Dear investors,

At the beginning of the year, the market turned its eyes to Brazil's macroeconomy. With the high interest rate and the political uncertainty expected for the year, the themes of the moment are interest rates, inflation, exchange rate, GDP and elections. This scenario is causing Brazilian institutional and individual investors to migrate their capital from the stock exchange to fixed income, while, interestingly, foreign investors are on the other side of the operation, buying shares on the Brazilian stock exchange. In this letter, we will explain which side we are on.

Interest and the Stock Exchange

As a rule, investors buying stocks demand an expected return that is always above the basic interest rate, since they are subject to more risks buying shares in companies than buying fixed income securities. The higher the return demanded by the investor, the lower the price he is willing to pay for a share, since the main methodology for estimating the value of a company is based on the projection of how much money your business will be able to generate in the future. each year and discounts that cash flow at the investor's target rate of return. In this way, the greater the target return, the greater the discount applied to the cash flow and, consequently, the lower the result of the price estimate for the company.

Thus, when the basic interest rate rises, the required return on investments in stocks also rises and the practical effect is that the market starts to assign a lower price to stocks, causing the stock market to fall. This logic may seem to justify the migration of capital from the stock exchange to fixed income, but note that the movement only makes sense if done before interest rates rise, as, after the rise, the stock market has already dropped and you would be selling cheap stocks. In turn, carrying out the movement before the interest rate rise brings a more fundamental problem: how to know when interest rates will rise?

Because of this problem, we follow an investment philosophy that is not based on macroeconomics. We used the example of interest rates, but it extends to other macroeconomic factors and is a little more complex: the market already considers a projection of how interest rates will evolve over the years, so we would need to know when interest rates will rise (or fall) with more accurately than the market already considers in its expectations. To illustrate how difficult it is to project macroeconomic variables, let's evaluate the experts' hit rate over the past 20 years.

Experts' projections

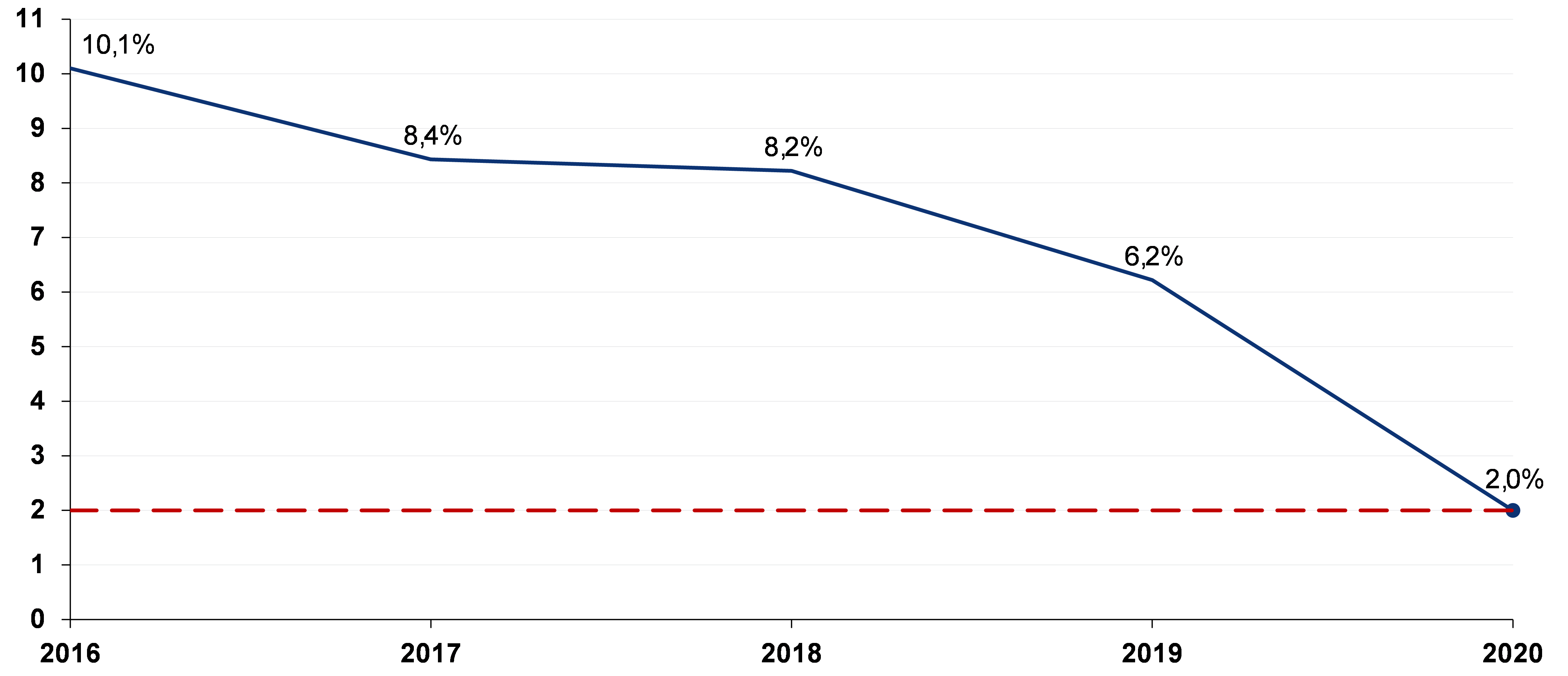

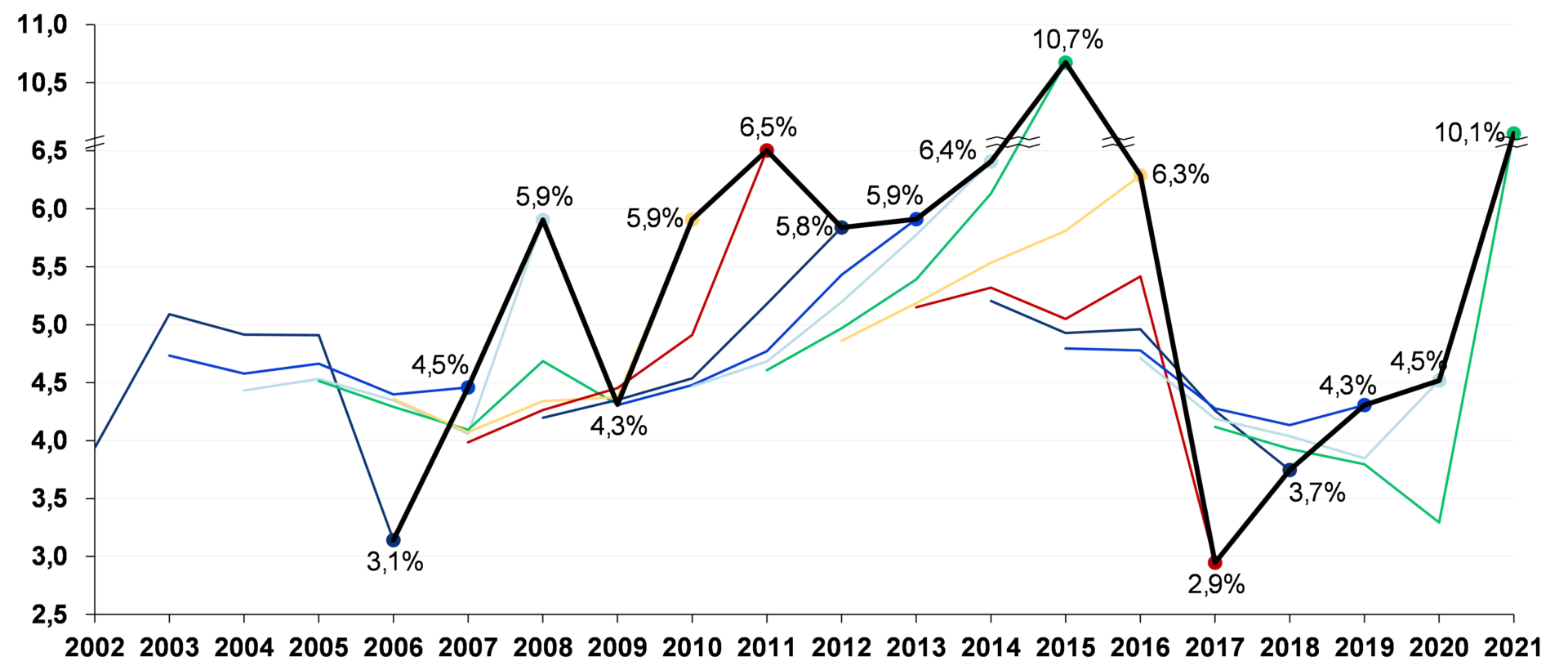

We analyzed data published by the Central Bank's Market Expectations System, which daily collects forecasts on macroeconomic variables produced by around 130 institutions participating in the financial market and consolidates this data into statistical series. With this information in hand, we verified the value projected by the market 4 years prior to the projection date. See this example illustrating the logic for building the graphs, considering the projection only for the 2020 SELIC rate.

The interpretation of the graph below is: in 2016, the market projected that the 2020 SELIC rate would be 10.1%, in 2017, it projected that it would be 8.4%, and so on, until the year 2020, when the SELIC rate performed was 2% . Note that if the market had hit the realized rate during the previous 4 years, the graph would be the red dotted line on the graph.

Projection for the 2020 SELIC rate

If the market were always correct in the projections for the SELIC Rate, the long-term graph with the projections and forecasts would be as illustrated below:

Graph if the projections for the SELIC rate were always correct

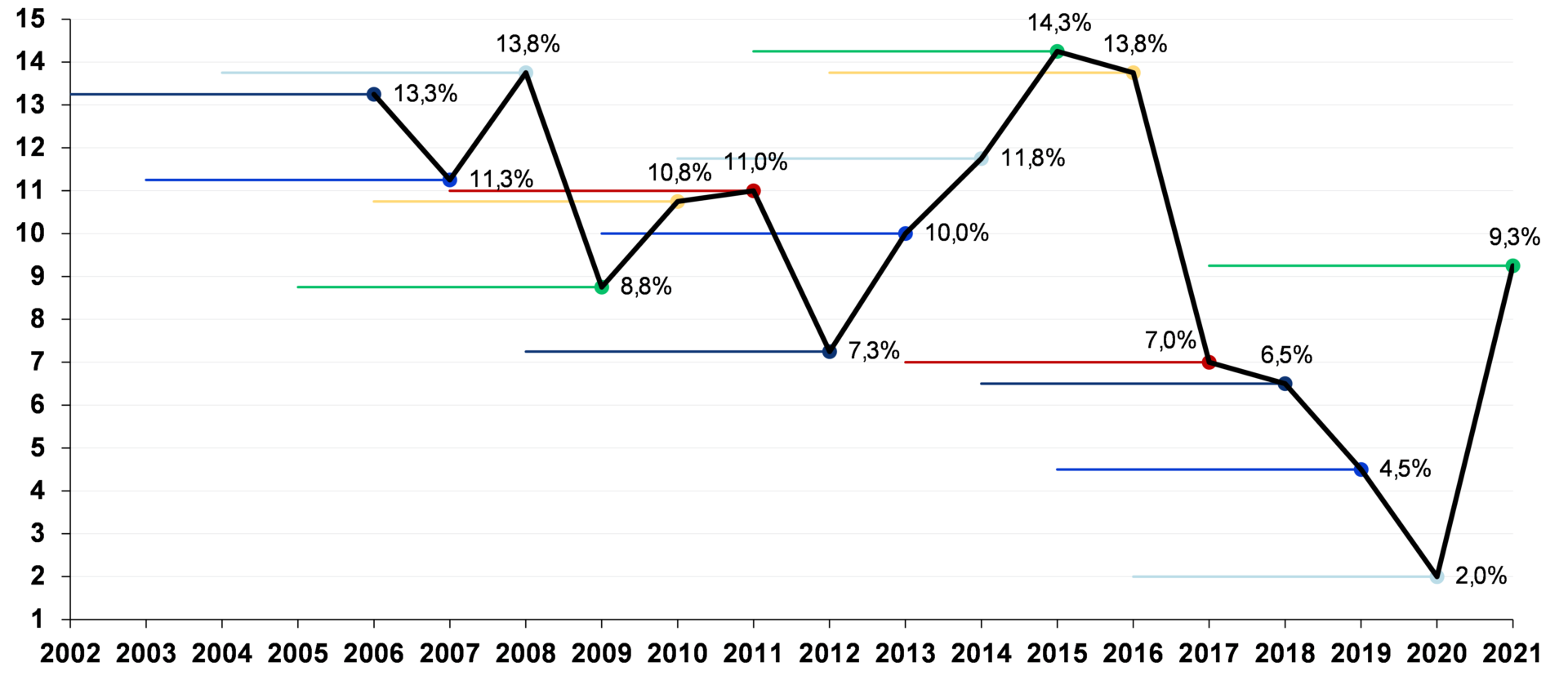

Now let's go to the graphs comparing the real projections for the SELIC Rate, GDP, Dollar (USD/BRL) and IPCA with the values achieved over the last 20 years. They are a bit complex, but the way to interpret them is: the more curved the colored lines, the greater the errors in the market projections. The black line represents the realized values.

Projections vs. amounts realized - SELIC Rate

Observe how the projections are very much anchored in the interest rate at each moment. Projections for the 2021 SELIC rate followed the evolution of the rate between 2017 and 2020, making the projection made in 2020 for the following year more wrong than the projection made in 2017 for 2021.

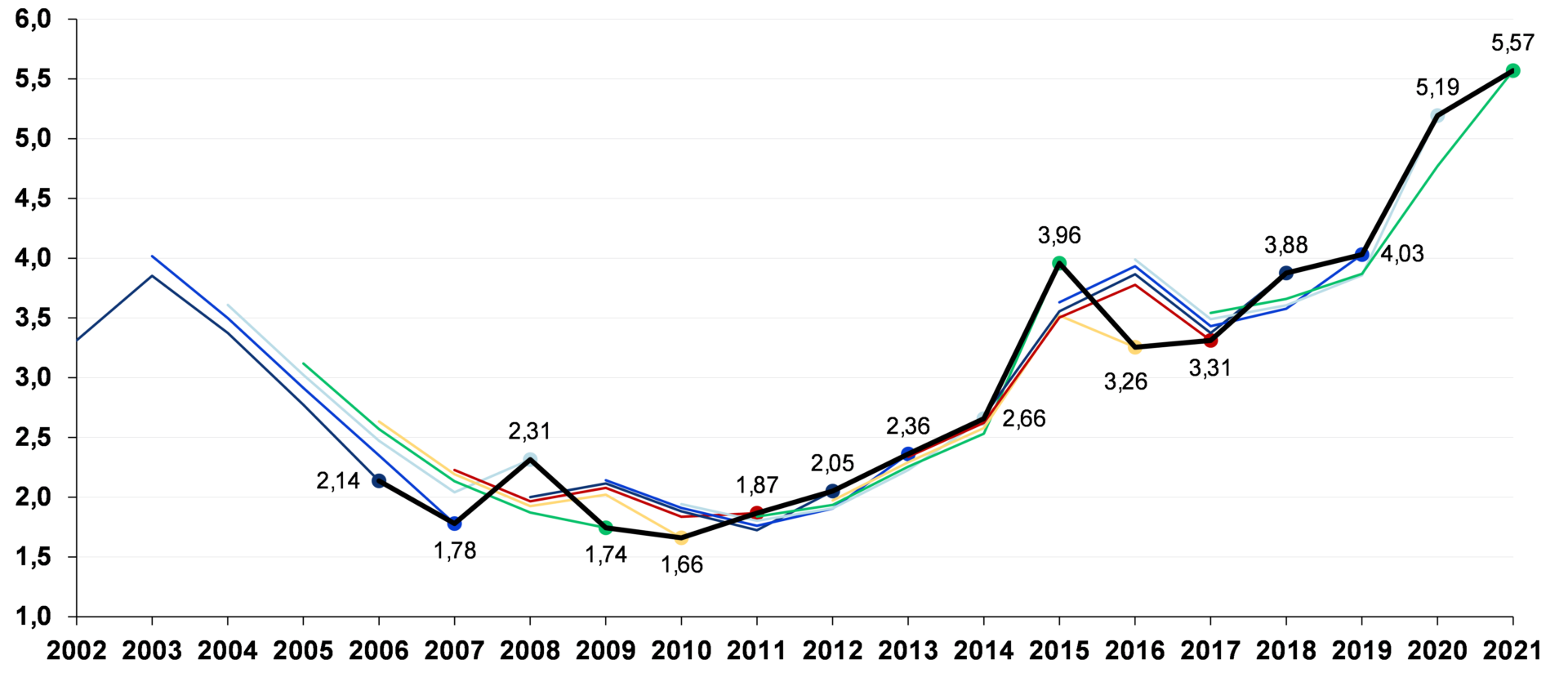

Projections vs. Realized values - Dollar (USD/BRL)

For the dollar, the anchoring effect of the exchange rate at each moment is again visible. The projections vary little in relation to the exchange rate at the time they were made, and their predictive power is quite low.

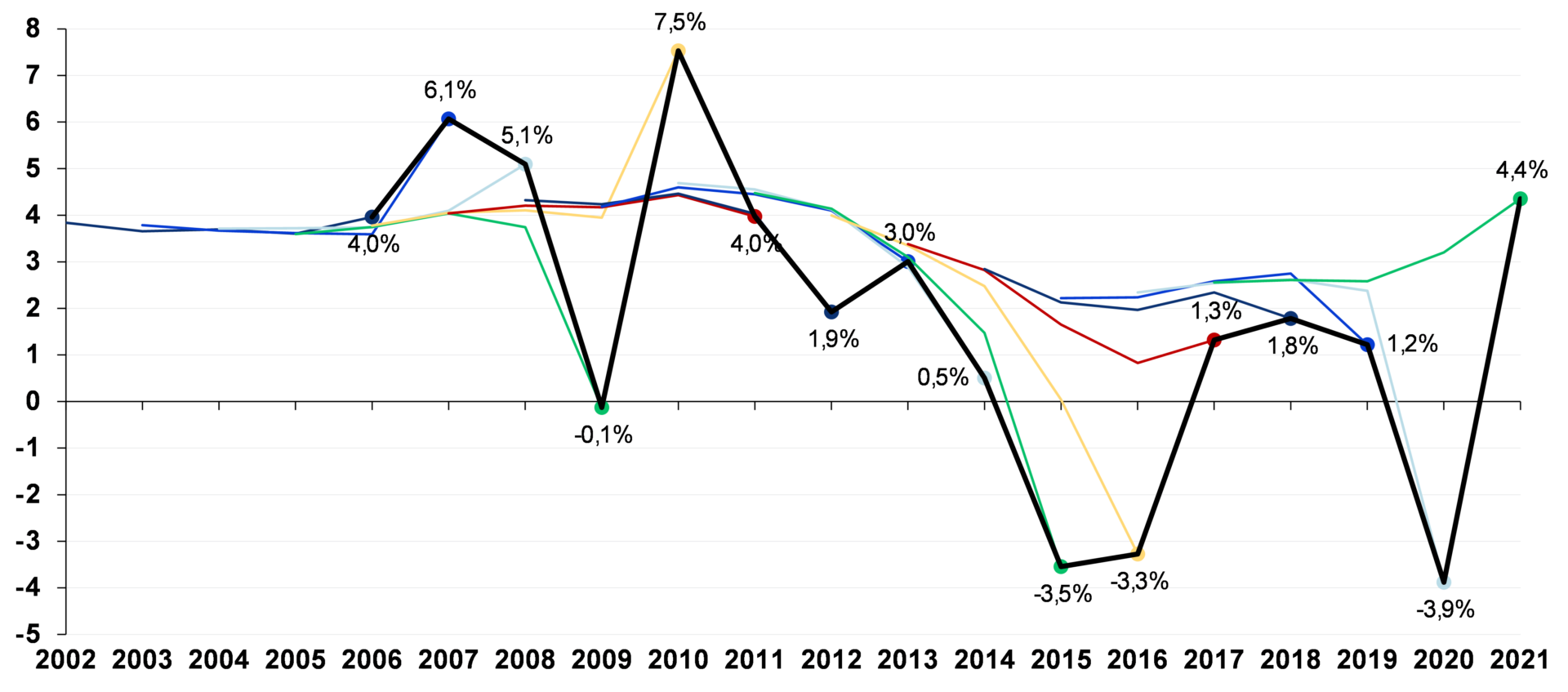

Projections vs. realized values – Brazilian GDP growth

In GDP projections, the market seems to always consider an average growth rate, between 2-4%. All the years of growth outside this range were not anticipated by the market.

Projections vs. realized values - IPCA

For inflation, the same effect is present: the market typically expects something between 4.0 and 5.5%, and is wrong every time real inflation falls outside this range.

In short, market projections for the main macroeconomic variables are far from being accurate... Remembering that these projections are made by teams of specialists from the largest financial institutions in Brazil, so it seems unreasonable to expect that someone will be able to get much more right than do this consistently over time.

our approach

We deal with this problem in a simple way, but one that has worked for us for almost 9 years, and has worked for other investors with similar investment philosophies for several decades: we don't try to project macroeconomic scenarios. This position stems from the reflection that, however uncomfortable it may be to live with this uncertainty, there is no benefit for our investments in replacing the discomfort of uncertainty with the comfort of an illusion of knowledge about the future.

Assuming that it is not possible to predict the macro future, the strategy of buying stocks when the macro scenario is good and selling when it is bad would lead to the undesirable result of buying high and selling low.

Another important consideration is that, in long-term theses like ours, it is likely that we will go through both good and bad years, from the macroeconomic point of view. So, our strategy is to identify good companies with resilient business models, which are capable of going through the crises that will certainly happen in the future, and buy shares in these companies when their prices are very attractive, regardless of the macro scenario at the time.

what are we doing now

Finally, to practice. We are now on the side of foreign investors, buying the shares of our countrymen who decided to migrate to fixed income, as the Brazilian stock market seems cheap to us and we are finding interesting investment opportunities in a quantity that we have not seen for years.

After the recent stock market crash, we were able to allocate a good part of the capital that we had kept in cash for months. At the same time, this year Ártica's partners and management team made new contributions to our fund, as well as several people who have already invested with us for some time and also decided to allocate more capital to Ártica Long Term FIA.

We thank our investors for their trust, for sticking with us even when we decided to go against the current, and we remind you that the crowd must still be for the stock market to fall, as we want to buy new shares as cheaply as possible!