Annual Letter 2020

Dear investors,

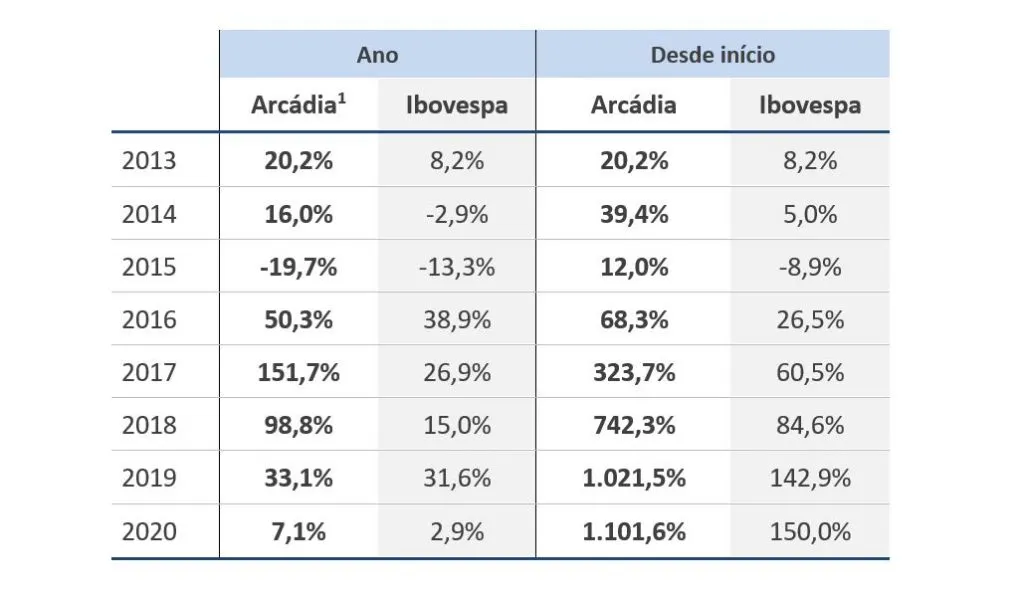

We ended 2020 with an annualized return of 7.1%, higher than the Ibovespa and the CDI, which totaled 2.9% and 2.8%, respectively, during the period. The cumulative return since the Fund's inception, approximately 7.5 years ago, is 1,102%, representing an annualized return of 39.2%:

2020 Retrospective

2020 was a challenging year for everyone. It was marked by the Covid-19 crisis, which, in addition to its dire humanitarian consequences, brought enormous volatility to financial markets.

With the Ibovespa surprisingly ending 2020 in the green and close to its all-time highs, the days of extreme uncertainty we experienced at the beginning of the year seem distant. It's worth remembering that circuit breaker1 of the Ibovespa was activated 6 times in the year (record historical record along with 2008) and, in March 2020 alone, the index accumulated losses of 30%, the worst month since August 1998 and the fourth worst in history. Between January and March 2020, the Ibovespa had an accumulated drop of 47%, losing almost half of its value in just two months.

This enormous volatility has brought important lessons for investors:

The first and most important is portfolio risk management. As we published in our October 2020 monthly letter, we believe that the best way to manage portfolio risk is not by diversifying investments across dozens of theses, but rather by thoroughly analyzing each investment opportunity, carefully selecting companies with high return potential, resilience to navigate diverse economic scenarios, and a robust capital structure. We have always kept our portfolio concentrated in our best theses, which for many is synonymous with greater risk, and we have successfully navigated not only this Covid-19 crisis, but all others that have occurred since our founding in 2013.

Another important lesson was the importance of focusing on the long term. During the crisis, investors with a long-term perspective had the serenity to analyze and understand that the crisis was temporary and that, over time, the economy and good companies would recover. A drop in stock prices was a short-term phenomenon and could present an excellent buying opportunity.

That's exactly what we told our investors on March 20, 2020:

"We believe this could be one of those rare opportunities to make a good stock market investment. This is a severe but temporary crisis. Some companies may fall by the wayside, especially the most leveraged and exposed to hard-hit sectors, but those that survive should not see their results affected in the long term. We are firmly convinced that all the companies we invest in and would like to invest in belong to the second group. In just a few weeks since the crisis began, new contributions to our fund already represent 110% of the total capital contributed in 2019. And, of these contributions, 75% was money from our team (or from family members, at our recommendation). Many investors ask us to tell them when is a good time to invest. We believe this is a good time."

Case CEB

In this letter, we will share a case recent and little known about the fund: the investment in Companhia Energética de Brasília (CEB).

CEB gained notoriety at the end of 2020 with the successful privatization of CEB-D (its energy distribution subsidiary), which was sold to Neoenergia for R$2.515 billion, and its share price rose to R$1801 in 2020, higher than any share on the Ibovespa index.

The privatization took place in December 2020, but our investment in the company began in 2019. Below, we detail our investment process in CEB and comment on the current outlook, given that it still represents an important position for the fund.

Chart 1 – Price per share of CEB (CEBR6) and main milestones

Context and initial investment

CEB is a state-owned company controlled by the Federal District government, with a stake of 80%. The remaining 20% are traded on the B3 (Brazilian Stock Exchange). Its most liquid asset classes (ON: CEBR3 and PNB: CEBR6) are sparsely traded on the stock exchange (daily liquidity of approximately R$$ 500,000/day), and therefore, the company was (and still is) overlooked by many investors. This lack of coverage created a huge investment opportunity for us in 2020.

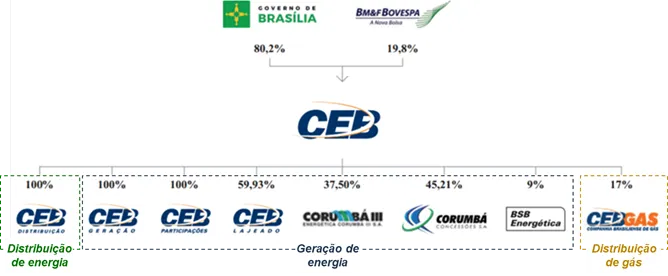

The company operates in the areas of energy distribution, generation, and marketing through eight subsidiaries. The figure below presents CEB's corporate structure:

Chart 2 – CEB’s corporate organization

CEB's main asset is CEB Distribuição SA (CEB-D), which holds the concession to operate energy distribution in the Federal District.

CEB-D is a loss-making company in a difficult financial situation, driven by high personnel costs and an inflexible cost structure (as a state-owned company). Due to electricity sector regulations, which require companies to maintain minimum levels of financial health, CEB-D was at risk of losing its concession.

To address this problem, the company's solution was to privatize CEB-D, a plan that gained momentum with the election of a more liberal district government. In June 2019, the company's privatization was approved by its shareholders, and BNDES was hired to advise on the transaction.

CEB-D also had some characteristics that caught our attention and could make it a highly sought-after target for private companies in the sector:

- Operating in one of the richest regions of the country, with low default rates;

- High density of consumers per km of energy distribution line, which reduces the need for investment per consumer and increases the profitability of the operation; e);

- Low rates of network failures and interruptions compared to other state-owned companies, indicating a high-quality infrastructure without the need for major investments in adjustments after the eventual acquisition.

Given the sector's successful history of privatizing state-owned companies (companies like Equatorial and Energisa have managed to generate enormous value for their shareholders by acquiring state-owned companies and making them more efficient), the news of CEB-D's privatization immediately caught our attention and led us to study the case.

In addition to energy distribution, the company also plays a significant role in generation, where it has solid assets and very stable cash flow. Among these, four hydroelectric plants (Lajeado HPP, Corumbá III HPP, Corumbá IV HPP, and Corumbá Queimado HPP) stand out, with a combined installed capacity of 200 MW.2 and concessions expiring between 2032 and 2037.

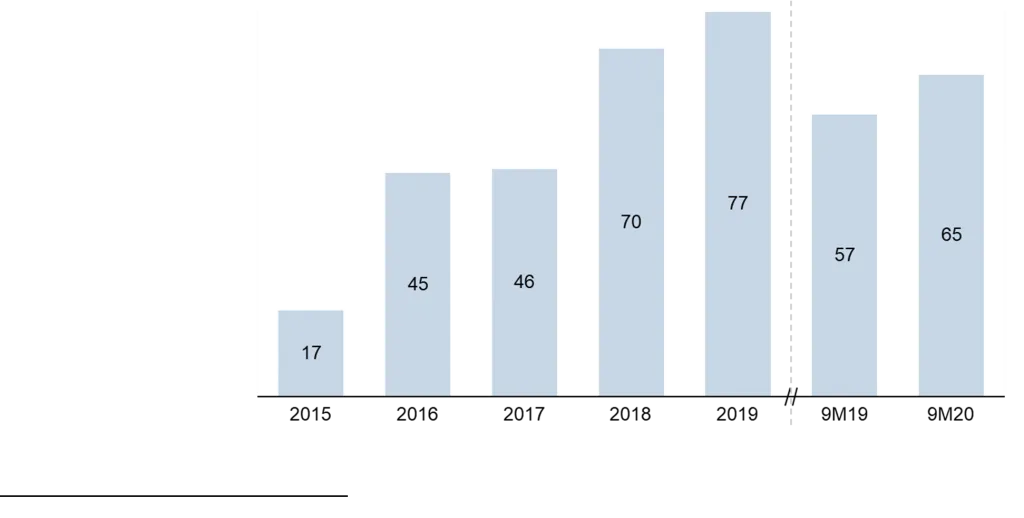

The results of these generators caught our attention due to the profit growth observed over the last 5 years, as shown in the graph below.

Chart 3 – Net profit from CEB generation operations (in R$1.4T million)

The main reason behind this growth is the reduced leverage of one of the concessions (Corumbá IV), which still had high debt due to the investments required to build the plant. With cash generation in recent years, the company was able to pay off a large portion of this debt and significantly reduce its financial expenses. With a reduced debt level, we expect results to be even better in the coming years.

Despite these positive results, the cash generated by the generators was largely used to cover CEB-D's losses. Thus, after privatization, the consistent positive results of these companies should be more evident in the company's financial statements.

Estimate of valuation e gestão de risco no portfólio

With the context explained, let's move on to our analysis of the company's potential value. Considering that CEB was a holding company with several subsidiaries operating in different areas, it makes sense to calculate the company's value using a "sum-of-the-parts" methodology.

Para isso, o primeiro passo foi estimar o valor das geradoras. Considerando seu perfil de geração de caixa e o prazo de duração de suas concessões, estimamos, de forma conservadora, que tais empresas tinham valor conjunto de R$ 600-700 milhões, o que representava múltiplos de EV/EBITDA de 6,0x e EV/Capacidade instalada de R$ 4,0-4,5 milhões / MW, ambos abaixo das médias do setor.

The next step was to estimate the value of CEB-D. In this case, given the privatization context, we worked with two scenarios:

Scenario 1 assumed a successful privatization process. In this case, based on the sector's privatization history, we estimated that the company could be valued at over R$1.0 billion. Given CEB-D's unique characteristics (mentioned above), there was room for positive surprises if multiple bidders participated in the auction.

Scenario 2 considered a scenario without privatization. In this case, given that the company was unable to meet ANEEL's financial targets, the concession would likely be declared extinct and CEBD would cease to exist. Considering the company's liabilities and the costs of closing the transaction, we estimate that, in this scenario, CEB-D would have a negative value of R$$ 300 million.

There was also the possibility of the company continuing to operate the concession, which would be more advantageous (despite CEB-D being in deficit), but we considered this scenario unlikely and ruled it out for purposes of estimating the company's value.

Considering that the holding company costs and the value of CEB-Gás (a small subsidiary) were negligible, the company's value resided mostly in the sum of CEB-D and the power generation companies, which we estimate at R$ 1.7-1.8 billion in scenario 1 and R$ 300-400 million in scenario 2.

These amounts compared to a market value of R$700 million at the time. In other words, in scenario 1 (privatization), there was a potential gain of R$140-160 million, and in scenario 2 (remaining state-owned), there was a potential loss of R$40-60 million. Clearly, the successful privatization of the company was crucial to the investment's success. We then set out to analyze the likelihood of privatizing CEB-D.

Estimates of this nature are always uncertain in Brazil, considering the various participants and political leanings involved in such processes, but some factors gave us confidence that the chances of privatizing CEB-D were high:

There was a successful history of 7 recent privatizations of regional distributors like CEB, meaning we were not treading an unknown path.

The Federal District government and CEB itself were keen on privatization, both because CEB-D was at risk of losing its concession and because of the more liberal bias of the company's board of directors, which is working to make it more efficient. This was evidenced by the steps the company had already taken toward privatization.

Aneel, the sector's regulatory agency, also welcomed the process, as it was a way to improve the quality of energy distribution in the region.

The main opponents of the process were the company's own employees, organized as unions, and politicians who supported them. Thus, we looked at the history of other privatizations to understand what kinds of threats such opposition might generate, but none of these processes had been blocked by union opposition.

Furthermore, at the time of the analysis, the Supreme Federal Court (STF) had recently ruled that the privatization of subsidiaries of state-owned companies did not require legislative approval. The decision had been made in the context of the privatizations of Petrobras and Eletrobras subsidiaries, but it also applied to CEB.

Finally, private companies were highly interested in the asset. There were at least six private companies in Brazil interested in acquiring state-owned energy distributors, and considering the asset's quality, there was no reason why many of these companies wouldn't be interested in CEB-D.

In our estimates, the probability of privatization should be greater than 25% for the investment to have a positive expected value, and considering the points above, it seemed to us that the odds were much higher than 25%. We therefore decided to make the investment.

Given that the position presented a significant potential loss (40-60%), we sought to control the risk by sizing the position. We started with a small investment and, as the privatization process progressed and the likelihood of success increased, we increased the initial position until reaching a level of 10% of the fund invested in CEB.

In summary: with a 10% position and considering our scenarios, we could lose 6% or gain 16% of the fund's total value, with the positive scenario being more likely than the negative. This asymmetry in the risk-return relationship is what led us to the decision to make this investment.

Current scenario

Even after the privatization of CEB-D (which should be completed by March 2021), we still believe that CEB remains an excellent investment opportunity and we maintain it in Arcádia's portfolio.

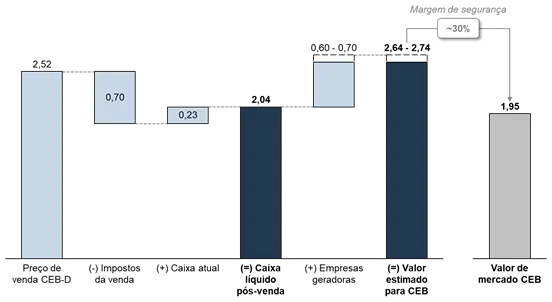

With CEB-D privatized for the value of R$ 2.515 billion, we estimate that the company will pay around R$ 700 million in taxes and, added to the existing cash of R$ 225 million, the company will have a net cash position of R$ 2.04 billion, while its market value is R$ 1.95 billion.3 – that is, the company’s cash alone is worth more than its current value on the stock market!

In this calculation, we haven't even taken into account the generators, which, as we've seen, have an excellent cash generation profile. With the valuation of the R$ 600-700 million mentioned above, we arrive at a fair value for the company of approximately R$ 2.7 billion. Compared to the market price, there is a margin of safety close to R% in the investment, quite high given that a large part of the valuation It's made up of cash, and it appears that a good portion will be distributed as dividends. It seems to us that the company is still cheap.

Chart 4 – Estimated composition of CEB’s value (in R$1.4 billion)

CEB is an atypical company in our portfolio. Typically, we like to invest in high-quality companies, leaders in their sectors, and with high profitability. Because CEB is a state-owned company, it doesn't meet all the qualitative characteristics we envision.

That doesn't mean it's no longer a great investment. In the stock market, it's possible to have excellent returns on average companies, and large losses on excellent ones. It all depends on the price paid for the asset. For us, buying cheap is a great risk management method.

“Investment success doesn't come from buying good things, but rather from buying things well.” – Howard Marks

Arctic Asset News

Temos algumas novidades para 2021. A primeira é que o Ivan Barboza, um dos sócios fundadores do Ártica deixou a prática de M&A para se dedicar exclusivamente à gestora da empresa. Além da vinda dele, nós reforçamos nosso time de análise, e agora estamos com uma equipe de 5 pessoas no time de investimentos. Outra mudança é que, para facilitar nossa comunicação, decidimos unificar a identidade da nossa empresa em torno de uma única marca: Ártica. Com isso, nosso fundo Arcádia FIA irá passar a se chamar Ártica Long Term FIA, unificando a nossa marca Ártica com a nossa filosofia de investimentos.

1 Circuit breaker is a mechanism used to stop trading when the market experiences a sharp decline.

2 The concessions for these plants are held by companies with varying degrees of CEB's shareholding. The 200 MW figure presented represents only CEB's proportional shareholding in each of these plants.

3 On 12/31/2020