Why have private pension?

Dear investors,

Historically, how to sustain oneself in old age was a private matter. People lived off savings accumulated over their lifetime or relied on their children’s support when they could no longer work. The first broad-coverage public pension system was created in Germany in 1889, under the government of Otto von Bismarck, guaranteeing retirement benefits for workers over the age of 70 (later reduced to 65, in 1916).

In the early 20th century, several countries followed the German example and created their own public pension programs. Brazil took its first step in 1923 with the Eloy Chaves Law, which created a fund called the Caixa de Aposentadoria e Pensões (CAP) for employees of railway companies. This structure was soon replicated across various other professional categories, and the number of CAPs multiplied, each administered by an employing company and operating under the principle that resources accumulated through contributions could be used exclusively for the payment of benefits.

In the 1930s, under the government of Getúlio Vargas, the CAPs of companies within the same professional category were consolidated into Institutos de Aposentadoria e Pensões (IAPs), and the government became part of the arrangement, participating in the administration of the IAPs and sometimes contributing to the fund as a way to subsidize certain professional categories. In 1966, the IAPs were unified into a single entity called the Instituto Nacional de Previdência Social (INPS), the direct predecessor of today’s Instituto Nacional de Seguridade Social (INSS). When the government began to participate in pension management through the IAPs, the principle that pension fund resources could be used exclusively for the payment of benefits was abandoned. That was the seed of the pension problems that persist to this day.

The Origins of the Pension Deficit

The logic of a pension fund should be quite simple. Workers invest monthly into the fund, those contributions are invested over time, and the wealth accumulated in this way is used to pay retirement benefits. A reasonable rule is that the benefit be proportional to the years of contribution, except in exceptional cases resulting in premature death or disability. In a very large group of people, there will be those who receive more and those who receive less than what their own contributions would yield, but since the factors that determine who falls into each case are practically random, the standardization of benefits is simply a mechanism for sharing and spreading life’s risks.

A pension system created with these rules would have contributions far exceeding benefits paid for many years, since those who retired shortly after the system’s creation contributed for a short time and will receive little, while those who joined the system when young will have decades of contributions ahead of them before receiving their retirement. This wealth accumulation phase would only end when the youngest generation of contributors reached retirement age. If new contributors were to stop joining the system, it would not be a problem. The pension fund should have sufficient resources to pay even the last generation of retirees without depending on new contributions.

That was not the story of our pension system, due to a public-sector maxim: the government always finds a way to use resources it has access to. The Vargas government itself, which created the IAPs, interpreted that the purpose of these institutes was to defend the long-term interests of their beneficiaries, which was not limited solely to the payment of retirement benefits but also involved promoting economic and social development. As a result, pension resources began to be used to finance infrastructure projects and other politically motivated investments.

The crucial question — how to finance the payment of retirement benefits — was addressed based on the logic that pension funds would never run out, so the contributions of new generations would be sufficient to sustain the benefits of retirees, without the originally accumulated wealth needing to be fully preserved. Put simply, the State decided it could appropriate the contributions made by parents throughout their working lives and use the contributions made by children to pay for their parents’ retirement.

A series of assumptions are involved in judging how much would need to be kept in pension funds to sustain retiree payments in this way. For example, the demographic growth rate (how many children will support their parents’ retirement), the retirement age, and average life expectancy (how many years parents will survive in retirement). Since adopting optimistic assumptions allowed the State to make more resources available for its own purposes, that is exactly what was done.

The problem is not exclusively Brazilian. Many countries, including several developed ones, adopted the same principle that pension fund resources could be used for other purposes and today face pension deficits driven by two major secular trends: rising life expectancy and declining average birth rates. In other words, fewer and fewer active workers are required to make contributions to finance the benefits of more and more retirees, already knowing that when they retire, they will very likely receive less than they contributed.

The most correct way to fix the problem would be for the State itself to cover the pension deficit and honor the terms in place when contributions were made, but anything involving the government gains complexity. The current government is not the same one that decided to appropriate pension resources, and there are no surplus funds available to make the necessary compensation. Other public spending would need to be cut or taxes raised. There is no elegant way out.

The path taken by virtually all countries with problems of this nature has been to reform the rules of the pension system. Brazil did this in 2019, with changes that increased the required contribution period and reduced the value of some benefits. It was a mitigating measure that does not solve the problem in the long run. The pension deficit still exists and continues to grow.

The solution is private pensions

As unjust as the situation is of being required to contribute to a pension system that carries a high risk of not paying its benefits in full in the future, there is no escape for most Brazilians. The contribution to the INSS is compulsorily deducted at source, taken directly from the monthly payments made to those who work under the CLT employment regime. The alternative is to save something beyond the compulsory contributions in order to build wealth that remains under one’s own control and guarantees sufficient resources for a comfortable retirement.

Acknowledging the inadequacy of the public pension system, the Brazilian government created in 2001 the Regime de Previdência Complementar (RPC) — a voluntary supplementary pension system that grants certain tax benefits to those who create private pension plans. The available options are the well-known PGBL and VGBL, both offering the choice between a progressive or regressive tax regime. Details on each type of plan are widely available, so we will focus only on the most important characteristics of the PGBL and VGBL and on the regressive tax regime, which will be the most advantageous for the vast majority of our investors.

PGBL

The benefit of the PGBL is that you can invest up to 12% of your annual taxable income in pension funds, and this amount will be exempt from the income tax (IR) that would otherwise be charged in the year. In return, the entire balance invested in these funds will be subject to income tax at the time of withdrawal. There are two relevant advantages to this arrangement.

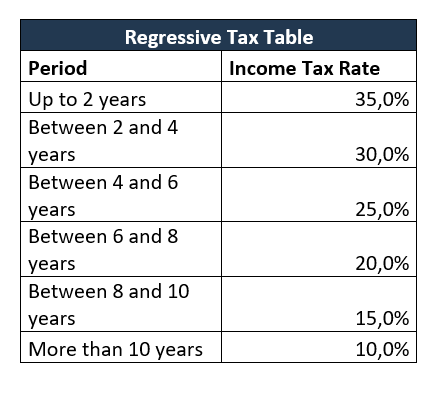

The first is that the income tax rate can be reduced from 27.5% to as low as 10.0% under the regressive tax regime, as the rate decreases over the period the funds remain in the pension plan, as shown in the table below:

From the fourth year of investment onward, the rate is already advantageous, and considering the intention is to save for retirement, reaching the 10 years required to benefit from the maximum reduction is not difficult.

The second advantage is that, even if the income tax rate were the same, deferring the tax payment from now until the moment of withdrawal (tax deferral) produces a meaningful difference in returns over long periods. Over 20 years, an investment with deferred income tax would be worth approximately ~17% more than an investment with the same return but with annual income tax payments. This is the same benefit that exists for investments in equity funds.

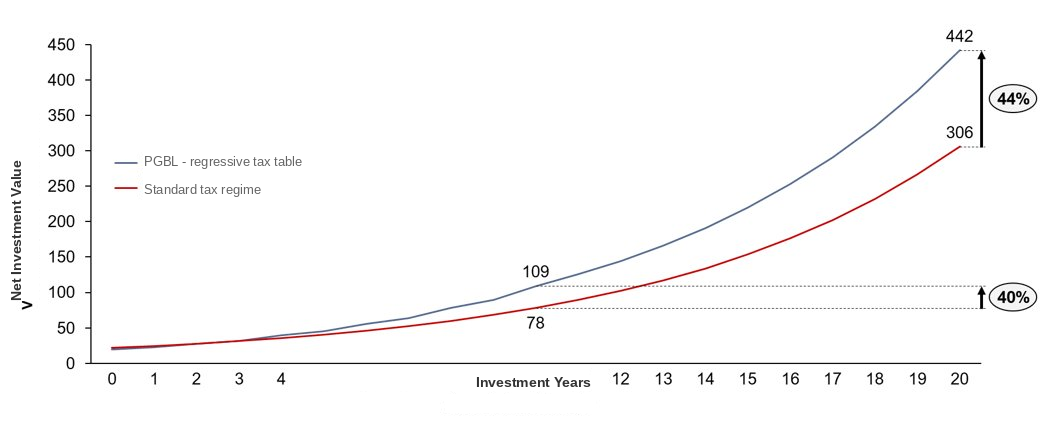

Combining the rate reduction and the tax deferral, the difference is enormous. We simulated the case of someone earning BRL 250,000 per year who invests BRL 30,000 (12% of their annual salary) in a pension fund with an annual return of 15%. If the investment is redeemed after 20 years, its net value will be 44% higher than an equivalent investment made without the PGBL tax benefit.

PGBL investment simulation with regressive tax table

In short, for those who work under the CLT and have income in the upper bracket of the income tax table, it is highly advantageous to invest in a PGBL under the regressive tax regime. If possible, up to the limit of 12% of annual income and for a period of more than 10 years.

VGBL

The tax benefit of the VGBL is only the rate reduction under the regressive tax regime, from the 15% applicable to capital gains down to 10% from the 10th year of investment onward. However, the VGBL has a useful feature for estate planning: in the event of the account holder’s death, the invested amount can be transferred to a designated beneficiary without going through the probate process and without the ITCMD tax being charged (between 2% and 8% of the estate, depending on the state of residence), since the VGBL functions in the same way as a life insurance policy.

There are two typical use cases for this VGBL mechanism. The first is when the probate process is expected to be lengthy and there are heirs who cannot support themselves independently. The VGBL is a way to quickly transfer a portion of the estate to those heirs. The second case is when there is a desire to distribute the inheritance differently from what the law provides, given that the VGBL is not included in the estate to be divided among the heirs. In fact, any person can be designated as a beneficiary of a VGBL plan, whether they are an heir or not.

What Is the Best Strategy for Investing in a Pension Plan

As the Chinese proverb goes, “the best time to plant a tree was 20 years ago. The second best time is now.” The earlier one starts saving for retirement, the lower the amount that needs to be invested, since the effect of compound interest grows exponentially over time. So, anyone who does not yet have an investment strategy for retirement should start thinking about one as soon as possible.

There are two basic principles that follow from the nature of these investments: you should invest with the very long term in mind, and there is no need for liquidity, since the idea is to only redeem these resources upon retirement. Thus, the goal is to seek the best possible rate of return over decades, while maintaining a healthy dose of prudence. Price volatility unrelated to the fundamentals of the invested assets matters little, as over very long periods these market fluctuations tend to cancel each other out and returns converge toward how much the fundamentals actually evolved. This mindset makes sense whenever the invested resources will not be needed in the short term. The sound principles of wealth building are the same regardless of the ultimate intended use of the accumulated capital.

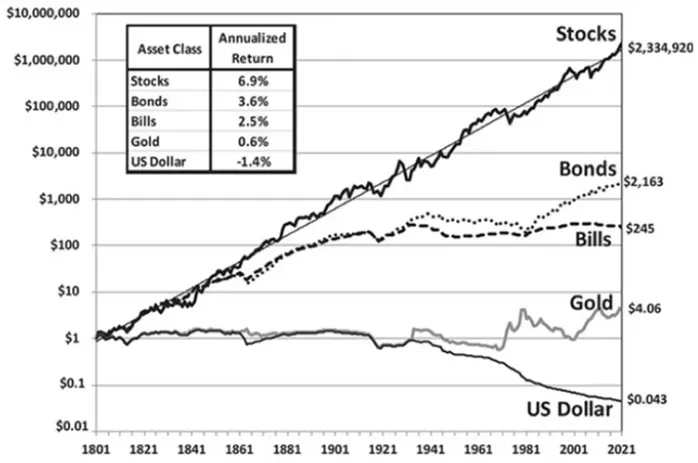

This is the investment philosophy we adopt in our funds, and we choose to invest in equities because it is the asset class with the highest returns over long periods — a point well illustrated by Jeremy Siegel, professor at the University of Pennsylvania (Wharton School), who gathered investment data from the United States over 220 years and compiled them in the chart below.

Return comparison between equities, fixed income, gold and the dollar

Source: Stocks for the long run, 6th edition (Jeremy J. Siegel)

Some argue that this conclusion does not apply to Brazil, since the Ibovespa has delivered returns very similar to the CDI over recent decades, but with far greater volatility. However, our market offers many opportunities for those willing to select the best companies on the exchange and invest in them during times of stress, when prices fall sharply. We have been doing this for more than 11 years, and the average return we have achieved since the founding of the Ártica Long Term FIA to date has been 29.2% per year, equivalent to 314% of the CDI’s return over the same period.

Launch of Ártica Previdência

Although our philosophy is well suited for pension investments, it was not previously possible to invest with us through the PGBL or VGBL, as these plans require that investments be made exclusively in funds specifically created to receive pension assets. However, we have news.

We have just launched the Ártica Previdência FIM, which began operations last Friday (11/29). In it, we will follow the same investment strategy as our other funds (Ártica Long Term FIA and Ártica Polaris FIA), with two adaptations: the first is that pension funds cannot hold more than 15% of the portfolio in a single stock, so the Ártica Previdência will be slightly more diversified; the second is that the new fund will not be required to keep at least 67% of its capital permanently invested in equities, a requirement imposed on equity funds to be exempt from the come-cotas tax. In other words, we will have flexibility to invest along with the most advantageous tax regime in Brazil: an income tax rate on capital gains of up to 10% with no come-cotas.

The Ártica Previdência FIM is already available to BTG clients, alongside the Ártica Long Term and the Ártica Polaris. Our funds are not publicly listed on the product platform, so the first investment must be made by requesting it through your BTG account advisor. After the first investment, the funds will appear in the bank’s app and additional contributions can be made by you directly. Should you have any questions, we are available to help via WhatsApp. (11) 97891-7619.