Dear investors,

In January 2020, we sent a letter commenting on our portfolio management process and our strategy for determining the percentage of equity allocated to each position.

One aspect of Arcadia's strategy that we consider quite different from that practiced in the Brazilian market concerns the degree of diversification. Despite being a common practice in developed markets like the United States, we realize that more concentrated investment strategies are rare in Brazil, and often treated as “taboo”.

Throughout this text, we present the main reasons behind our strategy of holding between 5 and 15 companies in the portfolio, with holdings ranging from 5 to 25% of the fund's equity.

1. Concentration allows for greater potential return

Our philosophy is based on allocating relevant portions of our capital to the theses in which we are most convinced. We differ from most investors when it comes to diversification because we believe that excellent investment opportunities are rare, and our top 10 theses will always have a much higher potential return than our top 50 theses. In a portfolio of 50 stocks, the 50th stock has a worse expected return than the 1st stock, so adding it to the portfolio should reduce the potential gain for the portfolio as a whole.

So we focused more on the few great investments we found, rather than also investing in middling potential opportunities just for diversification purposes.

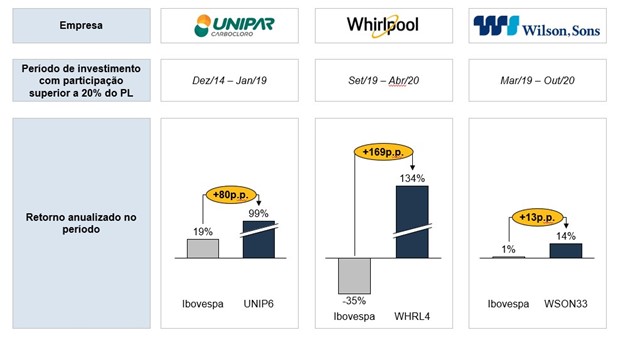

Throughout our history, we have already had 3 investments that have surpassed the portfolio's 20% barrier. In all these situations, the returns obtained were much higher than the market in general in the respective periods and contributed significantly to Arcádia's historical performance.

Graph 1 – Investments with a relevance greater than 20% of Shareholders' Equity

“ In the field of common stocks, a little bit of a great many can never be more than a poor substitute for a few of the outstanding” –Phil Fisher

The natural question that arises after this explanation is the following: “Does this approach not generate more risk for the portfolio?”

In our view, no. The justifications appear in the topics below.

2. Focus leads to greater depth in invested companies

A more concentrated portfolio forces us to be more careful in our decision-making process, getting to know the companies better and the risks involved in each investment. Even after the detailed analysis, the investment will only have a significant presence in the portfolio when we have a very high level of confidence in the thesis.

Obtaining this level of confidence requires considerable study and follow-up time. This level of dedication is not possible in a very diversified portfolio, so we prefer to focus on a maximum of 15 investments at a time. In addition, between invested and followed, each Arcadia analyst covers a maximum of 10 companies.

When concentration is accompanied by a deep level of knowledge of the assets and discipline and patience to invest only when there is a significant margin of safety, there is a reduction in investment risks.

“ Diversification is a protection against ignorance. It makes very little sense for those who know what they are doing” –Warren Buffett

3. Few stocks are enough to capture the benefits of diversification

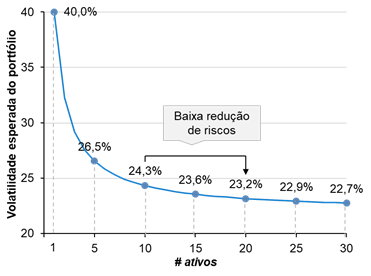

Many seek diversification as a means to reduce portfolio volatility and risk (“not putting all your eggs in one basket”). Although it makes intuitive sense, the numbers show that the volatility reduction benefit decreases dramatically from about 5 invested companies.

The graphic below illustrates this concept. It presents the expected volatility of a portfolio according to the number of invested companies and it is evident that the risk profile of a portfolio with 10, 20 or 30 assets is very similar.

Graph 2 – Decreasing benefits of diversification (portfolio volatility vs. number of assets held)[1]

If a portfolio of 10 shares has a risk profile similar to a portfolio of 30, and brings a higher return perspective, it doesn't seem to make sense to invest in the more diversified portfolio.

“The number of securities that should be owned to reduce portfolio risk is not great, as few as ten to fifteen holdings usually enough”Seth Klarman

4. Diversification does not protect against systemic risk

There are two types of risk to consider in portfolio construction: Non-systemic and systemic risks.

Non-systemic risk is risk that affects specific companies or industries. Examples include: regulatory changes affecting a particular industry; companies exposed to technological obsolescence; companies with accounting fraud; etc. This is the risk that diversification seeks to protect, but as we saw in the previous section, a portfolio of 5 to 15 stocks does a good job of providing such protection.

Systemic risk is one that affects the market as a whole. For example, an increase in interest rates in the economy reduces prices in the stock market as a whole, regardless of the company or sector in which it operates. In this scenario, portfolio protection is not obtained through diversification, but with hedging mechanisms, or allocation to other asset classes (eg, increasing the portfolio's cash position).

The Covid-19 crisis in March 2020 was an example of systemic risk, affecting the market as a whole. During the crisis, all stocks fell together and diversification did not bring greater protection to investors, precisely in that period when they needed it most. Proof of this is that, in the Covid-19 crisis, Arcadia dropped 34% against a drop of up to 47% on the Ibovespa (an index with more than 60 assets) in the same period.

5. There are few companies listed in Brazil

The arguments in points 1 to 4 above are valid worldwide. Even on the American stock exchange, with more than 5,000 companies listed, this level of 5 to 15 investments is enough.

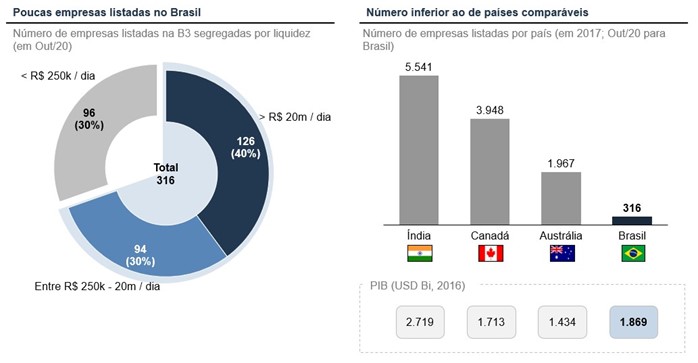

In Brazil, there are a much smaller number of listed companies. In October 2020, there are 316 companies listed in Brazil, of which 96 have very low liquidity (less than R$ 250 thousand per day), leaving only 220 as legitimate investment opportunities. With a higher liquidity bar (R$ 20 mm per day), the number of companies left is only 126.

For comparison purposes, countries like India, Canada and Australia, which have a GDP similar to that of Brazil, have 5 to 20x the number of listed companies. The graphs below illustrate these numbers:

Graph 3 - Number of companies listed in Brazil and comparison with other countries

With only 220 companies with investment potential (122 with the liquidity bar of many investors), it doesn't seem to make sense to put together a highly diversified portfolio. A portfolio of 50 assets is making a bet that almost 25% of the companies on the exchange are good investments at that moment (good companies at the right price), which doesn't seem very likely to us.

In summary, maintaining a portfolio of 5 to 15 companies allows us to focus our bets on the best investments, understand the companies we invest in well, and maintain a comfortable level of diversification.

Our comfort level with this level of diversification is reflected in the size of our personal investments in Arcadia – today, 58% of Arcadia Equity is our team capital.

[1] Assumptions: (a) standard deviation per asset of 40% (average standard deviation in Brazil); (b) 30% correlation between assets (historical average of shares); (c) assets held with equal weights