Investment Case: Wilson Sons

Dear investors,

Wilson Sons has been part of our portfolio since late 2018 and is currently a meaningful position in the fund. We decided to share this case because it is a good example of our investment philosophy: for more than two years, the share price moved sideways while the company continued to deliver solid operational results, even amid the crisis.

The company is traded in Brazil through BDRs (Brazilian ADRs), which has historically limited its coverage among investors. This changed in May 2021, when the company announced its intention to convert the BDRs into common shares and list on the Novo Mercado segment of B3. This relatively simple move brought greater visibility to the stock and contributed to a 24.8% appreciation since the announcement.

Below, we outline our investment process in the company—from the initial entry into the position to our current view on the investment.

Our Investment

Our relationship with Wilson Sons goes back several years. We first began analyzing the company in mid-2017 and had a very positive initial impression. However, there were some uncertainties in the thesis, so we decided to monitor the company for a period before investing. At the time, our main concerns were related to a potentially challenging competitive environment in the towage segment and the risk of discontinuity in its container terminal (Tecon) operations if concessions were not renewed.

After more than a year of close monitoring, we became increasingly comfortable with the risks that had initially concerned us and decided to initiate a position in November 2018. There were several factors that could benefit the company over the medium term—such as an economic recovery, expectations of lower capex levels in subsequent years (enabling higher cash distributions), and operational improvements. However, what stood out most to us was the asymmetric risk profile of the investment.

From a business perspective, Wilson Sons operates with stable and recurring results, with limited disruption risk. From a valuation standpoint, the company also appeared significantly undervalued. In particular, it was noteworthy that the company had invested more than USD 1.0 billion in its operations over the previous ten years—an amount that exceeded its market capitalization at the time.

For two years following our initial purchase, the investment in Wilson Sons delivered modest returns, with the share price moving sideways despite the company continuing to report solid operational performance. We used this period to steadily increase our position.

In 2021, our discipline and patience were rewarded. Since initiating the investment, the stock has appreciated by 100%, resulting in an annualized IRR of 37% for the fund.

Chart 1 – WSON33 share price and key investment milestones

As we have mentioned in previous letters, it is not enough to identify great businesses—the challenge lies in investing in them at the right price. In Wilson Sons, we believe we found an excellent combination of both.

Company Overview

Wilson Sons is a company with more than 180 years of history, operating in the port and maritime services sector. As an interesting fact, it is the oldest Brazilian company listed on the stock exchange—even older than Banco do Brasil. The company operates across seven different segments: (1) maritime towage, (2) container terminals (Tecon), (3) offshore support vessels, (4) offshore support bases, (5) logistics centers, (6) shipping agency services, and (7) shipyards.

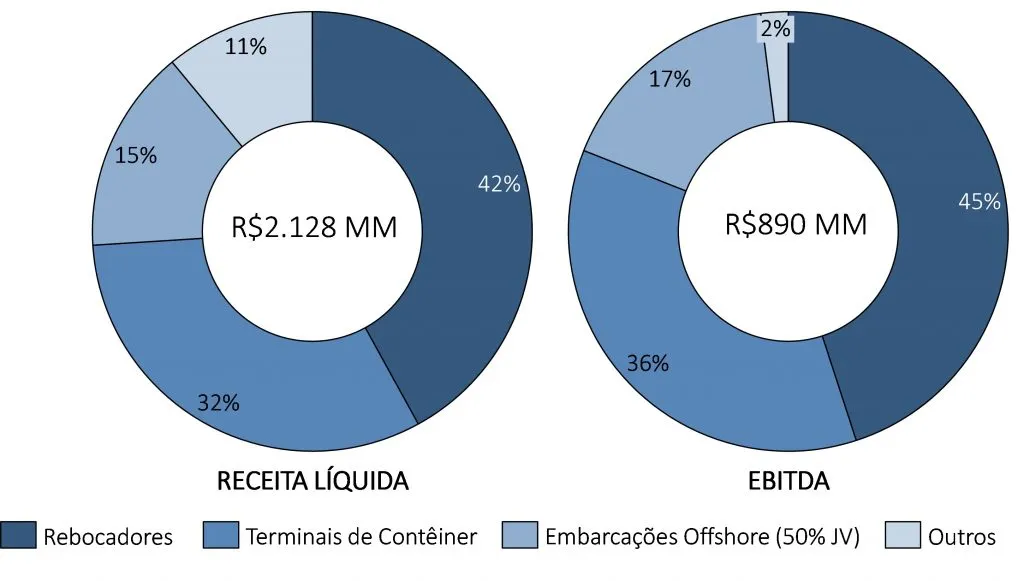

The first three segments are the most relevant to the company, as illustrated in the chart below.

Chart 2 – Net Revenue and EBITDA by Business Unit (% , 2020)

1. Towage (42% of 2020 revenue and 45% of EBITDA):

Towage vessels (tugboats) are small but highly powerful boats, used to assist large ships during berthing and unberthing operations at port terminals. The use of towage services is mandatory for shipping companies (shipowners) responsible for docking operations, and the activity is monitored and regulated by the Brazilian Navy.

Wilson Sons is the market leader in Brazil, operating a fleet of 80 vessels across all major Brazilian ports (35 ports). In terms of number of maneuvers, the company holds an estimated market share of approximately 40–50%.

Chart 3 – Brazilian Towage Market (fleet size, Mar/2021)

2. Container Terminals – Tecon (32% of 2020 revenue and 36% of EBITDA):

Wilson Sons operates two container terminals (Tecons) in Brazil: Rio Grande (Rio Grande do Sul) and Salvador (Bahia). Containers are widely used for transporting goods such as plastics and resins, agricultural products, paper and pulp, among others.

Both of Wilson Sons’ terminals rank among the most important in the country:

Chart 4 – Main container ports in Brazil and throughput by port

3. Offshore Support Vessels (15% of 2020 revenue and 17% of EBITDA):

Wilson Sons operates a fleet of 23 offshore support vessels through its subsidiary WSUT (a joint venture, 50% owned by Wilson Sons and 50% by the Chilean group Ultramar). These vessels provide support for oil exploration and production activities, particularly for Petrobras.

These vessels are typically contracted under agreements with an average duration of approximately two years.

Investment Thesis

Our investment thesis is based on three main pillars:

1. Strong market positioning in its core segments (towage and container terminals)

As mentioned earlier, Wilson Sons is the market leader in the Brazilian towage segment, with a 40–50% market share. This leadership position provides the company with several important competitive advantages, including: Extensive port coverage, allowing shipping companies to rely on a single provider across multiple ports in Brazil; A 24/7 centralized operations center, monitoring all vessels in real time, enhancing safety and operational efficiency (including fuel savings); An in-house shipyard, used for both construction and maintenance of its fleet.

The result of these advantages is a structurally higher level of profitability compared to its peers:

Chart 5 – EBIT Margin Comparison: Wilson Sons (Towage) vs. Peers

In this segment, supported by high margins and access to low-cost financing, Wilson Sons consistently delivered an average ROE above 20%.

In the container terminal (Tecon) segment, the company operates the only terminals in their respective states (Rio Grande do Sul and Bahia). In both cases, the nearest competing terminals are at least 700 km away, effectively creating captive markets and conferring characteristics of geographic monopolies. The result is a highly profitable operation, with ROE close to 30% in this segment.

There is additional comfort regarding this business due to two key factors: (1) concessions are long-term (Rio Grande expires in 2047 and Salvador in 2050); and (2) there are no announced competing terminal projects (and even if there were, new terminal developments typically take several years to be completed).

2. Well positioned to capture growth in foreign trade, likely to accelerate with economic recovery

Even amid the economic challenges of the past decade, trade flows have continued to grow—albeit at a slower pace than in the previous decade, which benefited from a more favorable macroeconomic environment. In both periods, containerized cargo grew at a faster rate than overall trade volumes:

Chart 6 – Growth in Trade Flows in Brazil vs. GDP Growth

| % Annual growth | Period 1 (2002-2010) | Period 2 (2010-2020) |

|---|---|---|

| GDP | 4,0% | 0,2% |

| Goods transported in ports (MM ton) | 6,0% | 3,2% |

| Goods transported in ports via container (MM TEU) | 11,5% | 3,7% |

The data above highlight two key points: (1) even during a decade of near-zero economic growth, trade flows proved resilient, growing at a reasonable pace of 3.2% per year (3.7% for containers); (2) with a stronger economic environment, it is reasonable to expect a more robust growth trajectory for trade flows going forward.

The data above highlight two key points: (1) even during a decade of near-zero economic growth, trade flows proved resilient, growing at a reasonable pace of 3.2% per year (3.7% for containers); (2) with a stronger economic environment, it is reasonable to expect a more robust growth trajectory for trade flows going forward.

This expansion in trade flows should benefit both Wilson Sons’ container terminal and towage operations.

In addition, the company has made significant investments over the past decade. In recent years, these investments have been focused primarily on renewing and expanding its towage fleet and increasing cargo-handling capacity at its container terminals. These initiatives position the company to capture another important industry trend: the increasing average size of vessels calling at Brazilian ports. To accommodate larger ships, Wilson Sons stands out for its powerful towage fleet and well-equipped terminals (particularly in terms of port draft).

Finally, it is worth noting that the company’s offshore support segment has been significantly impacted since 2015 by the downturn in Brazil’s oil and gas sector, which led to a sharp decline in vessel utilization rates—affecting both volumes and contract pricing. With the continued development of the pre-salt fields (with up to 18 new platforms expected by 2024), the outlook for the sector has improved, which should support a recovery in this segment over the medium term.

3. Lower Investment Requirements (Following a Period of Heavy Capex) Will Support Stronger Cash Generation in the Coming Years

As mentioned earlier, Wilson Sons has made significant investments over the past decade. A key highlight is the expansion of the Salvador container terminal, completed in March 2021, which increased capacity by 110%. As a result—particularly in the terminal segment—the company now has ample room to grow without the need for additional major investments for several years, enabling higher cash generation and potentially increased dividend distributions.

Chart 7 – Historical Capex and Dividends

It is also worth noting that, despite the challenging macroeconomic environment of the past decade, Wilson Sons demonstrated strong resilience, growing its results at a compound rate of 16% per year between 2011 and 2020. During this period, the company implemented operational improvements and benefited from currency tailwinds, as a significant portion of its revenues is dollar-linked:

Chart 8 – Historical Net Revenue and EBITDA

Valuation

From a valuation standpoint, our estimates suggest that—even under conservative assumptions—the company remains undervalued, despite the recent appreciation in its share price. We estimate that Wilson Sons is currently trading at approximately 12–14x its normalized cash generation, which appears attractive. Combined with the company’s favorable growth outlook—particularly given that growth can be achieved without significant incremental capital expenditures—we believe this represents a compelling investment opportunity.

On a relative basis, the table below indicates that Wilson Sons remains the most attractively valued company in its sector:

Chart 9 – Valuation Multiples Comparison4

1 BDRs (Brazilian Depositary Receipts) are share certificates for companies headquartered abroad. They operate similarly to common shares.

2 From the announcement on 05/23/21 to the closing price on 06/14/21

3 IRR: Internal rate of return. This metric represents the fund's annualized return.

4 Reference date 06/11/2021