Annual Letter 2021

Dear investors,

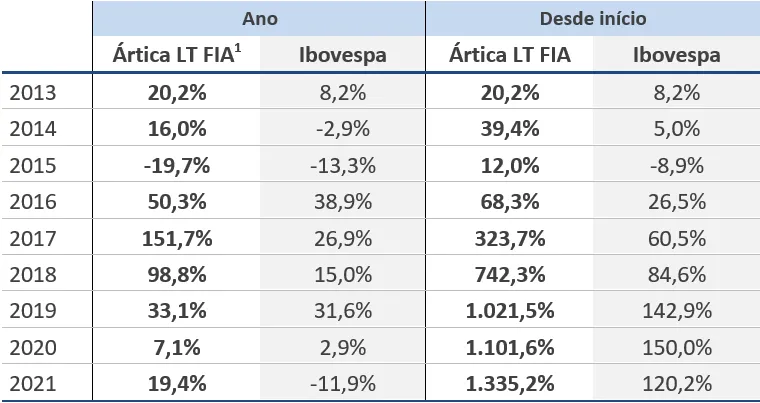

We ended 2021 with a return of 19.4%, higher than the Ibovespa and the CDI, which totaled, respectively, -11.9% and 4.3%. The cumulative return since the Fund's inception, approximately 8 and a half years ago, is 1.335%, representing an annualized return of 36.8%:

Retrospectiva 2021

Ártica Asset achieved several important milestones in 2021. In addition to delivering good returns to investors (we outperformed the Ibovespa by 31.41% on the 2021 stock index), the fund achieved a net worth of R$155 million (R$155 million) and more than doubled the number of investors (we went from 60 to 125).

Most importantly, we've successfully attracted investors aligned with our long-term philosophy. As a result, 107 of these 125 investors have never made a withdrawal, and 77 of them have invested in Ártica LT FIA more than once.

Having aligned investors is essential for us, as managers, to continue making decisions with a long-term perspective. Let me explain: Imagine that a good company's stock is trading at R$ 5.00, and our conservative valuation points to a fair value of R$ 10.00 (100% of upside!). The problem is that, due to market sentiment, this stock only falls. What should we do in a situation like this?

If you have a long-term mindset, the answer is obvious: buying a good company's stock at a 50% discount is a great opportunity. This stock may not make money in a month (or a year), but over a 3-5-year period, it's likely to be a very profitable investment. However, if the investor has a short-term bias, thinking of making money next month, they'll likely miss this opportunity. And if they do invest, they won't have the stomach to stay invested if the market continues to punish the stock and it drops from R$ 5.00 to R$ 4.00.

Our investment in Unipar exemplifies this dynamic. We initiated the investment in August 2014, and in just over six months, the shares had fallen approximately 25% (compared to a 12% drop in the Ibovespa index during the period)! It took almost two years for the share price to return to our initial purchase price. Undoubtedly, an uninspiring start for the position. Even with the decline, we maintained our conviction in our thesis and took the opportunity to purchase more Unipar shares at a good price. The result: In five years, the stock provided a return of 20x our invested capital!

If a manager doesn't have an aligned investor base, they can't "afford" to make this type of investment. Ultimately, their impatient investors could decide to withdraw their money if the returns in the coming months disappoint (for example, if they don't beat the CDI), so they need to focus on getting the ball rolling and choosing stocks that they believe the market will appreciate in the coming months. This is a difficult type of bet to make consistently.

For this aligned vision, our thanks to the investors of Ártica Long Term FIA! (The name is no coincidence)

Dinâmica de alocação de caixa

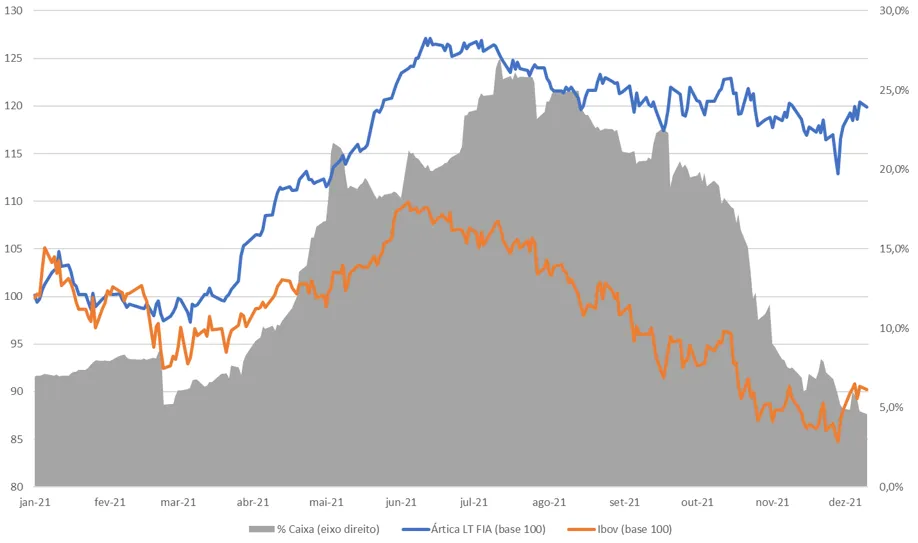

2021 was also a good example of our cash allocation vision. The chart below shows the fund's performance and the Ibovespa index, as well as the evolution of our cash position (as a percentage of the fund's equity) throughout the year.

Gráfico 1 – Evolução do Ártica LT FIA e IBOV (base 100 eixo esquerdo) comparados com evolução do caixa (eixo direito) ao longo de 2021

We started the year with a cash position of 7% of the fund's net worth and gradually increased it throughout the first half of the year, almost in line with the appreciation of Ártica LT FIA shares and the Ibovespa index. During this period of rising stock prices, it becomes more difficult to find new investment opportunities, so it's natural for our cash position to increase (both through the sale of shares that, due to their appreciation, have a reduced margin of safety, and through the receipt of dividends from invested companies).

With the stock market crash in the second half of the year, stocks became cheaper, and we were able to find some good investment opportunities, which reduced the fund's cash position to the current level of 6%. (We're very excited about this topic! With the stock market crash in recent months, we were able to build positions in great companies at very attractive prices!)

To be clear, at no point do we attempt to market time (i.e., try to predict the best times to enter and exit the stock market). We don't know how to do that (and we believe no one does). We simply buy when stocks are cheap and sell when they are expensive.

Dilema entre investir em bolsa ou renda fixa

2021 also marked a period of sharp increases in the Selic rate. The Brazilian economy's benchmark interest rate rose from 2.0% at the beginning of the year to 9.25% at the end of the year, and the rate is expected to continue rising at upcoming Central Bank meetings. This 7.25% interest rate increase over a single year is the largest in history since the Real Plan.

Given this scenario of higher interest rates, fixed income is once again becoming attractive to investors, which has led many to ask us: "Why invest in stocks now, given that I can already get a very attractive return on fixed income, without risk?"

Our view is that it is precisely in scenarios of higher interest rates that investors should increase investments in variable income.

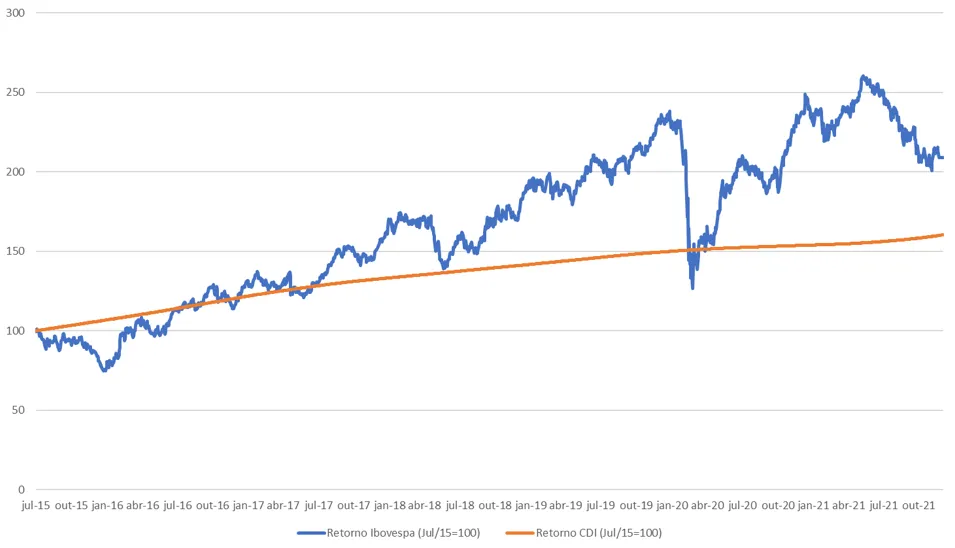

To illustrate this point, let's first focus on historical evidence. Six years ago, in July 2015, the Selic rate reached 14.25% per year, remaining at that level for over a year, until October 2016. This 14.25% rate is undoubtedly quite attractive and led many investors to concentrate their investments in fixed income. The result: An investor who had kept their money invested in the CDI from July 2015 to December 2021 would have achieved a return of 60%, or an annual return of 7.7% per year. By keeping this money in the stock market, the investor would have achieved a return of 109% (12.2% per year). This is a significantly higher return, even considering that we had an impeachment, a truckers' strike, and a pandemic during this period.

Gráfico 2 – Retorno de CDI vs. Ibovespa (Jul/15 – Dez/21)

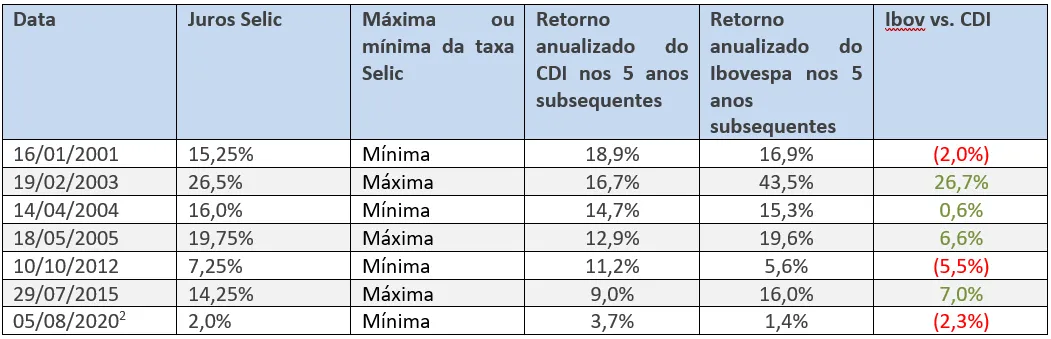

The stock market's outperformance during this period is not an isolated event. We compared fixed-income and variable-income returns over several time periods, considering the interest rate scenario in each. The data in the table below, which shows the return obtained by an investment in fixed income (CDI) or variable income (Ibovespa) in the five years following the Selic rate's historical highs or lows, makes the conclusion quite clear: the best times to invest in the stock market are precisely when the Selic rate is highest (gray lines in the table)!

Tabela 1 – Retornos de CDI vs. Ibovespa em diversos cenários de juros

And why does this happen?

The main reason is simply a matter of price. In periods of high interest rates, stocks tend to become cheaper, and therefore, it's natural for stock market returns to be higher in subsequent years. The opposite occurs in scenarios of lower interest rates.

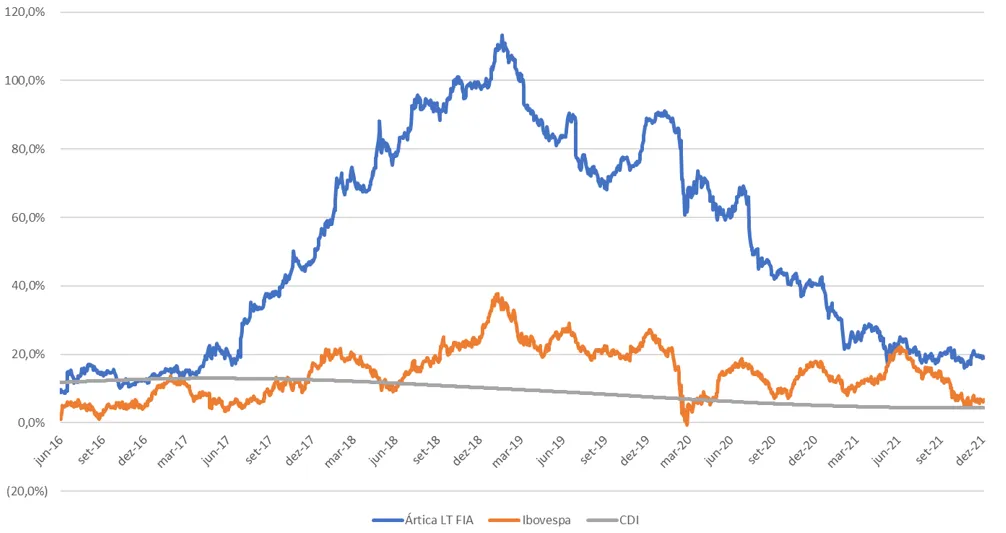

So does this mean that during times of low interest rates, we should avoid the stock market? Not avoid, but be extra careful to maintain the discipline of buying stocks only when prices are truly good. With this discipline, investing in stocks can outperform fixed income in both low and high interest rates. As the chart below shows, since our founding, Ártica LT FIA has consistently delivered returns higher than those of the CDI and Ibovespa over three-year periods.

Gráfico 3 – Retornos anualizados em janelas de 3 anos (Ártica LT FIA vs. Ibovespa vs. CDI)

To our investors

Como temos vários investidores novos nesse ano, vale lembrar que nossa equipe está sempre à disposição para sanar dúvidas sobre rentabilidade, explicar detalhes sobre nossos investimentos, ou mesmo para receber sugestões e ideias que gostariam de compartilhar. Fiquem à vontade para nos enviar uma mensagem clicking here, que responderemos rapidamente e com o maior prazer.

We would like to take this opportunity to wish everyone an excellent 2022!

A hug,

Arctic Asset Management Team