30 Years of Crisis in Brazil

Dear investors,

Political and economic crises are a recurring feature of the Brazilian equity market. With roughly half of capital flows coming from foreign investors, we not only import global crises but also generate a fair share of domestic ones.

Since the Real Plan, there have been ten periods in which the Bovespa Index declined by at least 25% from its peak over the preceding six months. We use this criterion to identify the most relevant crises over this time horizon and will provide a brief overview of each. By examining how the equity market behaved during these periods and in the years that followed, we aim to better understand how to navigate investments in Brazil’s inherently volatile market.

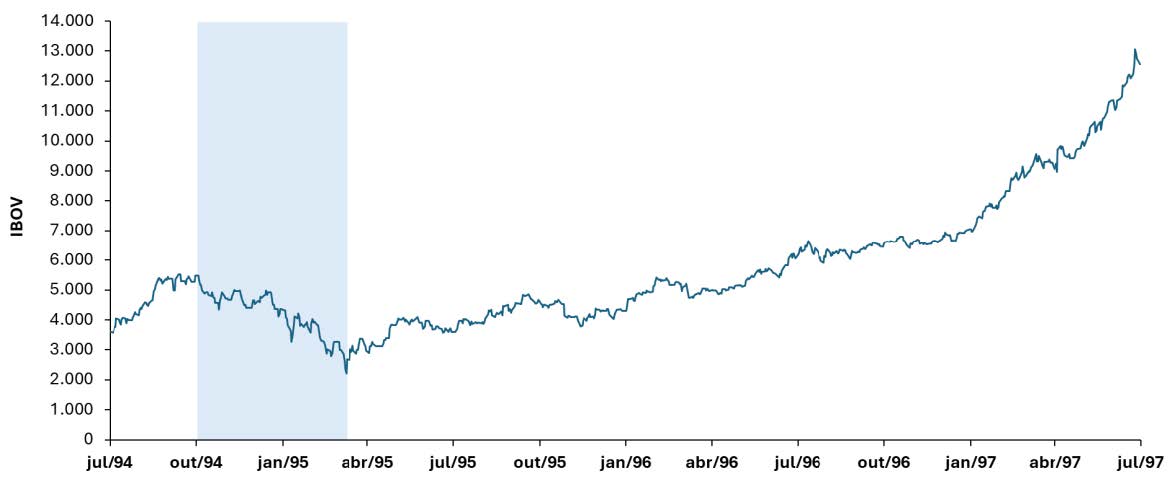

1995: Mexican Crisis (Tequila Effect)

In December 1994, following a period of political instability and significant fiscal deficits, Mexico experienced a sharp currency devaluation. The peso weakened from 3.5 to over 7 per U.S. dollar in a matter of days. In the months that followed, the country faced a massive outflow of foreign capital, high inflation, and a recession.

The event triggered a broader loss of confidence in emerging markets. Brazil had only recently implemented the Real Plan, and there were growing concerns that the Brazilian real could follow a similar path to the Mexican peso. To contain capital outflows, Brazil’s Central Bank sharply raised interest rates in early 1995, and the equity market suffered, declining 60% from its recent peak.

These measures proved effective in containing the damage and preserving monetary stability. The following years were highly favorable for the Brazilian stock market, with the Bovespa Index increasing fivefold before being hit by another crisis originating in Asia.

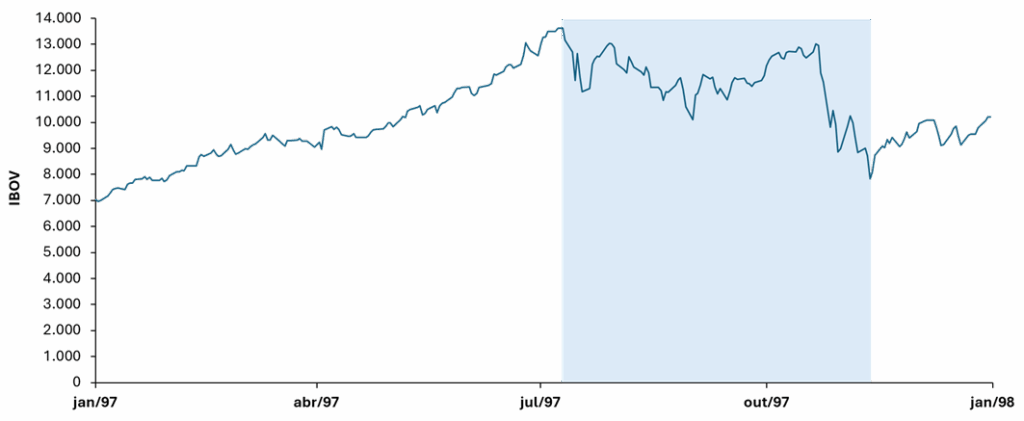

1997: Asian Financial Crisis

The 1990s marked the end of the economic miracle period for several Southeast Asian countries. The model that drove the region’s transformation was based on attracting foreign capital to finance the development of export-oriented industries that leveraged abundant low-cost labor. This strategy was successful for decades. As an illustration, South Korea’s GDP per capita increased from US$158 in 1960 to US$11,000 in 1997. However, prolonged periods of strong economic growth often lead to excesses, and this was also the outcome of the Asian economic miracles.

The availability of easy credit in foreign currency led governments in Southeast Asia to take on debt to finance a wide range of development projects without proper assessment of profitability and risk. As investment returns began to fall short of expectations, external financing dried up and capital flows turned negative.

The trigger for the crisis was the devaluation of the Thai baht. Until July 1997, Thailand operated under a fixed exchange rate regime that kept the baht stable against the U.S. dollar. This encouraged many Thai companies and banks to borrow in dollars with the intention of repaying these loans using revenues denominated in baht, effectively disregarding the associated currency risk. When foreign capital began to leave the country, maintaining the exchange rate peg became unsustainable, and the baht collapsed. The result was a wave of insolvencies that pushed the Thai economy to the brink of collapse. The crisis quickly spread to other countries in the region and then to global markets. The Brazilian stock market declined by 43% between July and November 1997. In the early months of 1998, the market showed signs of recovery, but was soon hit by another similar crisis, this time originating in Russia.

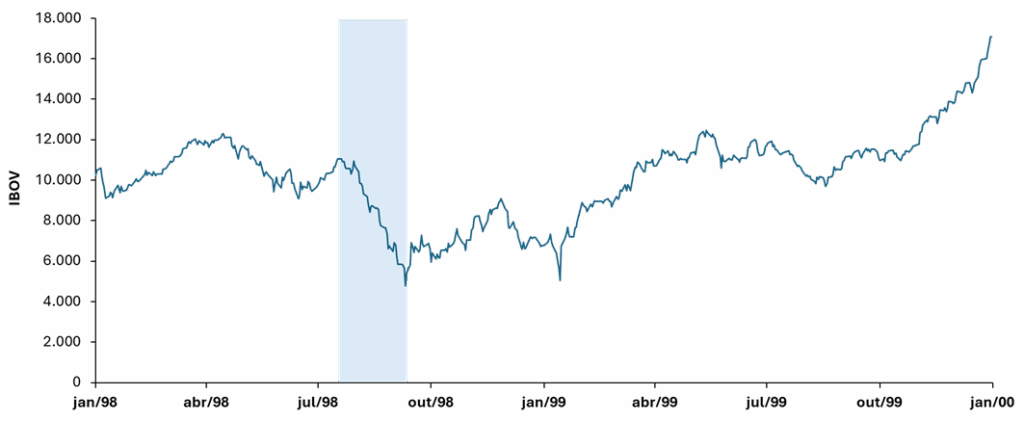

1998: Russian Debt Default

In 1998, post-Soviet Russia was facing persistent fiscal deficits, dependence on external capital, and a rapidly growing public debt burden when, on August 17, the Russian government announced an emergency plan that included a devaluation of the ruble, a restructuring of the banking system, and a partial default on its domestic debt. The announcement caught international creditors by surprise and triggered an even deeper loss of confidence, leading to intensified capital outflows from Russia and other emerging markets.

At the time, Brazil operated under a crawling peg exchange rate regime that kept the real overvalued, while a portion of its public debt was indexed to the U.S. dollar. In light of the Russian crisis, investors began to question the Brazilian government’s ability to sustain the exchange rate regime. This led to significant capital outflows, pressure on foreign reserves, and heightened volatility in the equity market. The Bovespa Index declined by as much as 61% from its peak that year before beginning to recover.

In November 1998, Brazil secured an IMF loan package in an attempt to defend the currency and avoid an imminent crisis, but the measure proved insufficient. On January 15, 1999, the Central Bank announced the abandonment of the exchange rate band regime, replacing it with a floating exchange rate system that remains in place to this day. On the day of the announcement, the Bovespa Index rose 33%, followed by a strong recovery in the subsequent months. By the end of March, the index had increased 112% relative to its level immediately prior to the announcement.

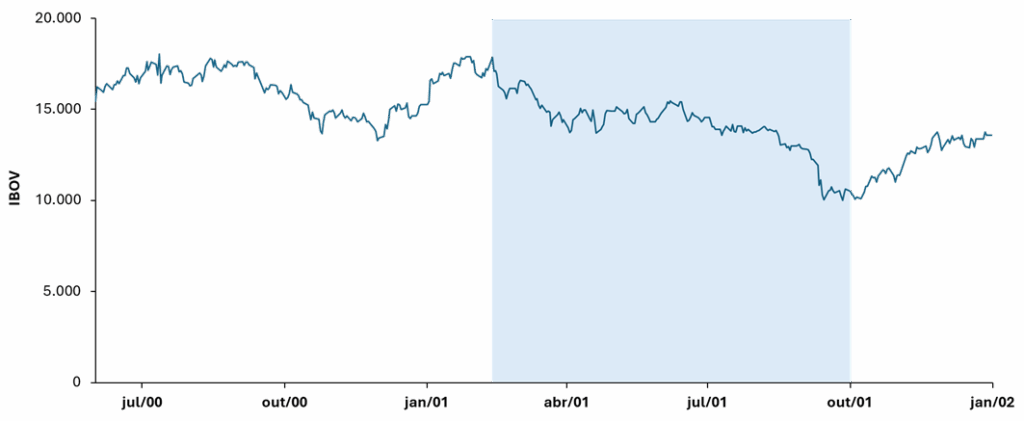

2001: Energy Crisis and the 9/11 Terrorist Attacks

In 2000, Brazil’s GDP grew by 4.4%, driven by the industrial sector and exports that benefited from the depreciation of the real following the adoption of a floating exchange rate regime. The following year, however, an infrastructure bottleneck emerged in the power sector. Due partly to insufficient rainfall and partly to a lack of investment in electricity generation in previous years, there was not enough capacity in 2001 to sustain continued industrial growth.

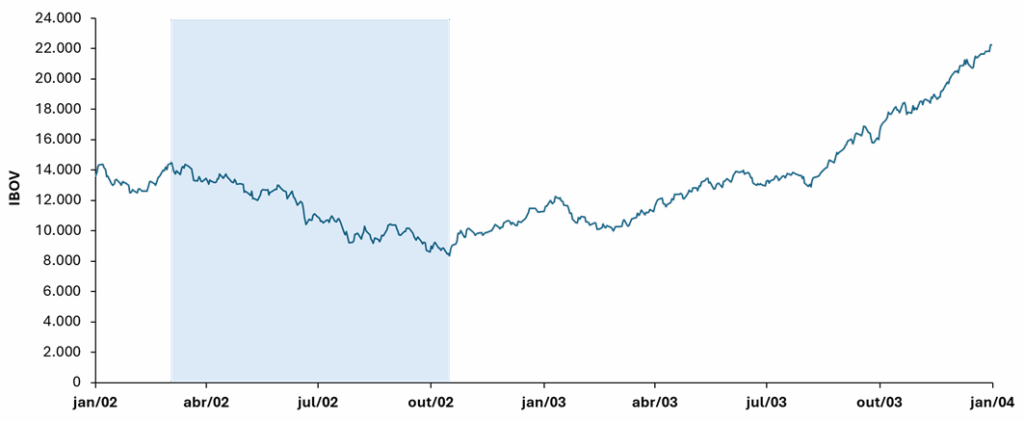

In May, the government announced an energy rationing plan—the so-called “blackout”—which mandated a 20% reduction in electricity consumption, with penalties and supply cuts for those who failed to comply. Inevitably, economic growth was affected, and GDP expanded by only 1.4% that year. The external environment also contributed to the deterioration of the Brazilian equity market. Argentina was facing a severe economic crisis, which spilled over into broader concerns about Brazil, and in September the terrorist attacks that destroyed the Twin Towers in New York sent shockwaves through global markets. The Bovespa Index reached its low for the year in that same month, 44% below its peak in January. In the months that followed, markets partially recovered, and by the end of December had risen 31% from the lows. However, the Bovespa Index would only surpass its previous peak in October 2003, partly because Brazil went through another crisis in 2002—this time driven exclusively by domestic political developments.

2002: Pre-Election Crisis (First Lula Administration)

When Lula began leading the polls in the 2002 presidential election, investors grew concerned about a potential shift in Brazil’s economic policy. The Workers’ Party (PT) had historically adopted a more aggressive stance, fueling speculation about a possible sovereign debt default, loss of inflation control, and increased government intervention in the economy. This crisis of confidence led to large-scale redemptions from local investment funds, forcing indiscriminate selling of equities and driving the Bovespa Index down 39% from its peak that year.

Following Lula’s inauguration, the government signaled policy continuity, which helped restore market confidence. The Central Bank president was maintained, the appointment of Antonio Palocci as Finance Minister was well received, and the federal government issued a formal commitment to fiscal discipline and inflation control. In the years that followed, the Brazilian market experienced the strongest bull cycle in its recent history, driven by China’s rapid growth, which fueled a global commodity boom and significantly benefited Brazil’s exports. From its low in October 2002 to its peak in May 2008—prior to the subprime crisis—the Bovespa Index rose by 778%.

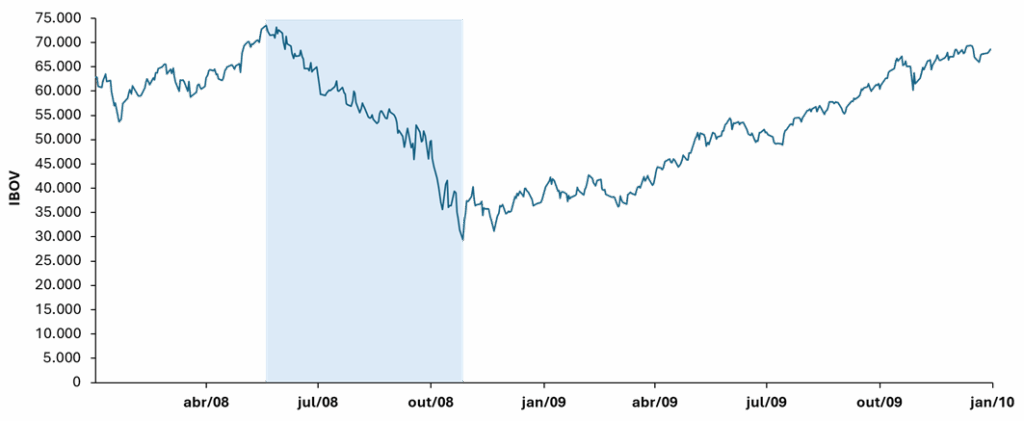

2008: Subprime

In the 2000s, amid low interest rates and a sustained upward trend in the U.S. housing market, financial institutions providing mortgage credit gradually relaxed their risk standards. Assumptions that real estate would always serve as sufficient collateral—given its continued appreciation—and that diversified portfolios would mitigate credit risk led to the creation of a massive volume of high-risk mortgage-backed securities, known as subprime. Rating agencies classified these portfolios as low-risk assets, and the higher yields they offered attracted capital from financial institutions and institutional investors around the world. In the second half of 2006, U.S. housing prices began to decline.

In 2007, the downturn in the housing market intensified, and subprime borrowers started to default on their loans. Properties were no longer sufficient collateral, leaving little recourse to recover invested capital. In 2008, the crisis fully unfolded. The entire chain of financial assets linked to subprime mortgages began to collapse, contaminating the balance sheets of a wide range of institutional investors, including banks, insurers, and pension funds.

The peak of the crisis occurred in the second half of 2008, when several major U.S. financial institutions became insolvent. The defining moment was the collapse of Lehman Brothers, the fourth-largest investment bank in the United States prior to the crisis. Shortly thereafter, Bear Stearns, the fifth-largest investment bank, and AIG, then the world’s largest insurance company, required government-backed rescues coordinated by the Federal Reserve, which sought to prevent a broader collapse of the global financial system.

Brazil could not help but be impacted by this grim scenario. Between May and October 2008, the IBOV index fell 60%. Despite the severity of the crisis, the market began to recover relatively quickly. Within a year of its lowest point, the IBOV index rose 115%, but only surpassed its pre-crisis high almost ten years later, in September 2017.

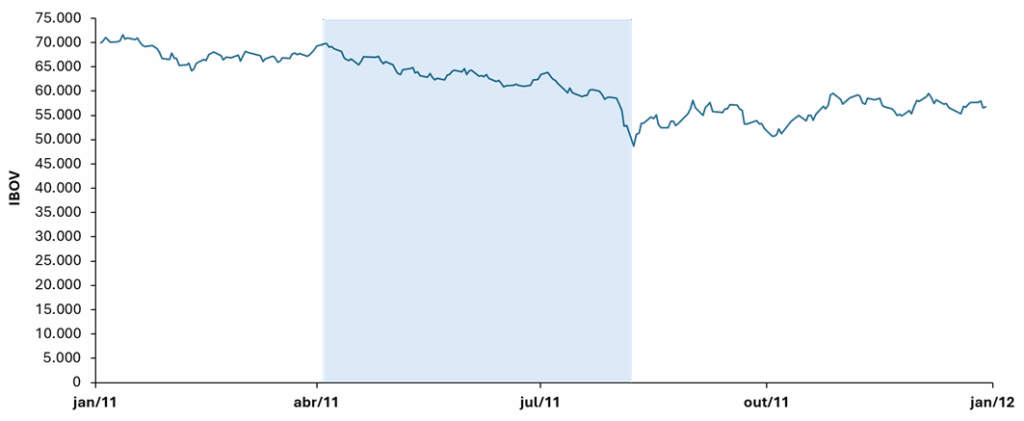

2011: Greek debt crisis

Following its entry into the European Union, Greece gained access to easier credit and lower interest rates. Unsurprisingly, the Greek government embarked on an economic development strategy based on expanding public spending, financed through fiscal deficits and a steadily increasing public debt burden. In order to remain within the Eurozone’s fiscal rules, Greece manipulated its fiscal data for several years. The true scale of the problem only came to light in 2009, when a new prime minister took office and revealed that the fiscal deficit for that year was not 6% of GDP, but 13% (later revised to 15%). Markets immediately began demanding much higher yields on new lending to Greece.

In 2010, the country received a bailout package from the European Commission, the European Central Bank, and the International Monetary Fund. In return, the government committed to a series of fiscal austerity measures aimed at restoring balance to public finances, which ultimately deepened the recession. Despite external support, the crisis was not contained, and in 2011 a second bailout package was announced, accompanied by a restructuring of Greek debt held by private creditors. In such situations, “restructuring” is often a euphemism for a partial default—holders of Greek bonds at the time lost roughly half of their invested capital.

Brazil was affected by the typical loss of confidence in emerging markets that occurs when any one of them faces severe distress, as well as by reduced exports to the European Union, which was in recession and at the time Brazil’s second-largest trading partner. The Bovespa Index fell 30% and took several years to recover, as the global economy remained weak for an extended period, despite expansionary monetary policies implemented by major central banks in developed economies.

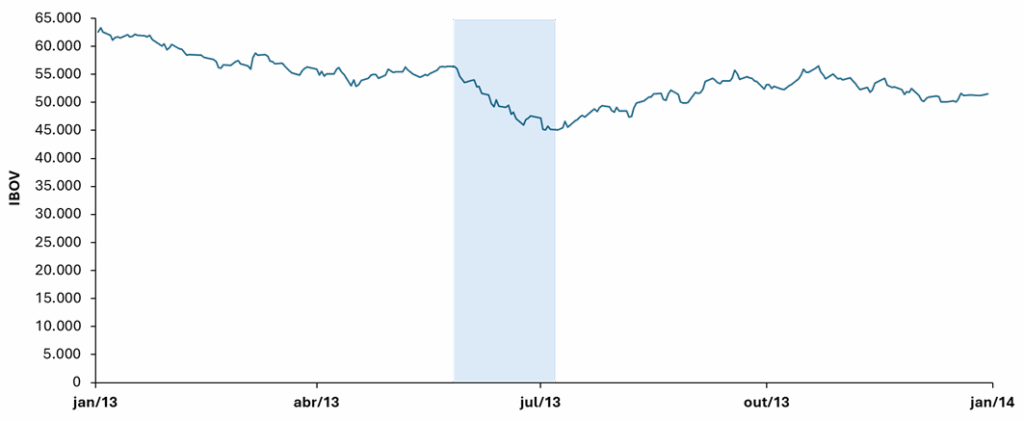

2013: Federal Reserve Tightening and Protests in Brazil

Since the 2008 subprime crisis, the Federal Reserve had been maintaining an expansionary monetary policy known as quantitative easing, which involves continuous purchases of financial assets to inject liquidity into the market. In May 2013, the Federal Reserve signaled that it would begin to scale back these asset purchases, triggering a sharp market reaction.

Although Brazil was not directly involved, the event led to higher U.S. interest rates and capital outflows from emerging markets. The Brazilian stock market, heavily dependent on foreign capital flows, was negatively impacted.

Domestic factors also contributed to the downturn. Brazil’s GDP growth fell short of expectations, inflation was running above the Central Bank’s target ceiling, and rising political tensions added to the perception of risk. June 2013 marked the peak of widespread protests initially triggered by increases in public transportation fares, which soon expanded to include broader concerns such as corruption, healthcare, education, and excessive spending related to the World Cup. These events already signaled the fragility of the Dilma administration, and by early July the Bovespa Index had fallen 29% from its peak for the year.

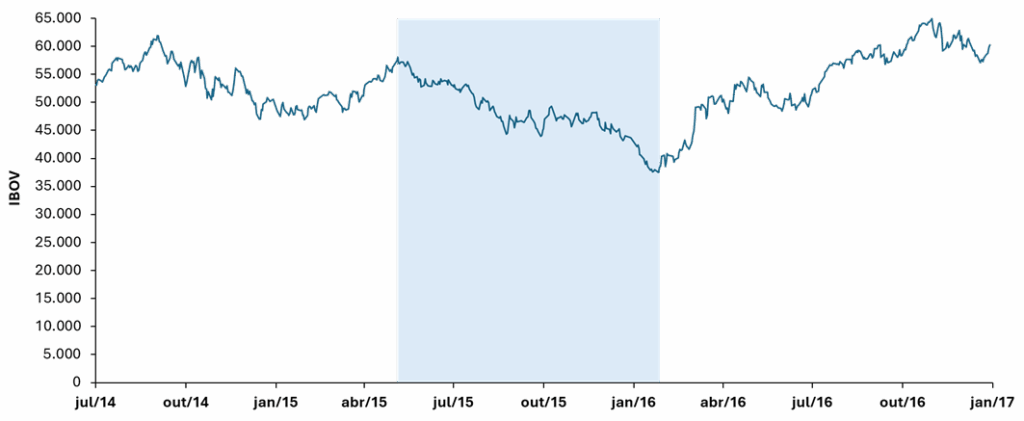

2016: Impeachment of Dilma Rousseff

Brazil’s economy grew a mere 0.1% in 2014. During an election year, then-President Dilma Rousseff adopted expansionary measures and postponed adjustments to fuel and energy prices in an effort to contain inflation. Following her narrow re-election, the consequences of these distortions became apparent: rising fiscal deficits and accounting maneuvers in public finances—known as “fiscal pedaladas.” The country entered a deep recession. GDP contracted for two consecutive years (3.5% in 2015 and 3.3% in 2016), and public debt increased from 52% to 70% of GDP.

At the same time, Operation Car Wash (Lava Jato) exposed systemic corruption at Petrobras and other institutions linked to the federal government. As expected, the market reacted accordingly. On December 2, 2015, Brazil’s lower house of Congress formally initiated impeachment proceedings against Dilma Rousseff. Market pessimism peaked in early 2016, when the Bovespa Index fell 35% from its peak in the previous year. In May, Dilma was suspended from office, and in August her mandate was definitively revoked. Throughout this process, confidence in Brazil’s institutions gradually improved, and by year-end the Bovespa Index had risen 60% from its January low.

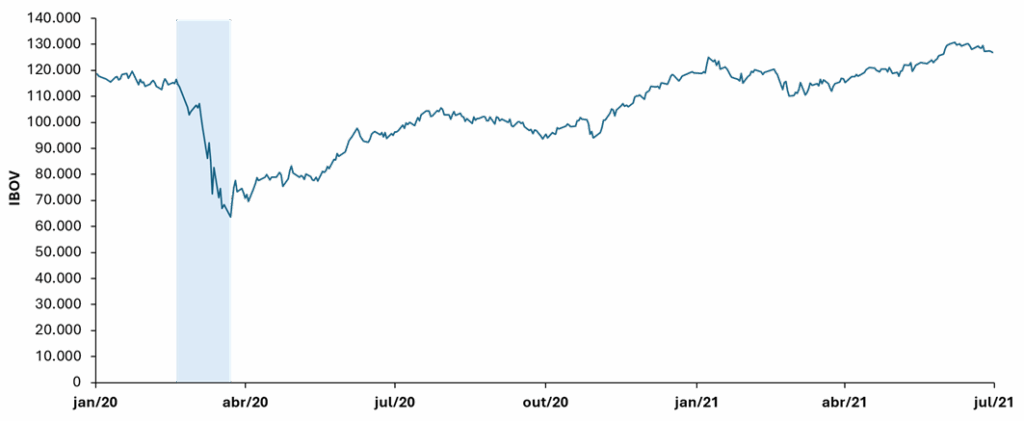

2020: Covid-19 Pandemic

This was the most atypical crisis in the entire period. The world was taken by surprise by a new virus that caused severe respiratory complications in some infected individuals and spread rapidly across the globe. In an effort to contain the spread, most countries imposed restrictions on movement in public spaces—the so-called lockdowns. As a result, a wide range of industrial and commercial activities experienced significant disruptions to productivity. Markets reacted with panic—not only due to the immediate economic damage, but also because of the uncertainty surrounding how long the pandemic would last and the extent of its impact. Equity markets around the world experienced one of the most abrupt declines in history. In Brazil, the Bovespa Index fell 45% in just over one month.

In response, governments and central banks worldwide announced aggressive economic stimulus and social support measures, and equity markets rebounded almost as quickly as they had fallen. In the three months following the March lows, the Bovespa Index rose 50%. By the end of 2020, the index had already recovered to its pre-pandemic level.

Lessons from past crises

It is striking how volatile the Brazilian equity market is. As if domestic challenges were not enough, the reliance on foreign capital makes the market vulnerable to any turbulence in the global economic environment, and our status as an emerging market tends to trigger distrust whenever another country in the same category faces difficulties. But, as with most things, there are two sides to the story.

On average, Brazil has experienced one major crisis every three years over the past decades. Each of these episodes caused substantial wealth destruction for investors who were fully allocated at prior peaks. However, in many cases, the volatility proved excessive, and in more than half of these crises the market rebounded quickly after falling beyond what fundamentals would justify. The same events that create risk also offer highly attractive investment opportunities.

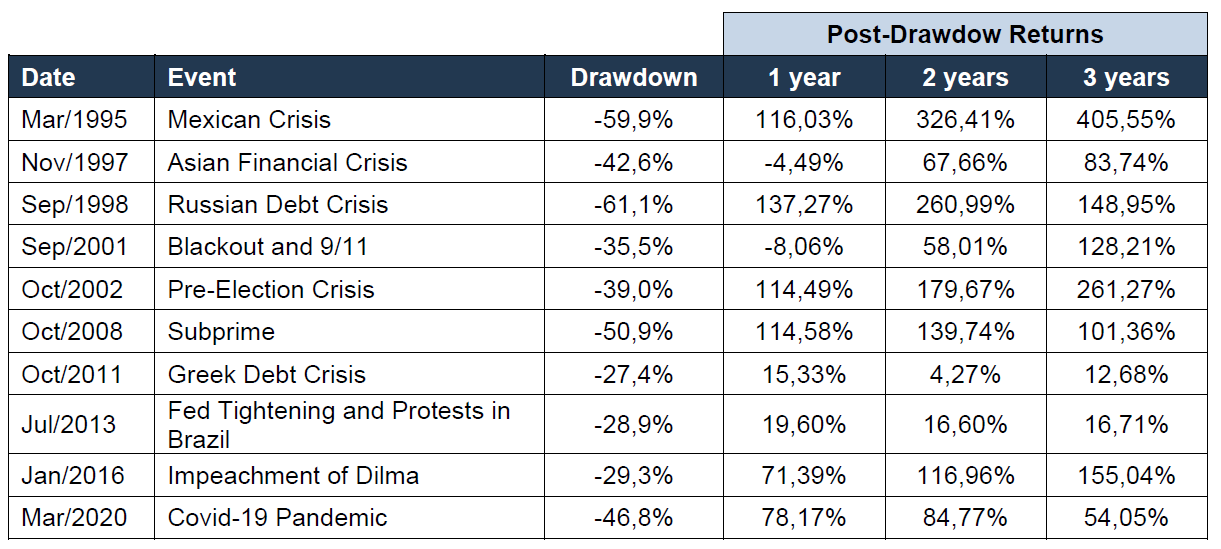

The chart below summarizes the Bovespa Index returns in the years following the trough of each crisis. In several cases, the subsequent returns were exceptional.

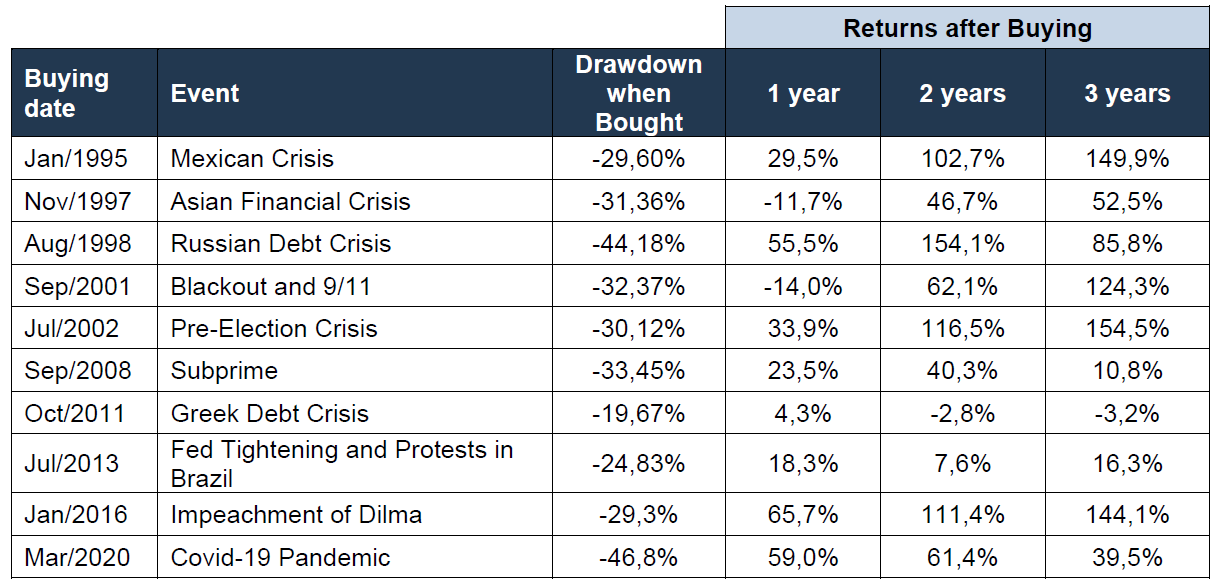

If equal amounts of capital had been invested at those moments and held for three years, the average return of this “portfolio” would have been 33% per year. However, this return is entirely theoretical, as it is not possible to know in advance the exact timing of the trough in each crisis. A more realistic simulation considers the entry point as the moment when the Bovespa Index reaches a 25% drawdown and remains below that level for five consecutive trading days. We assume purchases are made evenly over the subsequent 20 trading days. Exit dates in the simulation are inherently arbitrary, based on 1-, 2-, and 3-year anniversaries from the entry point, also assuming sales executed evenly over the following 20 trading days. The results are summarized in the table below.

Investing the same amount of capital in each crisis and holding for three years would have resulted in an average return of 21% per year. Not bad for a simplistic strategy limited to the Bovespa Index. Setting theoretical simulations aside, there are two key lessons to be drawn from these results.

The first is that the greatest risk in equity investing is not present when the economic environment is weak and overall sentiment is pessimistic. In such moments, the downside is already priced in. The real risk of capital loss arises during periods of euphoria, when investors become complacent and prevailing narratives serve to rationalize why elevated prices are still justified.

The second lesson is that the ability to remain calmly rational and act during periods of widespread distress is one of the main sources of return in equity investing. Some legendary investors attribute this ability to an innate trait that shields them from the paralyzing fear that prevents most people from buying during downturns. Our view is that, like most human abilities, it is partly innate and partly developed through discipline and training. Having experienced multiple economic cycles and maintaining the discipline to follow well-defined principles are critical in distancing oneself from the market’s prevailing sentiment.

Where We Stand Today

Revisiting past crises provides a useful perspective for assessing the current environment. It becomes clear that Brazil’s situation is not as severe as it has been in the past, despite current challenges and the persistent pessimism among local investors. Since the pandemic, we have not experienced an acute crisis. The issue is more chronic: fiscal imbalances and ongoing political noise have prevented the start of a new bull cycle in the equity market. From the pre-pandemic peak to today—a period of approximately 5.5 years—the Bovespa Index has risen 11.3%. Over the same period, inflation (IPCA) increased by 37.5%, and real GDP grew by roughly 14%. In other words, the Brazilian economy has advanced, while equity prices have not kept pace.

The same dynamic can be observed at the company level: financial performance and share prices have diverged, creating attractive investment opportunities. The Ártica Long Term fund has delivered returns approximately 2.5x higher than the Bovespa Index over the past three years. Our approach has been straightforward—ignore political noise and remain focused on capturing these opportunities.