Stocks with insider purchases

Dear investors,

An analysis that we consider to be quite relevant for investment decision-making is to evaluate the level of purchases by people who know the company's operations and numbers internally – the Insiders. This information is useful both because the insiders They are the ones who know the company best and, in theory, would be able to estimate its fair value more accurately, as it is always desirable to invest in companies in which the main decision-makers are aligned with their shareholders through the investment of their assets in the business.

In this month's letter, we explore the topic and provide some research based on historical data that supports our view.

“Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise” – Peter Lynch

O que são compras de insider

Insiders is the English term used to designate people with access to key company information, such as controllers, directors, and officers. Because they possess "privileged" information, they are subject to specific trading rules—for example, they cannot buy or sell shares close to quarterly earnings announcements.

In Brazil, CVM Instruction 358 regulates such transactions and establishes that they cannot be carried out in the 15 days prior to the disclosure of companies' financial information and before the disclosure of material facts.

Conceptually, they would be better positioned than the market to assess the value of their company, so purchases made by them could indicate when they believe there are good opportunities.

Such information may be of various natures. Examples include temporary changes in business conditions (e.g., improvements in the industry's competitive dynamics; growth in the volume of orders for new products; price increases; cost reduction programs) or a better assessment of the company's true value (e.g., turnaround successful in some subsidiary that operates at a loss; M&A operations; profit growth when new product development costs are over).

Resultados de pesquisas sobre o tema

Returns associated with purchases of Insiders have been analyzed in numerous academic studies over several decades. In all cases, the evidence shows that, in fact, purchases of Insiders tend to be good predictors of future stock profitability.

The table below presents the results of 5 studies carried out in the USA in the 1950s, 60s and 70s. In all cases, the companies selected for the study were those that presented purchasing volumes of insider that significantly exceeded the sales volume of insiders. It was also considered an investment strategy in the stock shortly after the information about the purchase of insider.

Tabela 1 – Retornos de ações compradas logo após a compra de insiders1

Some of the best-known studies on the topic of transactions Insiders were conducted in the 1970s, 1980s, and 1990s by Nejat Seyhun, a professor at the University of Michigan. Based on his studies, Seyhun published a book on the subject: “Investment Intelligence from Insider Trading”.

In the book, the author presents some interesting conclusions from his studies:

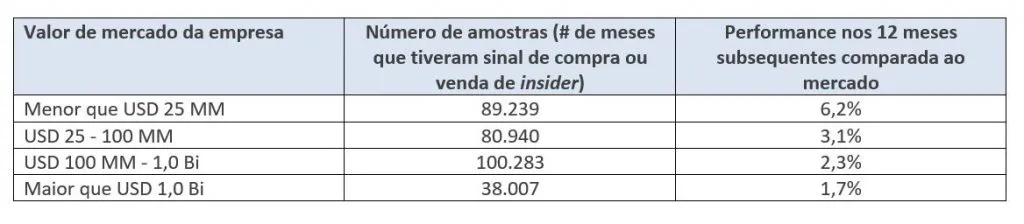

The table below presents the return of stocks compared to market indices in the 12 months following the announcement of a purchase or sale event. insiders. In the study, the author selected only operations that had no conflicting transactions in the previous 3 months (i.e., a company with a purchase of insider which had sales of insider in the previous 3 months are excluded from the sample; the same applies to companies with sales of insider).

Table 2 – Stock returns 12 months after purchase or sale of insiders2

In addition to proving the results of previously conducted studies, the table also shows that purchasing operations insider has greater predictive value than sales of insiders. The reason is that a sale can be motivated by several factors that are independent of the fundamentals of the action (e.g.: the need to withdraw resources to buy an apartment, a car, make a new investment), while a purchase will only be made if the insider see an opportunity to make money.

The author's studies covered the period from 1975 to 1994. In it, it was possible to observe that throughout the entire sample period, transactions of insider proved to be good predictors of future returns, without showing any downward trend.

Even more recent studies continue to point in the same direction. A landmark 2011 article by Kaspar Dardas of the European Business School analyzed transactions of insider in the period from Jan/2002 to Dec/2009. The study showed that purchases defined as “high conviction”3 were associated with returns on average 20.9% higher than market indices in the 12 months following the publication of the purchase.

A very important point to consider in the analysis is the position of the Insiders. In the reports published by companies listed on B3, there is a distinction between three positions: directors, members of the board of directors, and controllers.

The evidence shows that directors are the ones who best trade their companies' shares, followed by advisors and controllers, as shown in the table below.

Table 3 – Returns according to the position of the insider4

The reason for this distinction is their proximity to information. Directors are responsible for key decision-making and are involved in critical company activities on a day-to-day basis. Board members are a little further away from the source of information, but actively participate in the company's key strategic decisions. Controllers, on the other hand, often have access to company information through directors or board members, which reduces their advantage when trading shares.

One finding interesting thing about the study is that purchases of insider in small companies it has greater predictive power than in large companies, as shown in the table below.

Table 4 – Returns according to company size5

As seen in the table above, insiders of small companies are able to obtain profits that exceed the profits of insiders of large companies by an impressive 4 times.

There are two hypotheses to explain this phenomenon. The first is that small companies are less covered by the market, so their market value tends to be farther from their intrinsic value more often, giving the insider greater opportunities to profit from such deviations. The second hypothesis is that new events tend to be more significant in small companies than in large ones. For example, a new product about to be launched and expected annual profit of R$100 million will have a much greater impact on a company with a market capitalization of R$1.0 billion than on one with a market capitalization of R$100 billion.

Transações de insider in practice

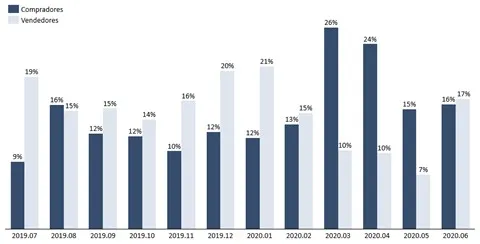

For illustrative purposes, we have compiled transactions from insider of all companies listed on the stock exchange between July 2019 and June 2020 (we have a robot for this). The results are presented in the table below:

Chart 1 – % of companies listed on B3 that are net buyers or sellers of shares

What is striking is that the number of companies with purchases of insider increased substantially in the months of March and April. In other words, the Insiders They proved to be excellent investors in the initial period of the Covid-19 pandemic, buying shares precisely at the time of the greatest drop in the stock market (probably realizing that the market reaction was exaggerated and the pandemic was not affecting business as much as initially feared).

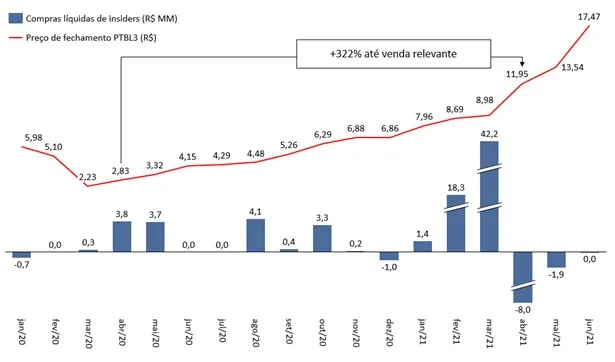

An interesting specific case that occurred in 2020 was that of the company Portobello (ticker PTBL3). As of April 2020, Insiders of the company began to buy shares in significant volumes. What caught attention was that the company had no history of purchasing insider, and suddenly, there were purchases by directors, board members, and the controlling shareholder. Even more significant was that the purchases continued for several months until March 2021. The result: the stock went from a level of R$ 2.83 at the beginning of the purchases to a value of R$ 12.00 when the sales began in April 2021 – an increase of more than 4x in one year.

Graph 2 – Purchases of insider vs share price appreciation (PTBL4)

As demonstrated above, transactions of insider can bring good insights about potential investment opportunities. Therefore, we actively monitor such transactions to choose the best stocks for our portfolio. Obviously, an investment decision is never based solely on this criterion, but rather on knowing that insiders are buying shares in their companies is a great reinforcement for our theses.

1 Studies referred to in the table are listed below and were compiled in an article by Tweedy, Browne Company LLC:

- Donald T. Rogoff, “The Forecasting Properties of Insider Transactions,” Michigan State University, 1964;

- Gary S. Glass, “Extensive Insider Accumulation as an Indicator of Near Term Stock Price Performance,” Ohio State University, 1966;

- Charles W. Devere, Jr., “Relationship Between Insider Trading and Future Performance of NYSE Common Stocks 1960 – 1965”, Portland State College, 1968;

- Jeffrey F.Jaffe, “Special Information and Insider Trading,” Journal of Business, July 1974;

- Martin E. Zweig, “Canny Insiders: Their Transactions Give a Clue to Market Performance,” Barron’s, July 21, 1976.

2 Source: Nejat Seyhun, “Investment Intelligence from Insider Trading”

3 The author defines “high conviction” purchases based on a series of parameters that include the position of the insider, the financial volume and the recurrence of the purchase

4 The sample size differs from Table 2 because the study in Table 3 does not exclude trades that had opposing transactions in the previous three months. Source: Nejat Seyhun, “Investment Intelligence from Insider Trading”

5 The sample size differs from Table 2 because the study in Table 3 does not exclude trades that had opposing transactions in the previous three months. Source: Nejat Seyhun, “Investment Intelligence from Insider Trading”