Equities or Fixed Income: The Brazilian Investor’s Dilemma

Dear investors,

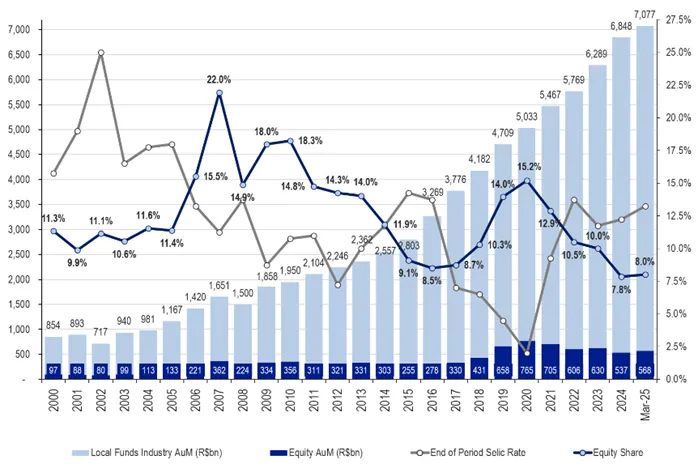

The Brazilian stock market has been losing ground in the portfolios of local investment funds since 2021. Today, 8.0% of total capital managed by funds is allocated to equities — very close to its lowest level in 25 years (7.8% at the end of December 2024) and well below the average of 12.7%.

Local Fund Allocations to Equities (R$ billions)

Source: BTG Pactual – Brazil: Follow the money, May 13th 2025.

The main reasons for the low allocation appear in the press almost daily: concern over the fiscal deficit, the Brazilian government’s rising debt, and sky-high interest rates — which fuel the Brazilian investor’s current mantra: why take risk in the stock market given this backdrop, when the CDI rate is so high?

The mantra is reinforced by the recent track record: from January 2021 to May 2025, the Ibovespa returned ~17% while the CDI returned ~55%. Combined with the fact that equity investment decisions are always more complex than simply investing in floating-rate bonds and watching one’s wealth compound steadily, it is fair to question why investing in the Brazilian stock market would make sense right now. Meanwhile, Ártica’s funds are nearly fully allocated to equities — so it is only natural that we have an answer.

Our first point is that stock market investments are not destined to the IBOV's return. There is much more room to obtain additional returns through asset selection on the stock market than in fixed income. Investors in Ártica Long Term FIA returned 74% (1.35x the CDI) in the period in question, even with the tide against stocks. The broader reasons to invest in stocks now are that companies are structurally biased to yield more than credit investments, and the best way to seek good returns is to buy when there is low capital allocation in the stock market, as this is precisely when capital is undervalued. Let's explore these points.

Average Business Returns Must Outpace the CDI

Our first point is that equity investments are not fated to deliver the Ibovespa’s return. There is far more room to generate additional return through asset selection in equities than in fixed income. Ártica Long Term FIA investors earned a return of 74% (1.35x the CDI) over the period in question, even against a headwind for stocks. The broader reasons to invest in equities now are that businesses are structurally biased to outperform credit investments, and that the best time to seek good returns is when capital allocation to the stock market is low — precisely when it tends to be undervalued. Let us explore these points.

The original sources of economic value are natural resources and human time invested in something with immediate utility (services) or future utility (consumable products, capital goods, and technology). Since there are infinite ways to organize the use of both — and centralized attempts to do so have been famously unsuccessful — the main advantage of the modern capitalist system is to create incentives for decentralized, continuous pursuit of the best possible organization through a self-calibrating price mechanism: the well-known supply-and-demand price-discovery process. The classic example of how productive activity organizes itself around this price mechanism is that any good will begin to be produced in greater quantities shortly after demand for it increases, because excess demand over available supply causes prices to rise, which incentivizes the creation of additional supply capacity until equilibrium is restored. The same logic works in reverse, and capital allocation optimization follows the same principle, viewed from a slightly different angle: when demand for something rises, higher prices cause the capital allocated to create additional supply capacity to expect higher returns, incentivizing more capital allocation toward this purpose until supply and demand rebalance and the return premium disappears.

Fundamentally, credit need not exist to solve the capital allocation problem. All investment could be made directly into businesses, and each investor would directly bear the risks of the economic activities they chose to support by making their capital available. The benefit brought by the credit mechanism is providing greater capital mobility in the economy. Rather than deeply understanding the expected return of a sector and committing to invest in it indefinitely — since selling stakes in a private company is a complex process — it is possible to outsource much of the problem to someone who already understands the sector demanding capital and has an allocation plan in mind. The capital owner makes a loan under far simpler terms to analyze: a predetermined rate of return, a payment schedule, and a collateral structure to reinforce the borrower’s commitment.

The benefit to the lender is clear. For the entrepreneur, taking on loans only makes sense if the agreed interest rate is considerably lower than the expected return on the use of capital, since the risk falls disproportionately on their side. Naturally, in many cases borrowers miscalculate and end up worse off than their creditors — but if this negative outcome becomes too common, entrepreneurs will borrow less capital, credit investment opportunities will become scarcer than the capital available to lend, and lenders will have to reduce the rates they demand to stimulate interest in new credit transactions. In other words, interest rates also follow the logic of prices. The spread between the average return on equity investments and the average rate on loans is necessary to keep the credit system functional, just as profit on the sale of a product is necessary to ensure its continued supply.

This logic does not necessarily hold at every moment. Just as supply-demand imbalances can cause significant price swings, periods of poor business results due to unpredictable factors can frustrate entrepreneurs’ expectations and leave lenders better off. But in the long run, it is unsustainable for credit investment returns to remain persistently higher than business returns — because that would mean entrepreneurs, the true creators of real economic value, would chronically accept earning less than passive rentiers, even when they could simply step back from running businesses and become creditors themselves.

A brief aside: the average interest rate on business loans is always higher than the CDI, which applies to ultra-short-term interbank credit operations and carries very low risk. It is therefore expected that the average return on businesses in general will be considerably above the CDI over long periods.

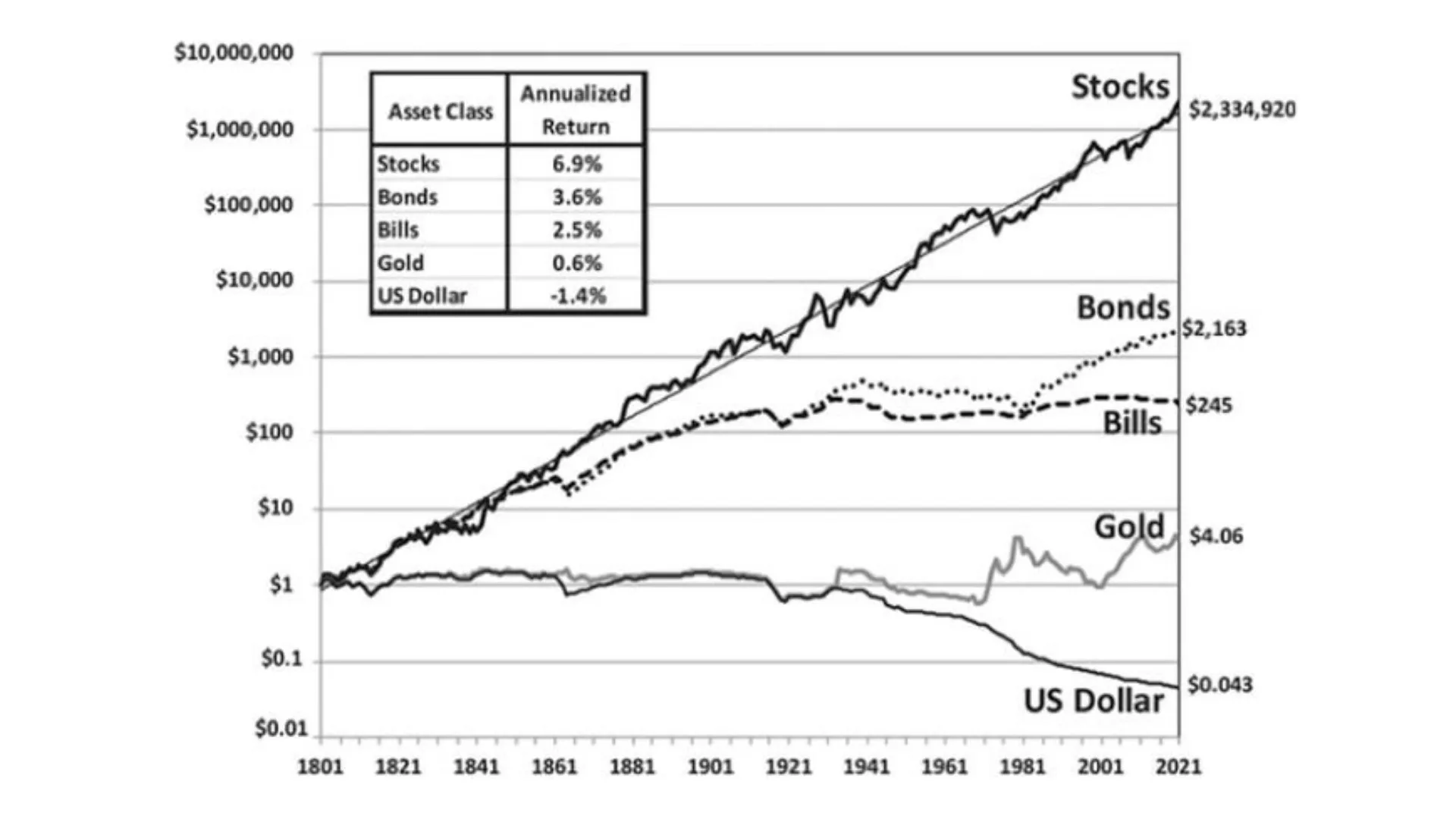

If the theoretical argument is insufficient, the most comprehensive empirical evidence comes from Jeremy Siegel’s long-run study, which analyzed fixed income and equity returns in the American market over more than 200 years and summarized the results in this famous chart, originally published in his book Stocks for the Long Run.

Note: real returns, above inflation

There is also anecdotal evidence: have you ever heard of great fortunes built through investments in bank CDBs, real estate credit notes, and the like?

When Is the Right Time to Buy?

Despite the conclusion that owning equity in businesses tends to be more profitable than being a creditor over the long term, the equity market is notably cyclical and the purchase price of shares has a significant impact on returns. The best way to gain confidence that a purchase price is attractive for investment is a well-known process: (i) qualitatively analyze how the company’s business works; (ii) estimate the cash flow generated by the business over the coming years; (iii) calculate the stock’s intrinsic value by discounting the estimated cash flow at your target rate of return; and (iv) only buy when the price is considerably below your intrinsic value estimate — the tried-and-true margin of safety. This is not highly complex work, but it requires a certain investment of time. However, there are simpler, quicker ways to check whether there are signs that it may be a good time to seek undervalued stocks.

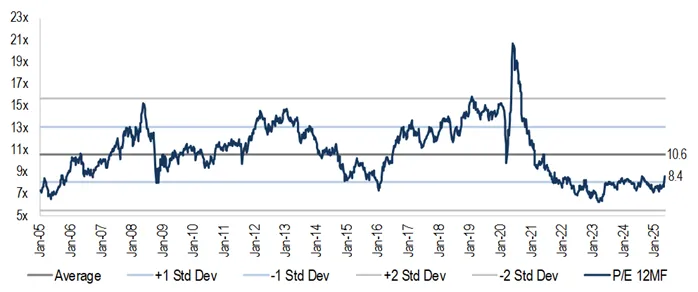

One such way is to monitor the evolution of the market’s average valuation multiples. Though simplistic, this indicator provides a general sense of how current prices compare to their “normal” level. Several investment banks regularly publish this index, which today stands ~21% below its 20-year average.

Average Price/Earnings Multiple* in the Brazilian Stock Market

*Considers estimated earnings for the next 12 months

Source: BTG Pactual – Brazil Strategy Monitor, May 23rd 2025

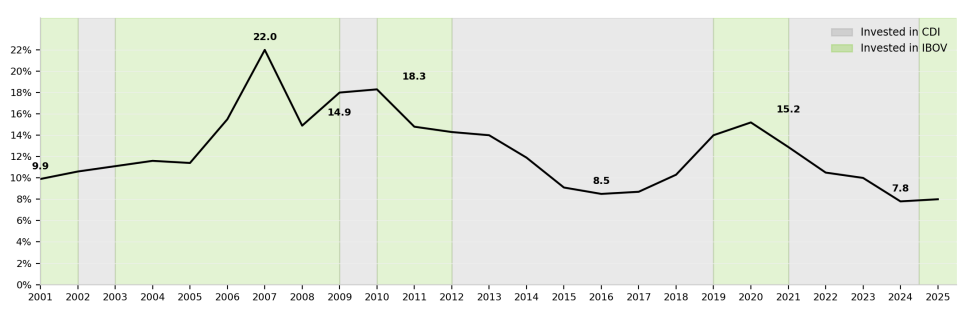

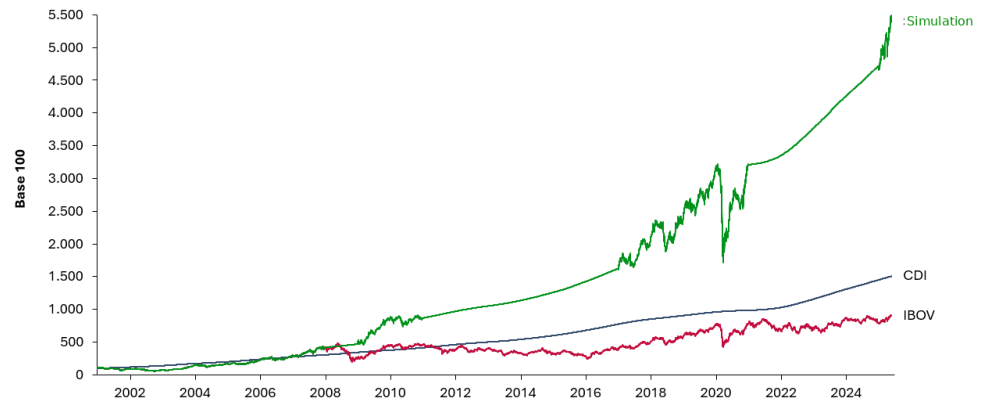

Another approach is the one we mentioned at the outset: monitoring the level of domestic fund allocations to equities — since when it is low, it tends to be a good time to buy. This assertion is not immediately obvious, given that most of the capital invested in the Brazilian fund industry comes from professional investors, implying that they would be making the same mistake as all other categories (foreign investors and retail investors). To test whether the assertion holds, let us simulate the return of a simple strategy: invest in the Ibovespa when domestic fund allocations to equities are at minimum levels (and beginning to rise), and in the CDI when they are at maximum levels (and beginning to fall). The investment periods in each index and the returns achieved under this simulated strategy are illustrated below.

IBOV vs. CDI Investment Based on Local Fund Equity Allocations

Simulated Strategy Return

The interpretation of these facts that seems most fair to us is that local investors, like all others, behave pro-cyclically: as the stock market generates good returns, they gain confidence and increase their equity allocation; when stocks begin to fall, they get frustrated and migrate to fixed income. This is what generates the pendulum behavior of markets, which — even as a completely well-known phenomenon — inevitably keeps repeating.

The trap is largely psychological. Most people, professional or not, feel insecure in the face of uncertainty and seek reassurance in the behavior of those around them. This is a good strategy in many areas of life. If you see a crowd running, it is advisable to run in the same direction and only ask why afterward. In investing, it is advisable to develop your own analyses and draw your own conclusions independently of what the majority thinks. The conviction to act against the crowd comes from analytical work executed with diligence — and a touch of faith in the ancient Latin proverb: fortis fortuna adiuvat — fortune favors the bold!