His son, Alexandre Ostrowiecki, then took over the company at just 23 years old, bringing in Renato Feder — a personal friend and son of the entrepreneurs leading the Elgin group — as a partner to help him face the challenge of maintaining and growing the business.

In the years that followed, Multi began expanding its lines of business, launching computer accessories and electronic products imported from China under the Multilaser brand, with the value proposition of offering the Brazilian market technology products at highly accessible prices and with quality control superior to indiscriminately imported Chinese goods competing in the same price range. To this day, Multi is strongly associated with Multilaser computer accessories, which represent only a fraction of the company's total business. But before we delve into its current business model, let us look at the data that caught our attention and led us to study the Multi investment thesis.

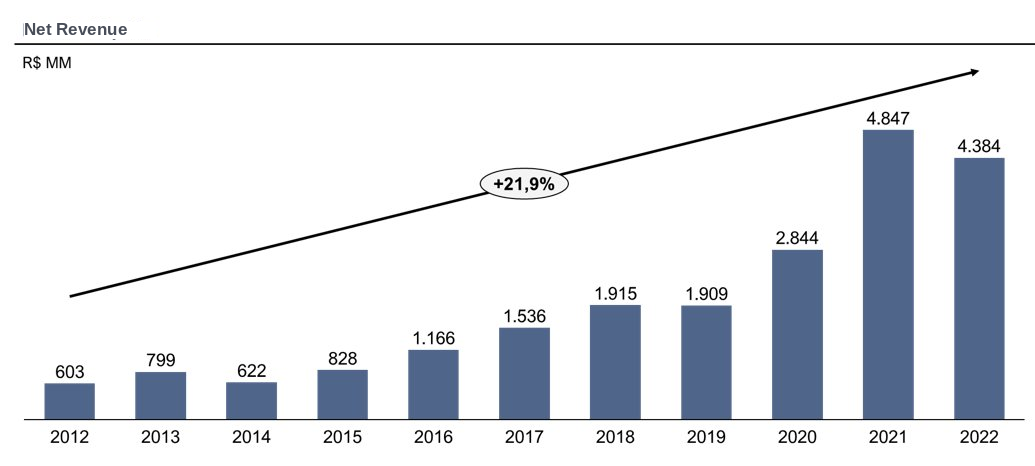

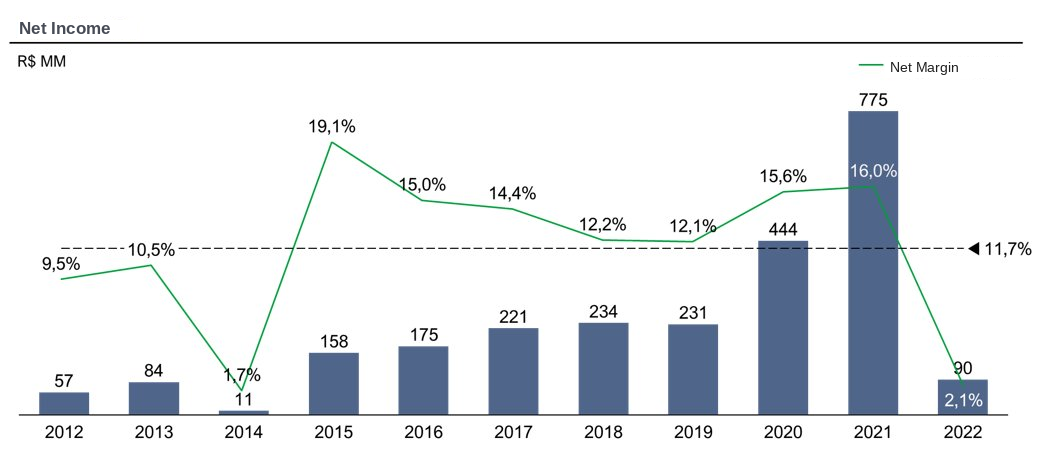

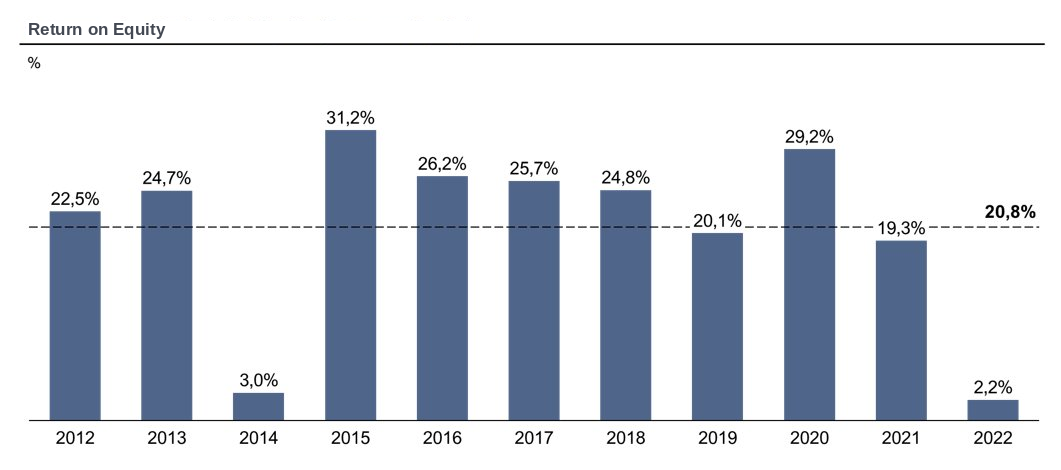

Over the past ten years, the company posted average revenue growth of 21.9% per year, with an average net margin of 11.7% and average return on equity of 20.8% (already including the poor year of 2022). The annual results history for this past decade is illustrated in the charts below.

Beyond this excellent track record, we appreciate the fact that, in contrast to the recent “unicorns” that grew rapidly while consuming hundreds of millions received from venture capital funds in loss-making operations, Multi followed a more traditional trajectory: it grew while maintaining good profitability over the years and reinvesting its own cash generation. If what we have presented so far has also caught your attention, let us explore what Multi’s business is today.

What Multi Does Today

Multi today is a major importer, manufacturer, and distributor of a wide range of consumer goods. Its portfolio includes more than 7,000 products (SKUs) across 44 brands, of which 20 are proprietary and 24 are partner brands, several of them distributed by Multi exclusively in Brazil. In addition to the well-known computer accessories, the company sells smartphones, notebooks, small appliances, household utensils, tools, sporting equipment, health and beauty products, telecommunications network equipment, automotive products, security equipment, children's items, pet products, and many other product categories. Multi is truly a fitting name for the company.

Multi's customer base is also highly diversified. There are more than 30,000 customers selling Multi's products across more than 44,000 points of sale. Among the clients are retailers of all sizes, distributors, companies that purchase large quantities directly, and public entities through contracts won in government tenders. End consumers are also served directly through e-commerce channels.

The company's business model is based on its sales force and operational efficiency. It consists of identifying technology-related products that are on the rise, building relationships with manufacturers — many of them located in China — testing products in its laboratories to ensure expected quality, and importing them into Brazil at competitive costs. Some products are purchased ready-made while others are assembled or manufactured on Brazilian soil, sometimes to take advantage of tax benefits offered to companies with local production. By maintaining high operational efficiency and cost control, Multi is able to offer products at extremely competitive prices compared to products of similar quality.

Note that this business model depends little on the product categories in which the company operates. Multi has 12 business units that operate autonomously and deal with very different product classes. Each unit has its own resources, marketing, and engineering teams, and senior executives’ compensation is tied to the return on capital employed in their unit. In addition to risk diversification, this decentralized operation also gives the company flexibility to adapt to changes in market demand profiles. That is, if a given product segment ceases to be profitable, the cost of abandoning it and replacing it with another segment is quite low. Even Multi’s production and assembly lines are easily adaptable to manufacture a wide range of different products.

This versatility is not theoretical. The company has already made major changes to its product mix over time while maintaining consistent financial results throughout the transformations in its portfolio. Embedded in Multi's culture is the discipline of continuously monitoring the profitability of each item and replacing those that do not meet the target profitability with new products. We believe that this dynamic of continuous portfolio renewal in pursuit of profitability is one of the key success factors for Multi.

However, the following question arises: if the business model is profitable, diversified, and adaptable, why did the company have such poor recent results and why was its valuation so heavily penalized by the market?

Recent results

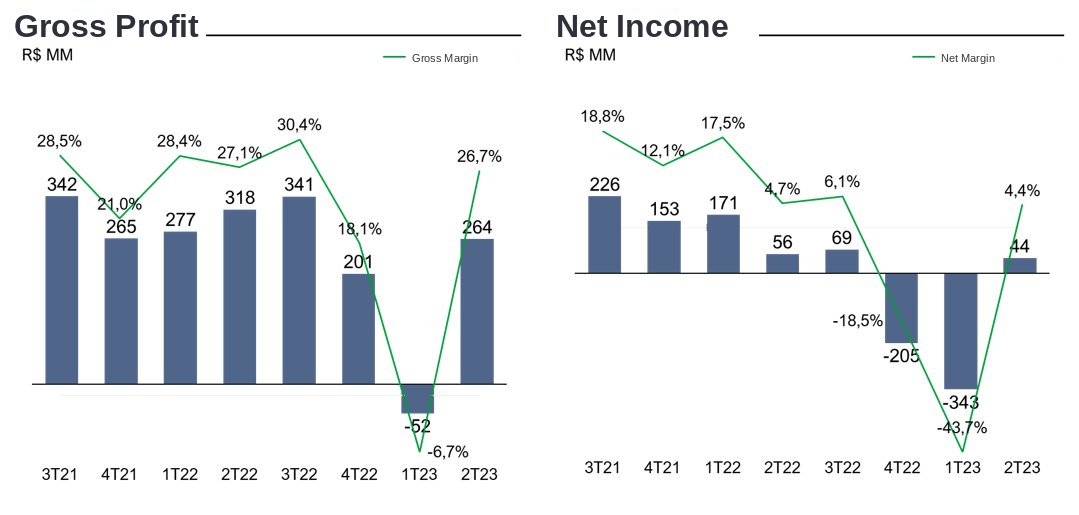

The year 2021, in which Multi went public on the Brazilian stock exchange, was quite atypical. Amid the lock down, while several service and entertainment businesses were suffering, various product segments experienced a period of elevated demand: for example, people working from home began buying more small appliances to ease their domestic routines and more computers and computer accessories to equip their home offices. However, at the same time, the goods import process was much slower than usual due to logistical problems and product shortages caused by production stoppages. Multi reacted to this scenario in a way that initially made sense: it increased its inventory levels in proportion to what was needed to sustain the sales volumes being achieved. This reaction is what later caused a severe hangover.

For a long time, Multi had followed the practice of maintaining robust inventories in order to quickly fulfill customer orders — a differentiator especially important for small retailers that do not have sufficient working capital to keep large amounts of merchandise in their stores. The practice worked well for years and appears well-suited to periods of predictable demand, but proved to be a dangerous strategy during periods of demand shock.

In 2022, following the end of the lock down and the consequent return to normalcy, consumption in the product segments we mentioned returned to pre-pandemic levels, while Multi still held inventories sufficient to meet several months of overheated demand. Faced with weak demand, the company was forced to carry out very aggressive inventory clearances that destroyed its profitability in Q4 2022 and Q1 2023.

In addition to this problem, in January 2023 the company migrated its ERP system (from TOTVS to SAP) and experienced a severe operational issue with the new implementation, which was resolved over the following two months but prevented the company from billing its usual order volume throughout Q1, significantly impacting its revenue for the period.

The inventory clearance and the ERP migration problem together led Multi to a loss of R$548 million over those two quarters — undoubtedly a significant destruction of value. However, before judging whether Multi's shares are worthy of investment, there are two important questions: i) will the harm suffered by the company have a temporary or lasting impact? and ii) does the current share price correctly reflect the expected business results?

Was the Harm Temporary?

The first question is the most important. If a business undergoes a structural transformation, its historical results become of little relevance in estimating its future. A well-known example is the story of Kodak, which was successful for more than 100 years but quickly succumbed after the emergence of digital cameras. So let us investigate the two problems Multi experienced.

The biggest problem was the excessive purchase of inventory of items that experienced overheated demand during the pandemic. After the purchases were made, only two alternatives remained for the company: continue selling at normal prices until inventory normalized, or sacrifice margins to clear excess stock more quickly. Since much of Multi’s inventory consisted of technology products, which lose value over time and can become unsellable (by becoming obsolete), the chosen alternative was to carry out the inventory clearance as a corrective measure. Despite the damage, we do not believe that this inventory sizing error will lead the company to new excessive purchases, inventory clearances, and negative margins. In addition to not being a systemic problem — since purchases of new products are not dependent on past purchasing decisions — the memory of the recent mistake acts as a certain antidote against repeating it in the near future. So much so that Multi is already moving in the opposite direction: it has been taking severe measures to reduce purchases and take less risk in the products selected to keep in inventory.

The second problem is easier to analyze. ERP migrations are non-recurring events, and SAP — the system Multi migrated to — is typically the definitive ERP adopted by large companies, meaning decades may pass before a new migration is necessary. In this context, it matters little whether the problem that occurred was unavoidable or the result of the company's lack of skill, since the business's future results depend almost not at all on the ability to repeat this process. One concern we had was the reputational damage caused by delayed deliveries to small retailers, but the vast majority of them had long-standing relationships with Multi, understood that the situation was temporary, and did not stop being customers as a result.

From this perspective, we believe it is correct to conclude that Multi has not undergone any transformation that will have a lasting negative impact on its future. Despite the poor recent quarters, the company continues to operate with the same business model that generated very positive results over the past decade, under the leadership of the same CEO who built the company's track record of success, who still holds a ~40% stake in Multi today and, during the share price decline following the weak results, purchased a significant volume of shares — signaling his confidence in the business. Furthermore, the latest quarter's numbers already show a good recovery in profitability and strong cash generation, indicating that the worst has passed.

Are Multi's Shares Cheap?

Estimating a company's value with a reasonable degree of accuracy requires detailed work in projecting its financial results and estimating how much cash flow the business will generate for its shareholders in the future (the discounted cash flow method). However, it is possible to get a sense of the minimum floor at which a business should be valued through less precise but faster and easier-to-understand analyses. That is what we will do here, presenting a considerably simplified analysis.

Multi posted R$4 billion in Net Revenue over the past four quarters. It is reasonable to assume that this revenue level is sustainable, since Brazilian retail was subdued during this period and some months were affected by the ERP migration issue. For reference, the company had already achieved Net Revenue of R$4.85 billion in 2021, a level 21% above current figures. Applying the average net margin of 11.7% the company posted over the past ten years, Multi's normalized Net Income would be R$468 million.

Today, Multi is valued at R$2.67 billion on the stock exchange (R$3.26 per share as of September 4), which would correspond to a Price/Earnings multiple of 5.7x. Compared to this figure, the average P/E multiple for companies listed on the B3 (ex-Petrobras and Vale) is 12.4x, over the period from January 2005 to July 2023. Another reference is that listed companies selling products similar to part of Multi's portfolio (Intelbras, Positivo, and Allied) traded at average P/E multiples of 11.6x over the past two years. Against these benchmarks, Multi today would be valued at a discount of around 50%. It could further be argued that its multiple should be higher than the Brazilian stock market average, given that it has growth rates superior to most other listed companies.

From another angle, Multi's book equity today stands at R$3.75 billion. If it is able to generate returns on equity at the historical average of 20.8%, the Net Income generated would be R$781 million. If we are more conservative and assume its future return on equity will be 15% (28% below the historical average), the company would still generate R$563 million in profit and the implied P/E multiple would be 4.7x.

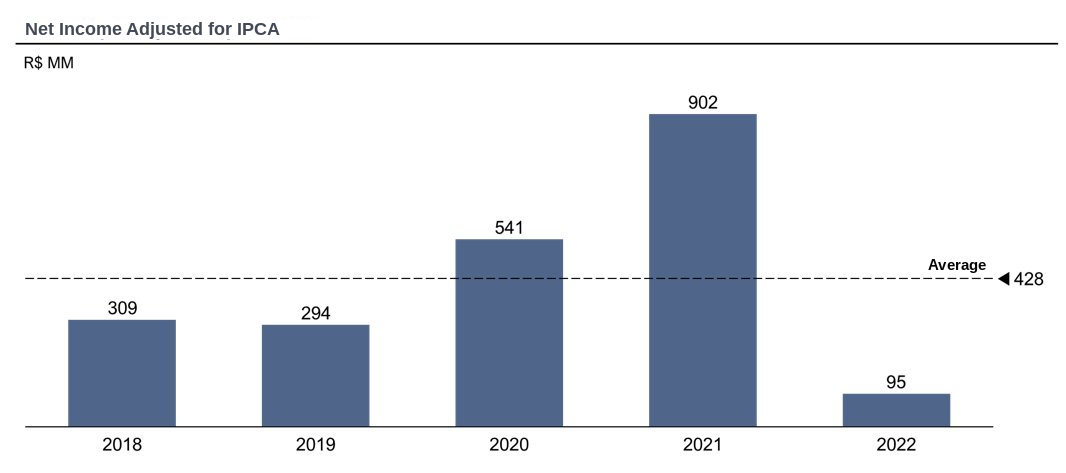

A third check is to assess the profits already generated by Multi over the past five years, adjusted for IPCA inflation, to estimate the corresponding values in 2023-equivalent Brazilian Reais. This period includes three pre-IPO years, before Multi raised R$1.9 billion to invest in its business growth, and the year 2022 with its profitability affected by the inventory clearance. Even so, the average profit level over the period was R$428 million, which would imply a P/E multiple of 6.2x.

Regardless of the angle of analysis, it is clear that Multi's shares are quite cheap. If the company grows at half the rate it did in the past and recovers profitability even minimally close to its historical levels, there will already be a significant appreciation relative to the current share price. If Multi returns to its historical performance, growing at over 20% per year with over 20% return on invested capital, the potential investment return is enormous.

Although the analyses presented here are quite simplified, the result of our detailed analyses points in the same direction.

Final considerations

Like every thesis, this one has its risks. The main ones are the possibility that Brazilian retail remains subdued, which could hurt both sales volumes and margins, and the risk that some tax change — amid the various measures the current government has been trying to implement to increase revenues — could negatively impact the company. However, the current share price of Multi seems to us so far below what would be reasonable that the investment can deliver an attractive return even if some moderate-impact negative events occur.

Another consideration is that we tend to spend much more time analyzing risks than possible positive events, but Multi has invested in several initiatives that could deliver results beyond what we estimate in our projections. For example, the company recently established several partnerships with internationally renowned brands, began producing small appliances, and entered the electric motorcycle market. These initiatives are still in an embryonic phase and generate revenues that are not yet meaningful to the business as a whole, but they could grow quickly and become relevant additions.

We assign little weight to these positive factors because it is common for investors to entertain themselves with the possibilities of exceptional gains and attribute excessive value to the chance that optimistic scenarios materialize. We prefer to follow a more prudent approach: maintaining focus on the risks of each investment, estimating the value of the business based on normalized result averages, and requiring a reasonable margin of safety in the entry price of new theses. If unforeseen positive events occur over time, they will always be welcome surprises.