The Risk of Debt in Brazil

Dear investors,

The European Central Bank began reducing its benchmark interest rate in June of this year. The Federal Reserve followed suit, cutting U.S. rates in September. Meanwhile, the Central Bank of Brazil (BACEN) had already been lowering the SELIC rate since August 2023. This earlier move was consistent with the fact that Brazil began its monetary tightening cycle well before developed economies, likely due to its greater experience in dealing with inflationary pressures. However, last month brought a surprise.

Contrary to the direction taken by the world’s major central banks, BACEN decided to reverse course and implemented a modest rate hike, from 10.50% to 10.75%. The market now expects rates to return to around 12.50%, with some projections pointing to a potential increase back to 13.75%. Just a few months ago, this possibility was not even being discussed. We draw two key lessons from this recent experience.

The first is that macroeconomic forecasts are highly unreliable and should not serve as a primary foundation for investment theses. We have written about this before, in our February 2022 letter, “How to Navigate the Macroeconomic Environment,” but a recent example helps reinforce the point.

The second is that there is wisdom in the approach traditionally adopted by Brazilian business owners, who tend to maintain lower levels of leverage than what financial theory might suggest as optimal. Much of the business literature commonly used in Brazil is imported from the United States and is broadly applicable. However, certain aspects require adaptation to local conditions. The approach to corporate debt is one of them.

Why Almost Every Company Uses Debt

A company has two main external sources of capital: equity, invested by its shareholders, and debt, provided by creditors. The fundamental role of a business is to generate returns on this invested capital at a satisfactory rate—commonly referred to as the cost of capital.

A company’s ability to generate operating results is independent of how its capital is financed. The capital structure—i.e., the mix between shareholders and creditors—only determines how those results are distributed. Shareholders seek the highest possible return, accepting a certain level of risk, while creditors aim to receive the contractually agreed return with minimal risk of default. Accordingly, creditors are granted priority in receiving their share of the results and, in exchange, accept a lower, fixed return than the return expected by shareholders.

If the company’s return exceeds the cost of debt, shareholders capture the residual value, and the return on equity becomes higher than the return of the business itself. For example, if a company is financed with 50% debt and 50% equity, the cost of debt is 14% per year, and the return on the business is 18% per year, the return on equity will be 22% per year (0.5 × 14% + 0.5 × 22% = 18%). If the return on the business were 10% per year, the return on equity would fall to 6%. This is the concept of financial leverage: the greater the share of debt in a company’s capital structure, the more amplified the return on equity—both positively and negatively.

An important point is that the cost of debt is not constant. The more a company increases its leverage, the higher the risk that creditors will not receive the agreed return, as a larger portion of the company’s results is required to cover interest payments and principal amortization. In this context, any fluctuation in the business’s profitability can make operating cash flow insufficient. As a result, the cost of debt rises as the share of debt in the capital structure increases.

In theory, the optimal approach is for a company to finance itself with debt up to the point where the marginal cost of additional debt equals the cost of equity. This would represent the optimal leverage level, maximizing the leveraged return to shareholders. We will discuss whether this point is indeed optimal, but it is reasonable to conclude that, in most cases, it makes sense for companies to carry some level of debt, as its cost is typically significantly lower than the cost of equity when leverage remains moderate.

The Brazilian Reality

The precision of theoretical calculations is often challenged in real-world situations. Even engineers apply safety margins in their models to avoid operating too close to theoretical limits—the same principle applies to business management, which deals with far greater uncertainty. This is particularly true in Brazil.

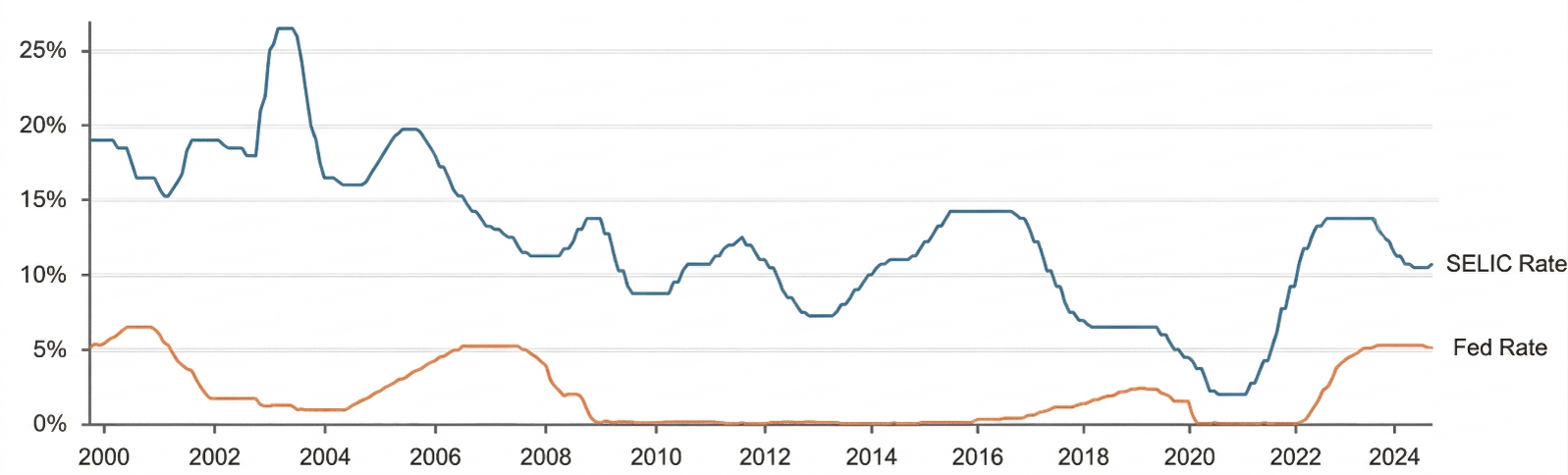

In the U.S. market, it is somewhat easier to manage leverage. The economy is more stable, and corporate debt is typically issued at fixed interest rates. While uncertainty around operating results still exists, the cash flow required to service interest and principal is known in advance. In Brazil, however, corporate debt is more commonly floating-rate, indexed to the CDI (Brazil’s interbank benchmark rate), and we are aware of how volatile the local economy can be. The chart below compares the evolution of the SELIC—the benchmark interest rate in Brazil—with the Fed Funds Rate, the base rate of the U.S. economy.

SELIC Target and Fed Rate History

Source: Central Bank of Brazil and Federal Reserve

It is striking both how much more stable U.S. rates are and how much wider the range of variation is in Brazil. Brazilian interest rates fluctuate so significantly that creditors themselves are often unwilling to take the risk of issuing fixed-rate loans, or they demand such a high return premium to compensate for the uncertainty that most business owners prefer floating-rate debt, effectively assuming the burden of a fluctuating cost of capital over time.

Beyond the unpredictability of financial expenses, there is an additional challenge for companies. When interest rates rise, the economy as a whole slows down. It becomes more difficult to grow revenue or pass through price increases, and business performance tends to weaken precisely when more cash flow is needed to service debt. Many companies end up unable to meet their debt obligations and fall into default. As default rates increase, creditors demand even higher risk premiums, further exacerbating the problem.

The average cost of corporate credit in Brazil (excluding subsidized lines) is around CDI + 10% (Brazil’s interbank benchmark rate). At current SELIC levels, this implies that companies would need to generate returns above 20% per year for borrowing to make economic sense. Very few businesses can consistently achieve this level of return. Reasonably priced debt is typically available only when backed by hard collateral, guarantees from highly capitalized shareholders, or accessed by very large and well-known companies. For the rest, the cost of debt in Brazil is prohibitive, and most borrowing ends up occurring in situations where companies have no alternative, rather than because it is economically attractive.

The conventional wisdom among traditional Brazilian business owners—that it is often better to avoid debt altogether—is a sound approach in an environment characterized by economic instability, volatile interest rates, and wide banking spreads.

Why is Brazil like this?

Most business owners tend to blame the banks. Seeing interest rates rise precisely when companies are going through more challenging periods, they often say that banks’ credit logic is like lending an umbrella when the sun is shining and asking for it back when it starts to rain. Banks, in turn, argue that the issue lies with business owners, who plan poorly, manage their operations inadequately, and generate default levels that require high interest rates for lending to remain viable. While the instinct to blame the immediate counterparty is understandable, the problem stems from a broader context.

Banks operate in a way that ensures the profitability of their own business. Companies take on debt when they believe they can generate sufficient returns or when they have no alternative to keep the business afloat. The real issue is that precise financial planning in an economy where the benchmark interest rate has fluctuated between 2% and 14% over the past five years is akin to building a house of cards on a rocking chair.

The necessary solution would be a more stable macroeconomic environment, with a government that adopts more conservative fiscal practices and a central bank committed to market stability. However, we recognize that this statement resembles the insight of a young manager who concludes that the solution for a struggling company is simple: increase revenues and reduce costs. We do not have high expectations that the Brazilian economy will improve in the near term, and a pragmatic approach leads us to accept that this is the environment we must operate in.

How to Invest in This Environment

Given Brazil’s high interest rates and economic uncertainty, many conclude that the best approach is to invest in fixed-income instruments. However, both debt and equity are exposed to the same underlying business risks of the company being invested in. The difference is that equity acts as a buffer against potential losses imposed on creditors. This protection works well when earnings volatility is limited, but it is ineffective in extreme cases—such as when a company enters judicial reorganization and forces creditors to accept haircuts on their claims to enable the business to survive (as seen in the case of Americanasn S.A.). It is like wearing a seatbelt: it reduces the risk of harm in a typical collision, but is far more effective in a car accident than in a plane crash.

Because fixed income is so popular in Brazil, it is common to see credit instruments offering return premiums that we believe are insufficient relative to the underlying risk. Pricing often seems to overlook the possibility of more severe outcomes, which would affect both shareholders and creditors. As a result, we prefer to invest in equities, maintaining direct exposure to business risk but without the contractual return limitations inherent in fixed-income instruments.

Given this exposure to risk—and the volatility of the Brazilian economy—investments that would deliver excellent returns in a stable environment can become traps. Even when conditions appear favorable in Brazil—which is clearly not the case today—it is unlikely that many years will pass without another crisis. Therefore, we seek to invest in businesses that can withstand a wide range of macroeconomic scenarios without breaking down. Among other things, this generally means avoiding highly leveraged companies.

There was a time when several U.S. business schools advocated that companies should optimize their capital structures, which often resulted in high leverage. It was even argued that indebted companies were better managed, as executives would be forced to maintain the cash flow discipline required to service interest and principal payments. A well-known analogy compared this logic to the idea that drivers would be more careful if a knife were attached to the steering wheel and pointed at their chest.

Warren Buffett criticized this line of thinking, arguing that no rational person would attach a knife to the steering wheel to drive more safely. Even if it reduced the likelihood of accidents, any minor collision would become life-threatening. The same applies to companies: situations that a non-leveraged business could navigate without major issues might lead a highly leveraged one to bankruptcy.

We believe that the more uncertain the macroeconomic environment, the more important it is to prioritize resilience of results over theoretical optimization. Excessive leverage in Brazil is akin to fixing a knife to the steering wheel and driving on a bumpy dirt road—not a particularly wise approach.