The New Cold War

Dear investors,

When we read about history, each episode appears to have been clearly triggered by a notable event. The Second World War began on September 1, 1939, when Nazi Germany invaded Poland. The Cold War between the United States and the Soviet Union began on March 12, 1947, with the announcement of the Truman Doctrine. However, this clarity is largely the result of the didactic organization historians impose with the benefit of hindsight. The boundaries of historical episodes are far more blurred when experienced in the present.

The rivalry between the United States and China, now quite evident, has been intensifying for more than a decade. Some argue that we are heading toward a new world war, while others believe the conflict will remain contained due to the deep economic interdependence that still binds the two nations. It is difficult to predict how far this will go, but it is already clear that the dispute has triggered profound shifts in global geopolitics. We will share our reflections on these developments and how they may shape the future.

History of the Rivalry

In the 2000s, China was not seen as a major concern for the United States government. In fact, the United States played a leading role in supporting China’s accession to the World Trade Organization in December 2001. At the time, the prevailing rationale was that integrating China into the global economy would generate significant cost advantages for American companies by leveraging inexpensive Chinese labor. Moreover, it was believed that China’s economic development—anchored in global trade—would gradually lead it to adopt Western practices and converge toward a democratic political system. That, however, is not what unfolded in the decades that followed.

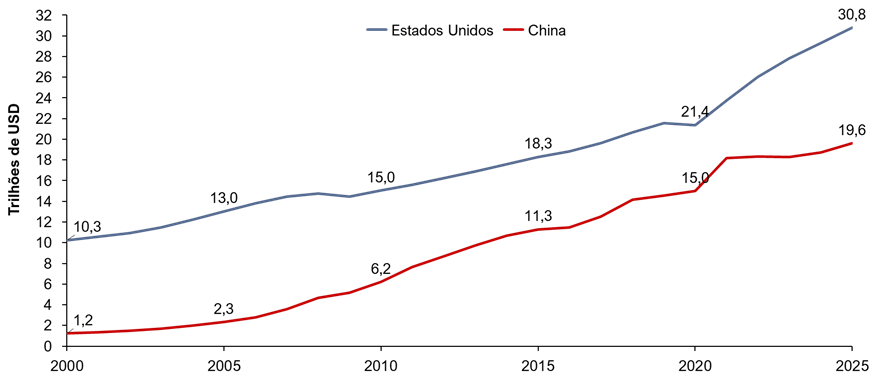

China’s economic development was faster and far more substantial than anticipated. Between 2000 and 2025, China’s GDP expanded sixteenfold, while U.S. GDP grew threefold. As a result, China’s economy increased from representing 12% of the U.S. economy to 64% of its size.

Evolution of U.S. and China GDP

Fonte: Federal Reserve Bank e World Bank

The expectation that integrating China into global trade would generate economic benefits for the West did materialize. The United States, along with several other countries, outsourced a significant portion of their manufacturing to China and experienced meaningful improvements in living standards, driven by the decline in the cost of consumer goods available to them. However, the assumption that China’s economic development would lead the country toward democracy and political alignment with the West did not come to pass.

China has maintained a culture, political system, and economic dynamics that differ substantially from the models idealized by the West. Its worldview and development strategy do not necessarily align with the global order architected by Western powers and led by the United States. With a population of 1.4 billion people and its position as the world’s second-largest economy, it is inevitable that the United States views China as a challenge to its supremacy.

Paradigm Shift

Following the collapse of the Soviet Union in 1991, the world entered an era of relative peace among major powers, with most countries operating under diplomatic arrangements shaped by the Western bloc after the world wars and guided by a broad principle of cooperation aimed at global development and prosperity.

In democratic political systems, and in the absence of imminent major geopolitical threats, governments increasingly prioritized their populations’ demand for a higher standard of living—strongly correlated with economic efficiency. We saw Germany, an adversary of Russia in both the First and Second World Wars, deepen its dependence on Russian gas in order to lower energy costs and pursue environmental targets. The United States warned of the geopolitical risks and exerted diplomatic pressure on Germany in an attempt to halt the move. Even so, economic rationale prevailed. Voters tend to prefer lower living costs over reduced geopolitical risk—and political incentives follow electoral preferences. This episode captures the prevailing mindset of the time, when economic optimization stood as the ultimate objective of nations.

In recent years, two major developments have forced the world to reassess its hierarchy of priorities. The first was the outbreak of the war between Russia and Ukraine, which heightened fears within the European Union of Russian expansionism and intensified broader Western frustration over Russia’s failure to adhere to what they consider established diplomatic norms. The second was Trump’s return to the U.S. presidency and the implementation of the “America First” policy, which made the conflict with China more explicit and marked a departure from the longstanding principle that the United States bore responsibility for protecting the broader Western alliance, even in the absence of clear reciprocity.

Suddenly, national security began to outweigh economic efficiency as the dominant priority. Germany stopped purchasing Russian gas—at least directly—in order to avoid generating revenues for Russia and financing a war machine advancing toward the European Union. The United States, in turn, imposed restrictions on the sale of advanced technologies to China. American companies may earn less as a result, but they also reduce their contribution to the advancement of a country perceived as a potential new global leader.

This is not merely a shift in the strategy of politicians and diplomats. Populations themselves have become increasingly aware of geopolitical tensions and have reacted accordingly. In one episode shortly after the invasion of Ukraine, British dockworkers refused to unload Russian oil shipments, even though there were no legal obligations requiring them to do so.

Prioritizing national security over economic efficiency may seem unusual to current generations, but it has been the prevailing mindset throughout most of human history. During the world wars, a French citizen would never have purchased Nazi products simply because they were cheaper than those produced in France. The past few decades were an exception—one that now appears to be coming to an end.

What We Expect for the Future

The pursuit of national security will inevitably lead countries to reduce their economic dependence on politically misaligned nations, either by reshoring segments of their supply chains or by developing alternative suppliers in countries perceived as non-threatening. This dynamic is likely to constrain global trade flows and, as a consequence, result in slower economic growth and higher inflation. As economic efficiency ceases to be the sole guiding criterion in business decisions, production costs tend to rise, putting upward pressure on prices.

There is a clear tendency for the United States and China to consolidate their spheres of influence over geographically proximate countries, given that geography remains a decisive factor in military strategy. Projecting military power across distant regions is both costly and risky. It requires complex logistical operations and entails greater vulnerabilities than actions conducted near one’s own territory. From this logic emerges the strategic imperative of preventing neighboring countries from falling under the influence of rival powers.

The competition for influence, characteristic of cold wars, may create opportunities for developing countries. One option is to maintain neutrality, preserving the ability to trade with any nation that offers favorable terms, much as Switzerland did even during the world wars. Another possibility is to discreetly auction one’s allegiance, negotiating financial aid, technology transfers, and military protection in exchange for political alignment, as many countries did during the Cold War between the Soviet Union and the United States.

We are also likely to see an intensification of the technological race and increased investment in infrastructure deemed critical in the event of military conflict—a risk that is ever-present and becoming increasingly explicit. This dynamic unfolds regardless of each bloc’s stated intentions. The weaker side fears the power of the stronger and seeks to develop in order to close the gap. As the weaker side advances, the stronger fears being overtaken and accelerates its own development to defend its leadership position. Thus, even if both sides claim purely defensive intentions, competition for economic and military power will persist.

The dynamic we are describing is far from new. Although it hasn't been part of our direct life experiences, history is full of episodes of this nature.

Impact on investments

Given that these geopolitical conflicts can significantly affect the economy, either broadly or within specific sectors, they must now be incorporated into the analysis of investment opportunities.

Traditional fundamentals remain fully valid. We continue to seek investments in companies with durable competitive advantages and high profitability, but we now also assess whether a business may be exposed to potential impacts from economic sanctions and/or tariffs.

The risk is particularly relevant for exporting companies. If their home country becomes subject to sanctions or tariffs, they may lose customers or be forced to reduce prices to offset the additional trade barriers. In such circumstances, competitive advantages alone do not guarantee business resilience. In the case of comprehensive sanctions, a company may lose sales even if it is the sole producer of a product with relatively inelastic demand. For example, Nvidia is prohibited from selling its most advanced chips to China, as the U.S. government has decided to restrict access to cutting-edge technologies that could have military applications.

Companies primarily focused on their domestic markets tend to be more resilient in this environment. They may even benefit if a meaningful portion of their competition comes from imported products. Should their home country impose sanctions or tariffs on other nations, foreign competition declines, allowing domestic players to capitalize on the gap created in the local market.

There may also be indirect effects on an entire national economy if a key sector is targeted. For instance, if Brazilian agricultural exports were disrupted, the broader economy would likely suffer as a result.

Fortunately, Brazil remains far from the epicenter of current geopolitical conflicts, and the likelihood of being severely harmed by sanctions or tariffs is relatively low. We are among the countries that stand to benefit from the search for trade partners that do not pose geopolitical threats. A recent example is the free trade agreement between the European Union and Mercosur, negotiated for decades and now on the verge of entering into force, which advanced largely due to the European Union’s desire to reduce its dependence on the United States.

At present, our portfolio has relatively limited exposure to geopolitical risks. Nevertheless, we believe it is prudent to closely monitor these global geopolitical developments and to exercise an additional degree of caution when assessing opportunities in sectors that may be deemed strategic.