The 1% per Month Trap

Dear investors,

In Brazil, from beginner investors to high-net-worth families, many believe that 1% per month is a good return target and adopt a strategy of seeking this return with the lowest possible risk. When interest rates are above 12% per year, fixed income is the preferred asset class for most investors, who see no reason to take on greater risks in search of extra returns. Once the benchmark rate falls below 1% per month, they begin exploring alternative asset classes and allocate part of their portfolio to investments with sufficient return potential to, combined with their fixed income holdings, pursue the coveted 1% per month again.

This strategy of using a fixed return rate as a reference for increasing or decreasing fixed income allocation is so common and intuitive that few question its rationality. However, that is precisely what we will do here. We will analyze whether it truly represents a sound rule of thumb for investing, whether there is something more efficient, and present a more generic conceptual model that better frames the relationship between return and risk in investments.

Where Does the 1% per Month Benchmark Come From?

Over the past 20 years, the average SELIC rate — the benchmark return for Brazilian fixed income securities — has been close to 11% per year. This gave rise to the general belief that 1% per month is the return typically achievable by investing in fixed income in Brazil. However, the chart below already illustrates the problem with assuming this rate as a fixed return target.

Historical SELIC Rate in Brazil

Source: BACEN

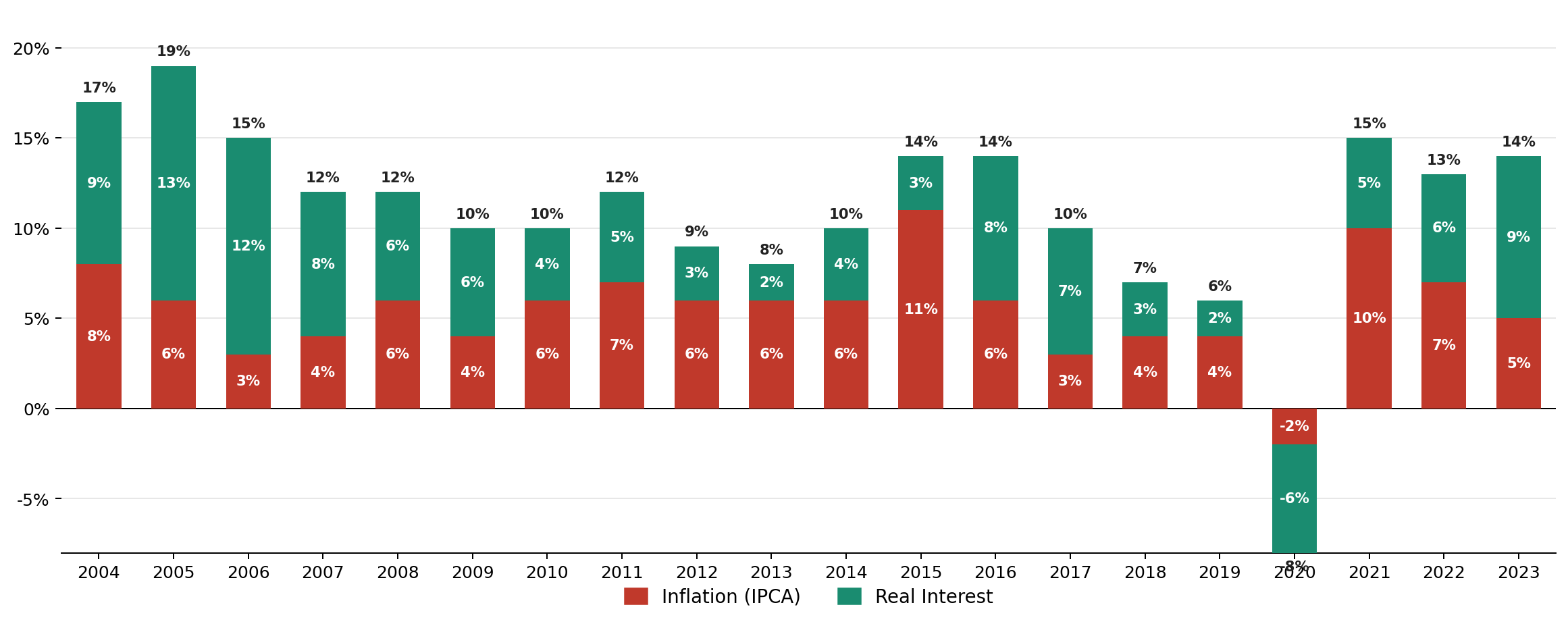

The rate has fluctuated significantly over the period and has recently been at lower levels. Furthermore, the SELIC is a nominal return rate, which includes a substantial inflation component. The typical assumption is that roughly half of the rate reflects inflation and the other half reflects real returns, but when decomposing historical rates into these two components, it becomes clear how crude this assumption actually is. Real returns — what truly matters for investments — are even more volatile than the SELIC.

SELIC history broken down into inflation and real interest rates

Source: BACEN, IBGE

The Best Rule of Thumb for the Brazilian Investor

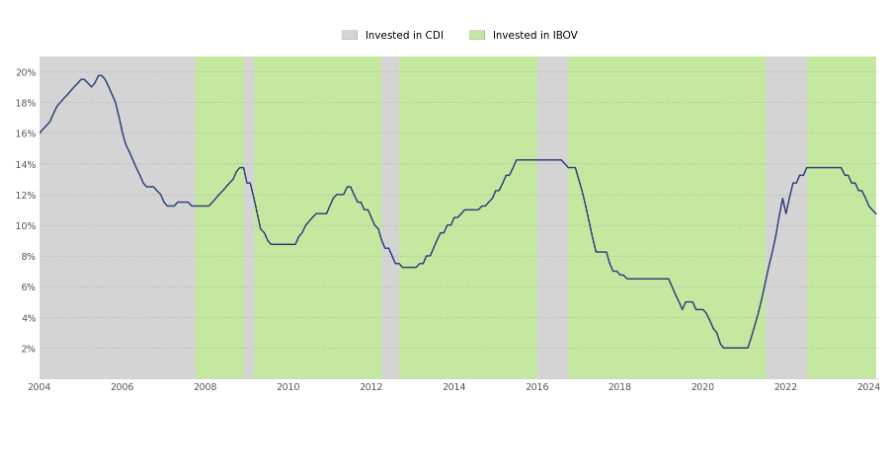

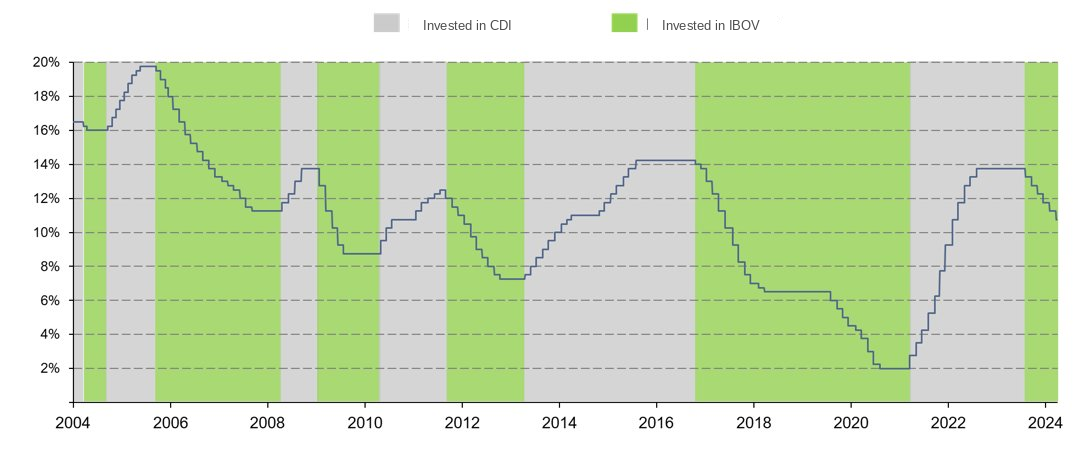

Even though there is meaningful variation around the 12% average return, what matters is evaluating whether the intuitive rule of investing in fixed income when interest rates are above a certain threshold — and in equities when below it — represents a sound strategy. To test this, we will simulate the return of a portfolio following a simplified rule: when the SELIC target is at or above 12%, all investment is allocated to fixed income; when below 12%, all capital is allocated to variable income. We use the typical benchmarks as references: benchmarks CDI for fixed income and IBOVESPA for equities. The chart below shows how the allocation would have been structured over the period from January 2004 to March 2024, just over 20 years.

Strategy 1: Fixed Income When Interest Rates ≥ 12% p.a.

With this strategy, an investor would have achieved an average annual return of 11.8% per year, above the returns of both the CDI (10.7% p.a.) and the IBOVESPA (9.0% p.a.) in isolation. At first glance, this intuitive, empirical rule does not seem unreasonable. However, there is no clear rationale for using a fixed nominal rate as the reference for allocation decisions, nor for 12% being the optimal value. In fact, over the period analyzed, the best cut-off would have been 11.4%, yielding a return of 12.5% p.a. Using 10% or 13% as the switching threshold would have produced returns below the CDI. The sensitivity of returns to the exact reference rate used highlights the ad hoc nature of these results and the risk of adopting rules without a sound theoretical basis. For this reason, it is worth seeking a more efficient rule — one that is still simple and practical enough for any investor to follow.

The relationship between interest rates and equities is well understood. The higher the interest rates, the lower stock prices should be, for two main reasons: (i) high interest rates hinder economic growth, and (ii) equity investors require an expected rate of return equivalent to the benchmark rate plus a risk premium that compensates for the additional investment risk. Therefore, even if a company generates exactly the same cash flow regardless of interest rate levels, investors will accept paying a lower price for its shares when rates are high. Accordingly, the most effective strategy would be to invest in equities when interest rates are at their peak and return to fixed income when rates are at their lowest. The problem is that interest rate peaks and troughs are difficult to predict, making this strategy hard to implement in practice.

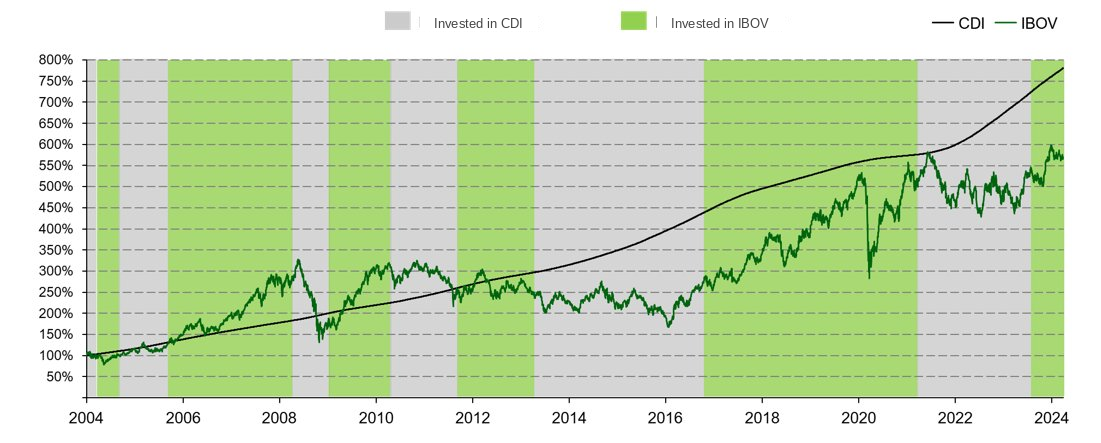

Trends in rising and falling interest rates, however, tend to be less erratic than stock market movements, as they are driven by monetary policy defined by the Central Bank. The exact timing of rate increases or cuts — and the terminal rate they will reach — remains uncertain, but the Central Bank acts in a planned manner and typically signals its intentions so that markets can adjust their expectations. We can therefore adopt a relatively simple strategy that makes more conceptual sense than the first: invest in fixed income when a rate-hiking cycle begins, and shift to equities when rates begin a new downward trajectory. Using the same simplified rules as in the previous simulation, the allocation under this second strategy is shown in the chart below.

Strategy 2: Fixed Income When Rates Rise, Equities When Rates Fall

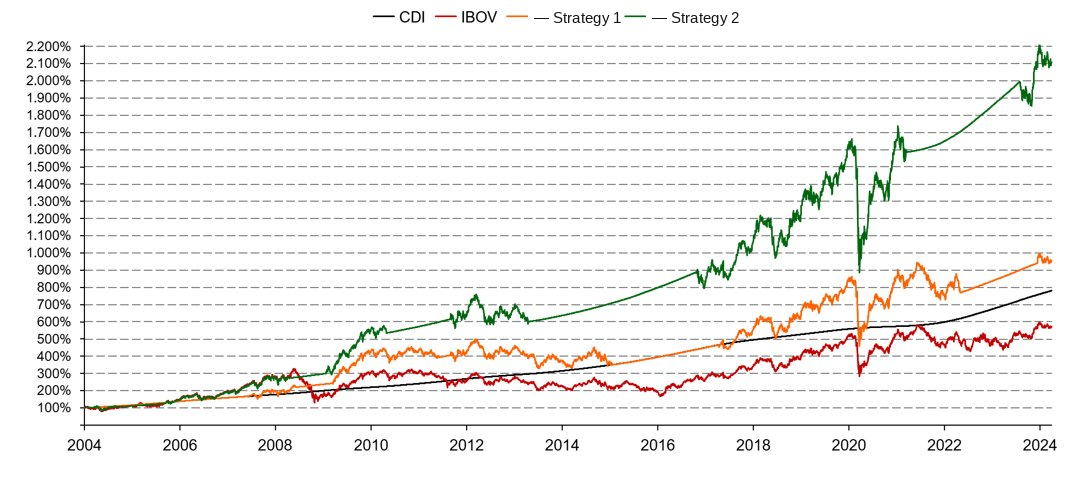

This strategy would have generated an average annual return of 16.3% per year — considerably higher than the allocation based on a fixed interest rate reference. In summary, here are the simulation results:

Return Comparison: Strategies 1 and 2 vs. Benchmarks

We also highlight how investing in equities can generate substantially higher returns than keeping all assets in fixed income — even in this analysis, where we used the IBOVESPA as the equity benchmark. This index does not capture the full potential of equity investing, as it assumes a completely passive strategy with no effort to select the best stocks. One example of the impact that stock selection can make is the Ártica Long Term FIA itself, which achieved an average annual return of 30.5% p.a. (21.6% p.a. above inflation) over nearly 11 years, from June 2013 to March 2024 .

Return Comparison: Ártica Long Term FIA

Now, let us seek a conceptual framework for approaching investment decisions that is generic enough to encompass different risk and return profiles — going beyond our simplistic scenario in which we considered only CDI and IBOVESPA.

How to Think About Return and Risk

When developing an investment strategy, one can approach the question of risk and return in several ways: fix the level of risk and seek the highest possible return, fix the desired return target and seek the lowest possible risk, or fix neither variable and always seek the best risk-return trade-off available in the market. However, it is not immediately clear which approach is best.

A useful starting point that simplifies the problem is recognizing that there is a maximum level of risk that a prudent investor should be willing to take, regardless of the associated return potential. For example, an opportunity offering a 50% chance of multiplying the invested amount by five and a 50% chance of ending up worthless has an extremely favorable risk-return profile — but it would be highly imprudent to allocate one's entire wealth to it and accept the real risk of financial ruin. The first step, therefore, is to determine the maximum level of risk one can (and is willing to) take on. A simple way to think about this is to identify what portion of invested capital is needed to sustain one's lifestyle. That portion should be preserved even under investment stress scenarios.

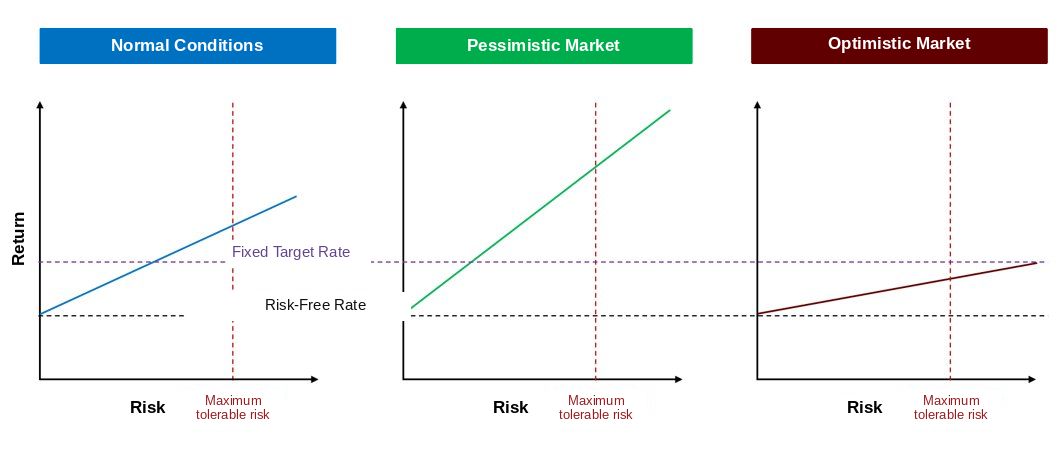

The second consideration is that the relationship between risk and return is not constant over time. There are moments when markets offer attractive returns for those willing to take on more risk, and moments when those additional risks are poorly compensated. Accordingly, fixing a target return rate will always lead to a suboptimal investment strategy. The charts below help to illustrate this reasoning.

Under normal market conditions, it is reasonable to assume that the incremental return offered as investors accept higher levels of risk is adequate. In such an environment, the return target will depend primarily on the level of risk the investor is willing to assume, subject to the maximum tolerable risk. The problem with treating this return target — established under normal conditions — as a fixed rate is that it becomes inadequate at the extremes of economic cycles.

During downturns, when the macro environment is unfavorable, interest rates are high, and market sentiment is pessimistic, most investors avoid riskier asset classes and, as a consequence, the risk premium per unit of risk increases. In this environment, it would be appropriate to seek higher returns, since the same level of risk the investor was willing to accept under normal conditions would now correspond to a higher target return. It may even be advantageous to move closer to the maximum tolerable risk at this point, as it is when taking on additional risk offers the greatest benefits.

During upturns, when the economy is performing well, interest rates are low, and markets become euphoric, investor optimism leads them to accept lower risk premiums on risky investments. In such scenarios, achieving the return target established under normal conditions might require accepting a level of risk above the maximum tolerable threshold. This is the moment when an investor should prioritize safety rather than chasing returns, as it is when additional risks are poorly rewarded.

In short, the best strategy is not to set a fixed return target — as this leads to settling for fixed income when rates are high (and when there are often great market opportunities) and to seeking investment alternatives precisely when taking on risk is least rewarding. The ideal approach is to always seek the best risk-return trade-off within the spectrum of opportunities that does not exceed the maximum tolerable risk level. In general, this means investing in higher-risk asset classes, such as equities, when markets are pessimistic and interest rates are high — and returning to more conservative classes, such as floating-rate fixed income, when markets are optimistic and rates are low. This may seem counterintuitive, as it is the opposite of what most investors do — but remember that the extra returns earned by the minority of highly successful investors come precisely from the mistakes made by the majority. Advice from many great investors echoes the same concept:

“Be fearful when others are greedy, and greedy when others are fearful.” – Warren Buffett

“When the world only wants to buy treasury bonds, you can almost close your eyes and buy stocks.” – Michael Steinhardt

“The best time to buy a house is when nobody else wants one.” – John Maynard Keynes

1We adopted the SELIC target rather than the effective SELIC because both rates are very close and the SELIC target has the advantage of having a fixed value for each period, as determined by the COPOM.

2Ártica Long Term started on 06/27/2013 as an investment club and was transformed into an Equity Investment Fund on 09/27/2019